[This post is the first of two on RBA QE. This post shows three problems. The second deals with solutions. I was going to post them together, but it got too long!]

The design of the RBA’s current QE policy is a problem. Current limitations are a modest impediment to easing right now, and a bigger problem if non-standard policy is required for an extended period.

Even if you’re unconcerned about market capacity, there are good reasons for a review. A change that extended the life of the QE would boost the power of current easing, by adding credibility to the threat of further easing. It would also help the RBA resist the gravity of policies they don’t like, such as the return of YCC and or negative interest rates.

Think for a moment what monetary policy could do if there was a large shock. The post-COVID easing was characterised by Central Banks buying a good deal more debt than was issued.

What if easing of similar power was needed once again?

If strong easing was required, concentration limits in the bond market would very likely push the RBA toward other policies. This would mean either YCC (a difficult policy, notwithstanding that Gov Lowe judged it to have been “a successful monetary policy measure”) or negative rates. Perhaps both.

Adding capacity to the QE program by changing its design means that the probability of being pushed toward these undesirable policies is lower. That’s a good thing. It’ll also help market function.

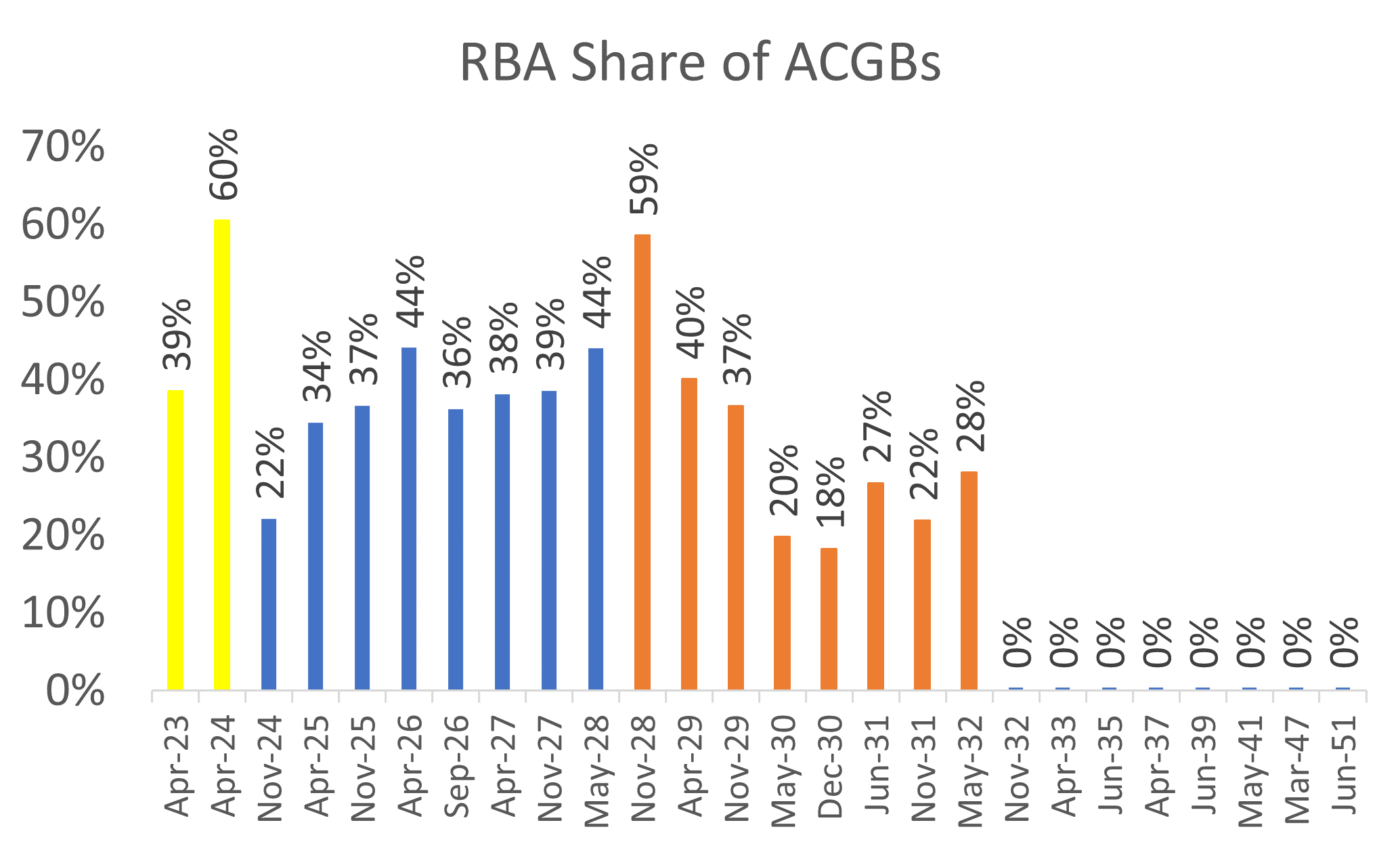

Problem 1: the RBA owns too much of the lines it buys

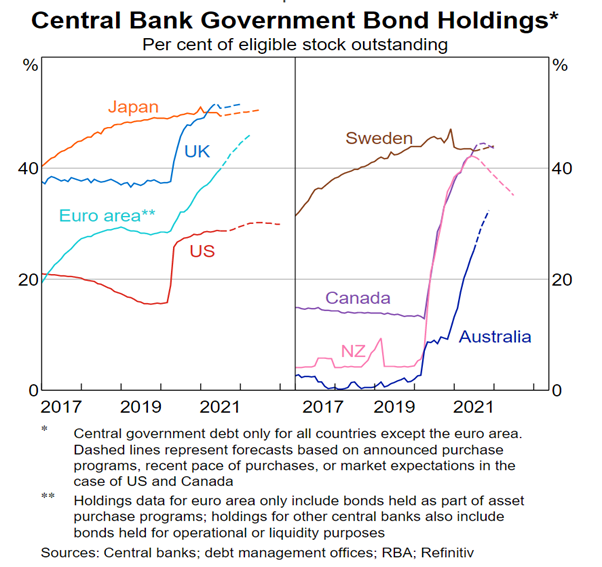

The RBA is fond of charts like the one below. It shows the proportion of the ACGB market the RBA holds, relative to other central banks. According to this chart, the RBA is simply catching up to other central banks, as their market-share rises from the high-20s, to the low-30s by the end of 2021.

This is true: but it’s also a bit of a fudge.

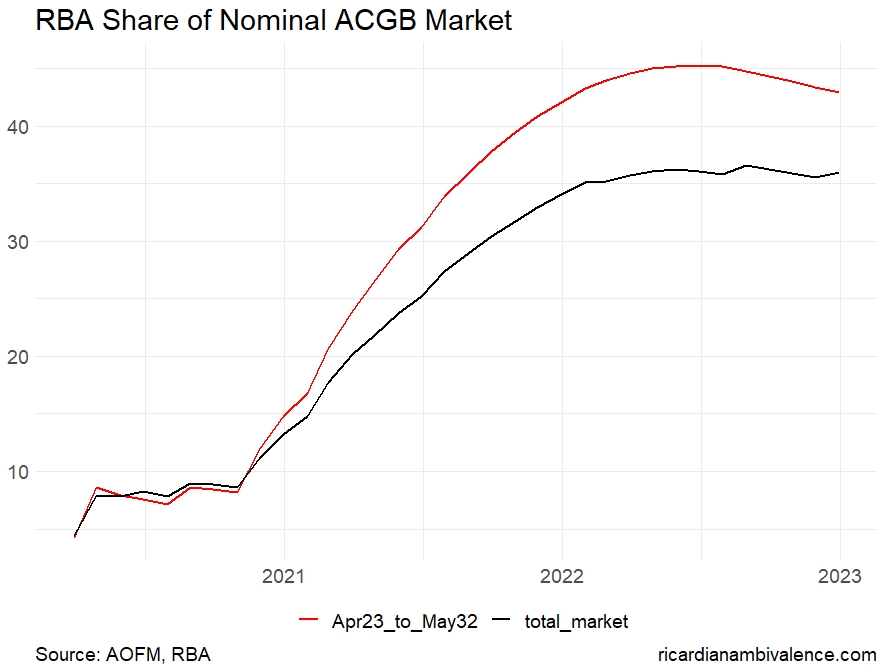

It’s a fudge because the RBA doesn’t buy across the ACGB curve. They only buy a subset of bonds: specifically, the ones that mature between April 2023 and May 2032. And that’s what is relevant when thinking about concentration. Limits arise because market function starts to suffer when the central bank owns too much of a particular line. So, it’s the RBA’s share of bonds that it buys that is relevant when thinking about the capacity of the QE program.

