With the amount of cash in the system well in excess of what’s required to liquify things, the main way that QE works is by taking risk out of the bond market. The idea is that the private sector has a risk-budget and that they are forced to take more risk elsewhere if the RBA buys the bonds. The riskier the bonds the RBA buys, the greater the boost to the economy from QE.

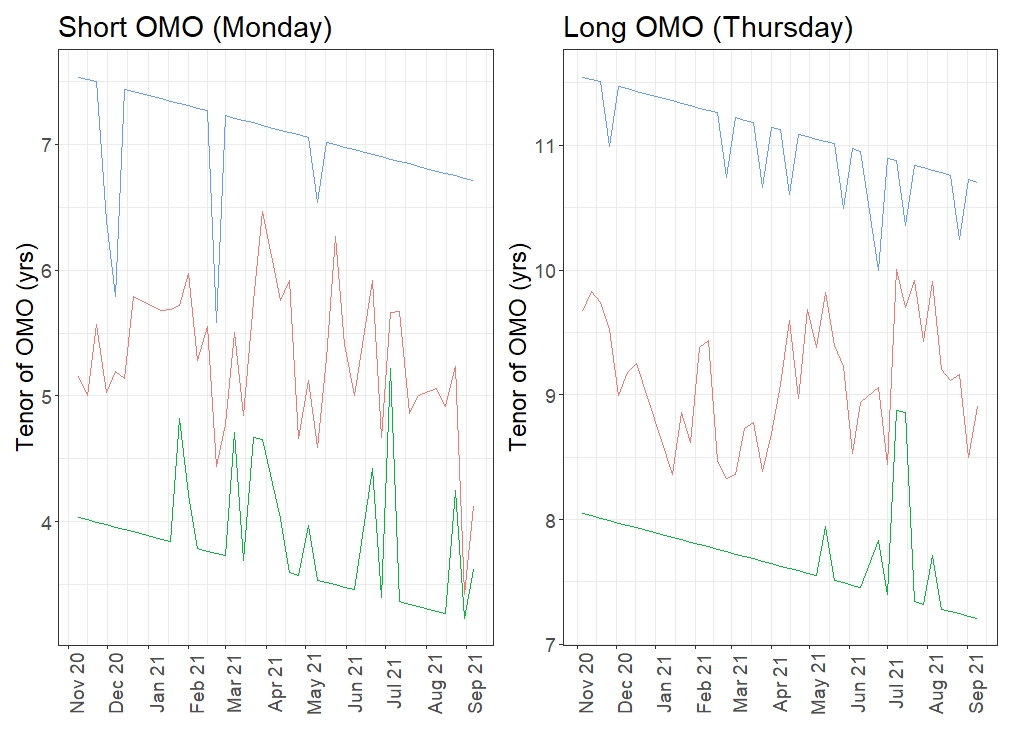

In government bonds, risk is basically proportional to the time to maturity of the bond. The longer the bonds the RBA buys, the greater the risk they withdraw from the market and the greater the boost for the economy. With that in mind, I’ve been interested in the shortening of RBA OMOs of late. While the change does not *technically* reflect a changed stance of Monetary Policy, it does reduce the force of the current policy. It’s a design flaw feature of the current program.

This shortening is built in, due to the fact that the QE-envelope doesn’t roll with the calendar. It means that the bonds are all shortening over time (this is why the blue and green lines slope down in the below chart). The RBA can fight this via bond selection; but this is a bit like fighting gravity. All the bonds roll down, and buying is large relative to their outstanding stock, so the amount of duration the RBA extracts with each round of QE must trend down. Supply/demand problems in the part of the curve they own are now constraint on bond selection (and a constraint on QE in general; see this post for more on the problem with RBA QE).

