Regular readers will know i have a soft spot for John Cochrane – and while he over-eggs it a little when having a go at Krugman at times, he is one of the best on the stuff that matters in the long run.

His latest post is a review of Bob Gordon’s paper Is Growth Over. In it, Cochrane makes the appropriate point that in the long run even level shocks are unimportant relative to getting the growth stuff right.

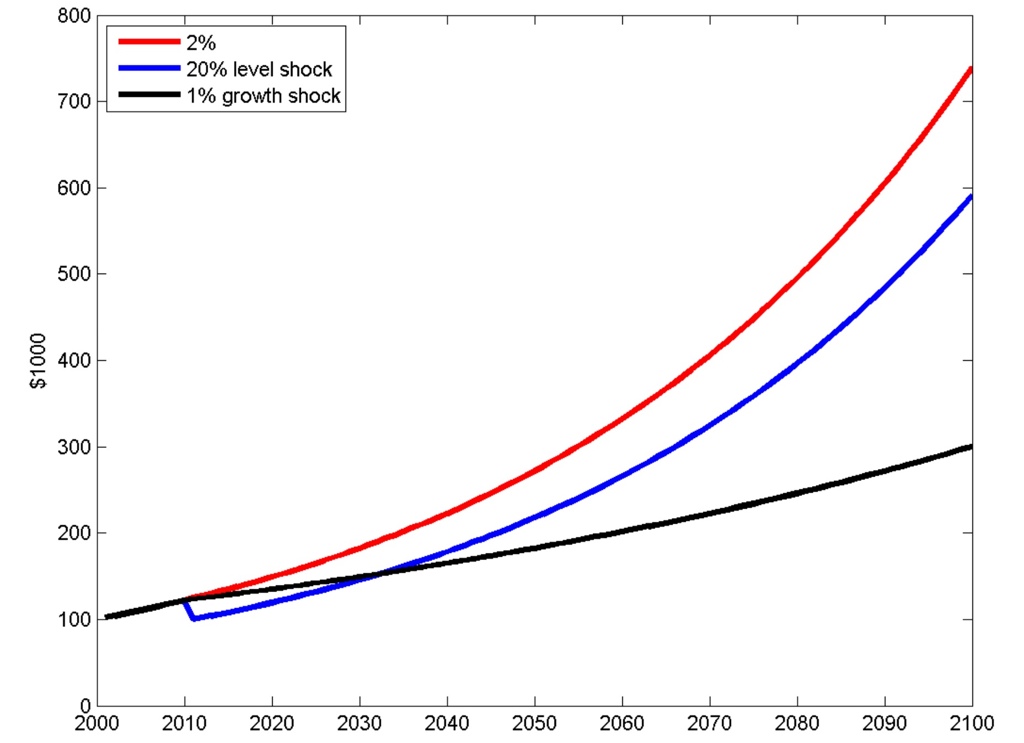

His chart, posted above, shows the improvement in average earnings in the case of compound 2% annual growth (red), a 20% level shock that does not alter the 2% CAGR assumption (let’s call it a GFC), and a shock that lowers growth by 1ppt to 1%

Charts like this are, to me, the strongest argument against ad hoc Keynesian ‘stimulus’ policies – in the long run the only thing that matters is the rate of return on our investments.

Though it does not always have to mean waste, stimulus often means waste (badly allocated capital). In the present case we have also got some bad regulation thrown in – sneaky protectionism is rife across the globe, as are wasteful ‘strategic investment’ subsidies.

In the context of large accumulated debts, this is a disaster – long run growth is the best way we might shrink those debts as a proportion of GDP, and ultimately pay them off.

gosh where to start.

A ‘stimulus’ can only occur in rare circumstances. It certainly wouldn’t be responsible for large scale debt as on a Keynesian basis you would normally have a budget surplus(es) prior to a ‘stimulus’.

Australia is the best example here.

Without one you experience a lower rate of economic growth for a considerable amount of time.

See Japan or the US.

Most of the time in ‘normal’ times A government running a Keynesian economic policy would be running a budget surplus, a large one at that if a boom was on.

oh Noah Smith has a good take down of this paper as well.

This seems a little trite. Firstly, you’d need to be sure that the 20% level shock doesn’t contribute to a long-term growth shock. Secondly, that level shock represents significant hardship and misery for a lot of people, and that can’t be overlooked. And thirdly, you’d need to be sure that stimulus is more wasteful than the alternative – it’s not enough to argue that it can be wasteful (although the evidence in Australian terms is pretty thin to support that assertion). You have to make the case that it’s more wasteful than 25% unemployment.

I think this is the right line of argument for short term stimulus – we should be willing to pay a price to limit skills losses due to temporary unemployment. However once we frame it that way, it suggests we should also look at other policies that encourage skills attrition, like unemployment insurance and minimum wages.

My strongest view is that a job is a pure good – i am much more concerned with unemployment than equality. But bad macro policies seem to stuff everything up – you get high inequality, low growth, and high unemployment … Probably due to distionary regulations and taxes.

I do not see much evidence of historical ‘path dependence’ – if anything the miracle of long run growth had been how resilient it was. Trend growth for the US was 3% forever, under Truman, Kennedy, Johnson, Nixon and Reagan … But now they struggle to beat 2%

I am sceptical of the ‘end of growth’ arguments (seems like flat-earth stuff to me) … But i like the chart as it makes clear what matters in the long run.

The US struggles to beat 2% GDP growth because the US is in a “balance sheet recession”. Private debt is near Great depression levels. US Stiulus has been too low to meet the private sector’s desire to net save and repair household balance sheets.

The people who have understood the dynamic of a balance sheet recession (Richard Koo, Warren Mosler, Cullen Roach, Ray Dalio) also understood US GDP growth was always going to be anemic post the debt bubble.

I read Koo’s book too – i wasn’t convinced he had found the holy grail.

I agree with you that debt funded investments that do not pay off (i prefer this to the meaningless term ‘balance sheet recession’) hurt for a time. The key reasons seem to be that capital re-allocation is slow and animal spirits are weak, so it is hard to invest the increase in savings, which ultimately results in weak growth and depressed yields.

But there are things that can be done on the supply side to raise expected returns, and they would make some impact, and possibly a large one over a long period of time.

Though it does not always have to mean waste, stimulus often means waste (badly allocated capital)

—–

That’s right!!!! The private sector rarely misallocates capital…just like

Lehman

Enron

OneTel

Babcock & Brown

Allco

Blood Bank

Bernie Madoff

Charles Ponzi

Washinton Mutual Bank

Bear Stearns

etc etc

Get the Government out of the way. The private sector could have won WW2 all on its own – talk about crowding out!!!!!!

Sure, the private sector gets it wrong too … But the great thing about markets is that they take the capital away from the losers. Governments and mandarins are harder to budge.