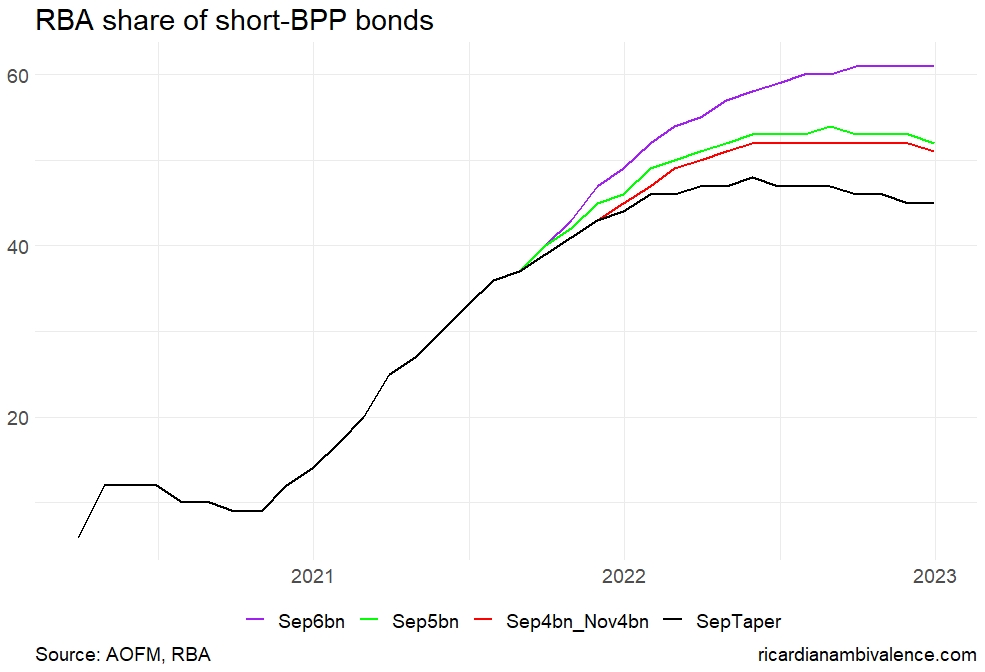

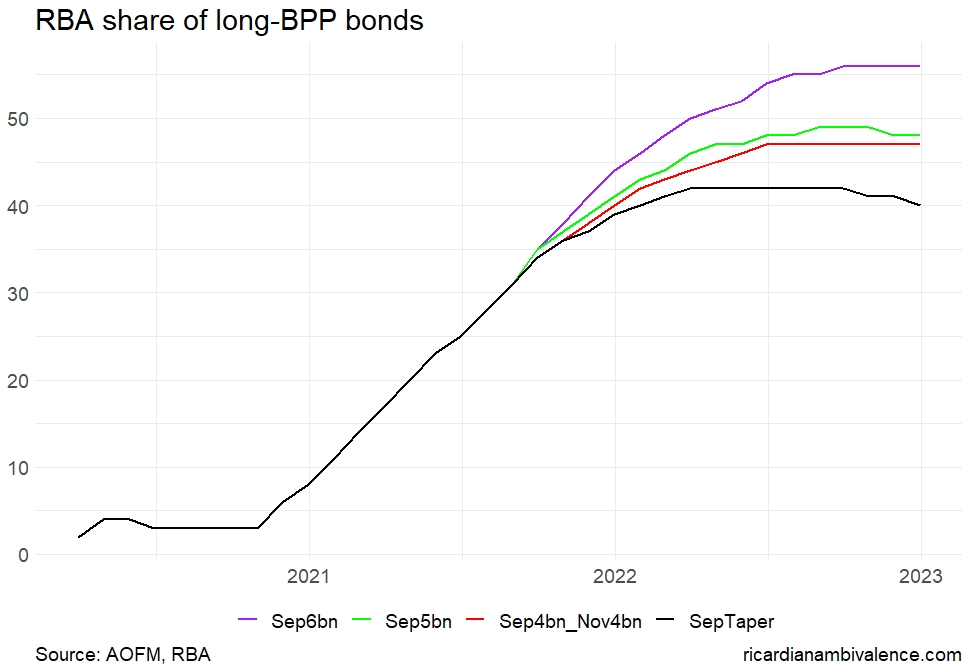

The RBA’s share of this subset of the bond market is a little below 40% just now. Depending on your assumptions, this share will rise to around 45% by mid 2022.