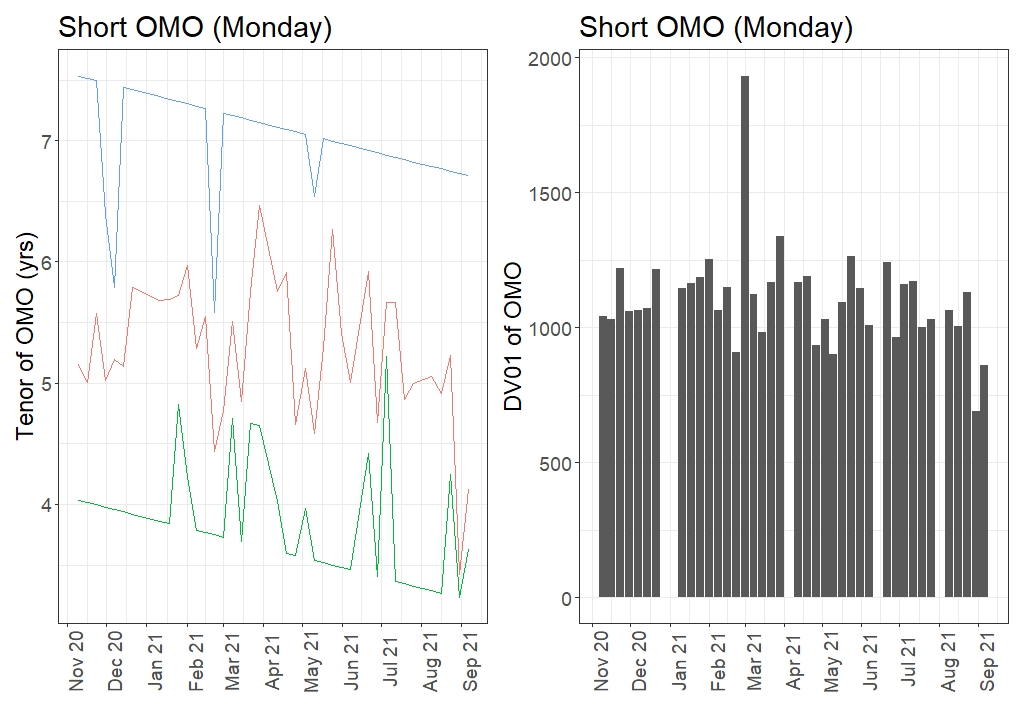

The problem has mostly been in the short OMOs. At the last few Auctions, the RBA has purchased a lot of shorter dated ACGBs. They have continued buying the longest bond in the short-BPP basket (the May’28, which is why the blue line remains flat), but in much smaller size. The skew to the shorter bonds has lowered the weighted average tenor and DV01 of the buybacks.

The fact that the RBA is shortening at the same time that they are tapering suggests to me that they are very comfortable with the decision to taper the pace of QE purchases. Their actions show that they aren’t particularly concerned with making sure that QE is delivering the maximum possible boost to the economy.