Here I assume no response to the Delta-outbreak. So QE tapers from 5bn to 4bn per week from Sep (as already announced) and steps down 1bn each quarter. This means that QE ends in August 2022, with the RBA having purchased an additional 100bn of ACGBs, or about 20bn more than the AOFM issues. The RBA’s total portfolio of bonds that mature in April 2023, or later, will be around 310bn.

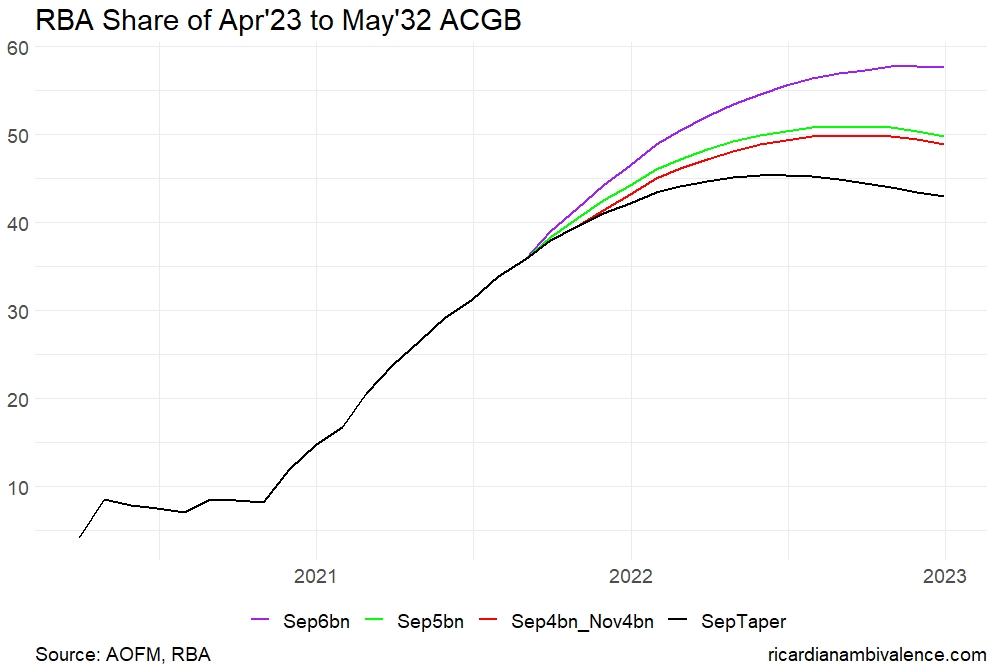

If, instead, the RBA continued buying bonds at 5bn per week until November, and then tapered purchases by 1bn per week at each quarterly review (I’m using the SOMP dates), they would buy 140bn of bonds, and which would take them to a little over 50% of the market by mid-2022. The outcome is much the same if they pre-commit to holding purchases at 4bn per week until February. The RBA’s share of the market would rise to 57% if they boosted QE to 6bn per week from September, and tapered 1bn per week at each quarterly meeting.

Of course, a worse economy will generate more bond issuance, so these ownership calculations are biased a bit high. So, think of this as a baseline on which to compare the policies.

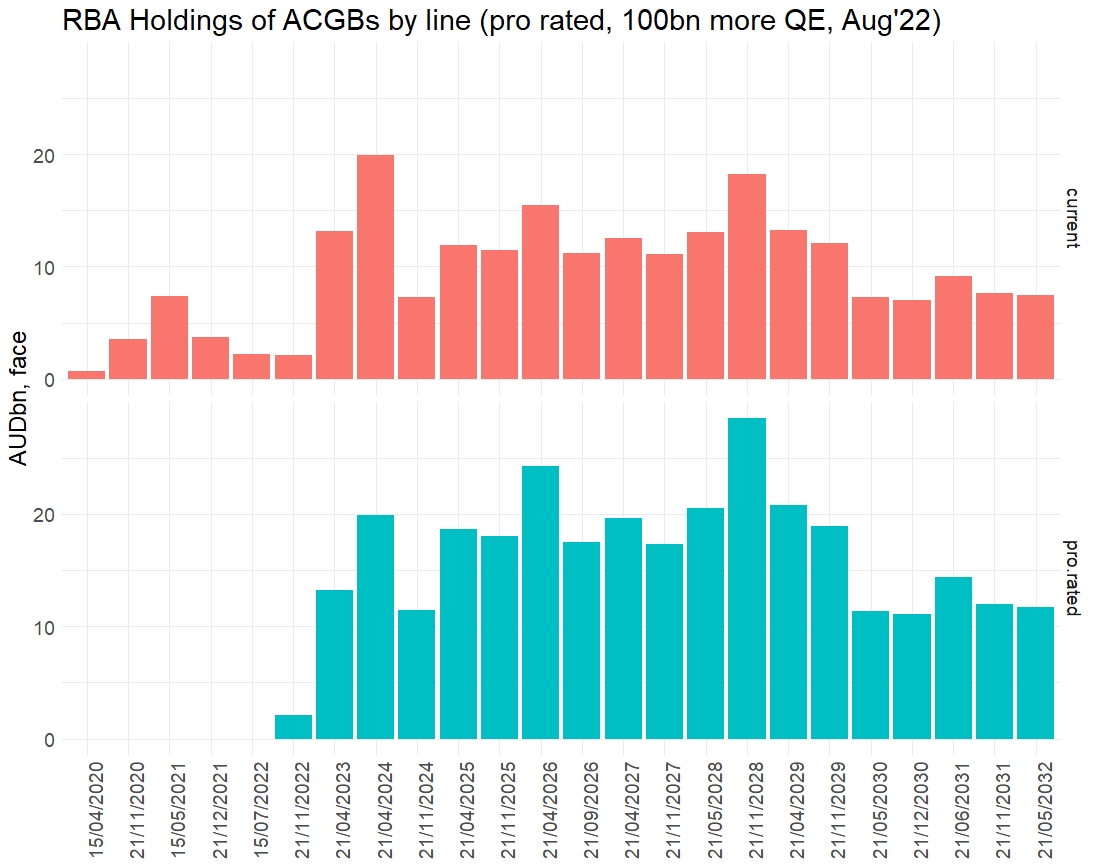

At the bond by bond level, forecasting RBA ownership is trickier. To keep it simple, I’ve assumed that future buying looks like current ownership, and have simply scaled up RBA ownership by the remaining 100bn. Under this assumption, the RBA ends up owning around 20bn of each of the lines between April 2025 and Nov 2029 and about 12bn per line of the other bonds.

The actual outcome may be a bit more evenly distributed than this, as both the AOFM and street will respond to scarcity. However, unless the design of QE is changed, the RBA must buy even amounts from the short BPP basket (the eight bonds from Nov 2024 to May 2028) and the long BPP basket (the eight bonds from Nov 2028 to May 2032). And here we can see the problem.