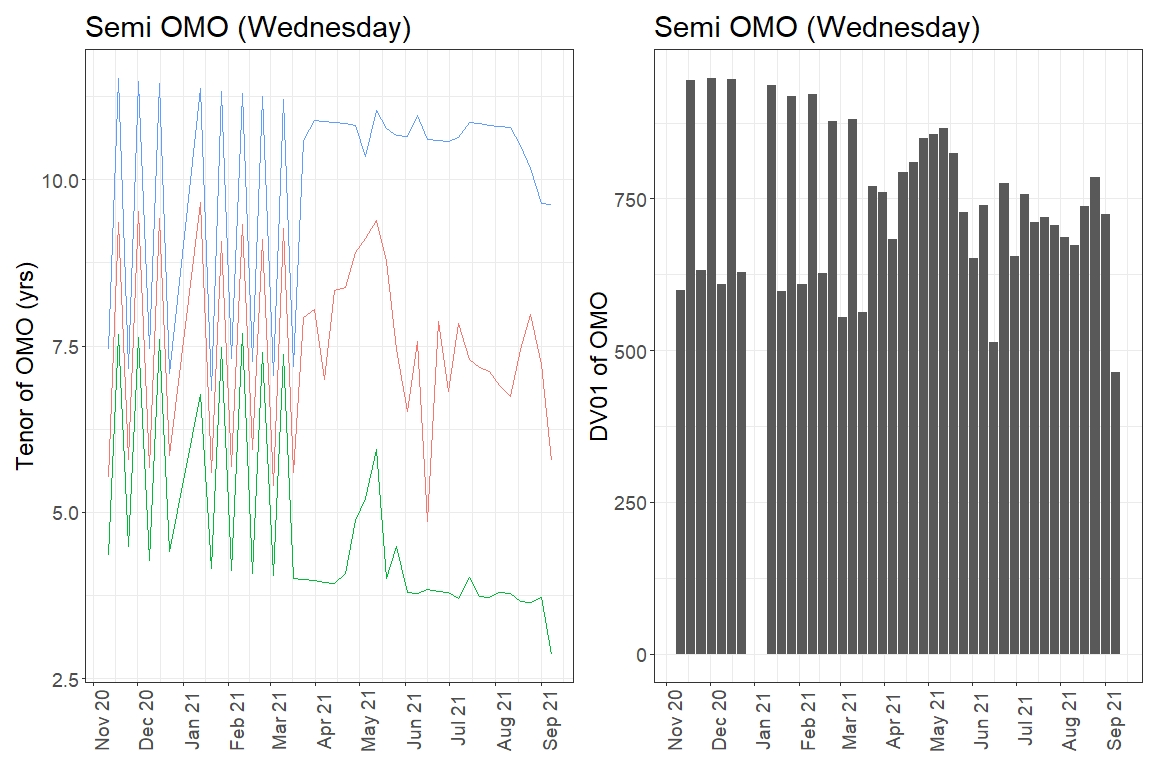

It’s not just an issue with the supply/demand balance in the short BPP basket. They did much the same thing in the Semi OMO last week. Purchases of Q’24s and NSWTC’24s, and a bit of a skew to the shorter Semis, pulled down both the weighted average tenor and DV01 of the OMO.

My hunch is that the RBA is now mostly concerned with the technical aspects of executing the QE without unduly distorting the market (and, perhaps, with one eye on getting out of it all together).

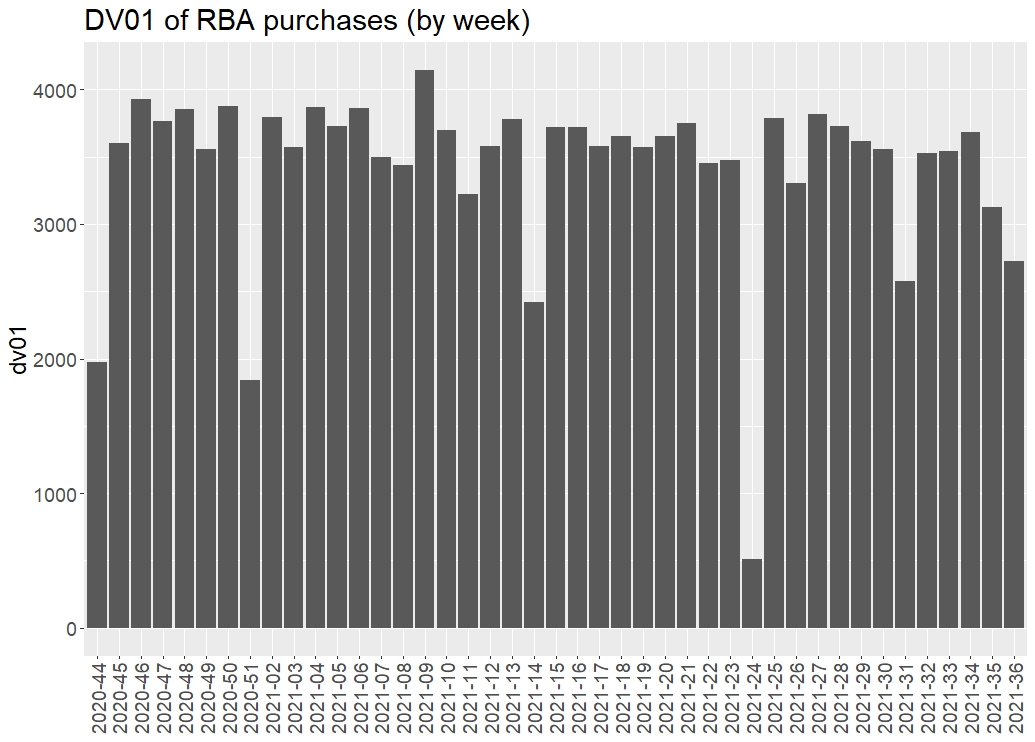

If the bias to toward the shorter bonds is maintained, the weekly DV01 of purchases will decline to around 2.5mil per week starting this week, down from a prior average value of ~3.5mil DV01. That’s a 30% taper in risk terms.

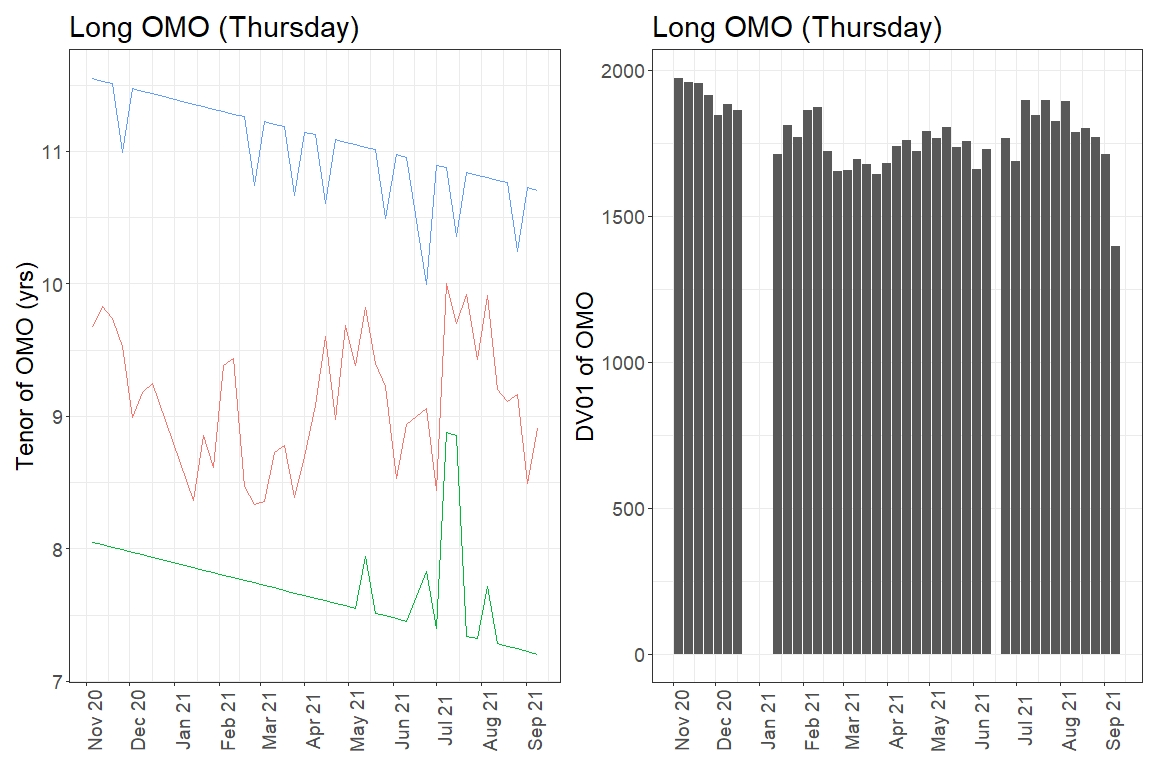

For completeness, I’ve pasted the long OMO charts below. You can see that the RBA was able to fight gravity via bond selection for a time. This is the most easily fixed part of the problem. If the envelope of purchases had rolled with the calendar, it would soon include both the Nov’32s and April’33. This simple change would add around 40bn of capacity to the program and allow the RBA to stabilise the DV01 of QE.