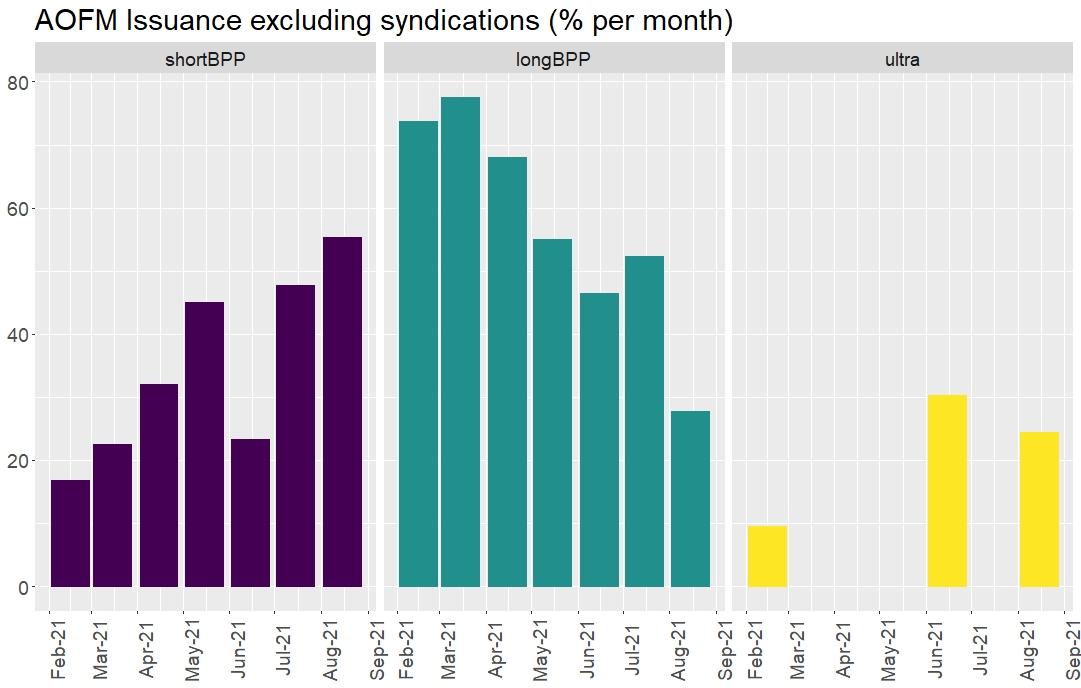

Assuming AOFM issuance is consistent with their recent pattern (44% short BPP basket; 42% long BPP basket; 14% > May’32), we can calculate the share of the market that the RBA owns. The RBA’s share of the short BPP basket rises to 50% in mid-2022. The peak for the short BPP basket rises to 54% if they delay the taper to Nov’21 (49% peak for the long BPP); the outcome for buying at 4bn per week until February is similar; and the RBA’s share of the short BPP basket peaks at 61% (56% long BPP) if the RBA accelerated the pace of QE to 6bn per month from September, and then tapered 1bn per quarter.

While it’s possible that the AOFM will tweak issuance, to lean toward the short BPP basket – and keen observers will note that the AOFM issued 55% Short BPP in August – this isn’t a long-term solution. It just moves the problem into the long BPP basket. Also, it pushes the AOFM further away from their historical issuance pattern. Absent QE, the AOFM’s would be issuing more Nov 2032s and April 33s, and be looking to launch a Q4’33 bond. Instead, they are growing very large refi stack in the BPP-basket bonds.

Problem 2: the tenor of the bonds the RBA buys is shortening

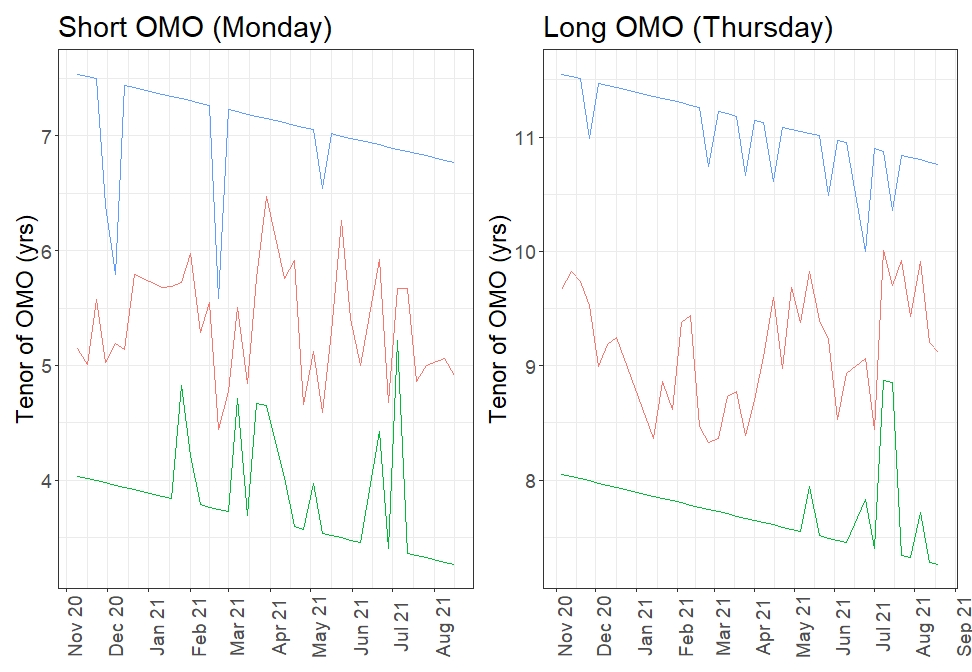

The envelope within which the RBA purchases bonds hasn’t changed since the program started.

For the entire life of the Bond Purchase Program, the RBA has purchased bonds that mature between November 2024 and May 2028 on Monday and bonds that mature between November 2028 and May 2032 on Thursday (April 23 and April 24, the YCC bonds, were purchased when required; Semis are purchased on Wednesday).

As a result, the RBA has had to fight the roll down of the envelope by bond selection. They have done reasonably well so far, but concentration in the April’26 to May’28 part of the curve will become a constraint soon.

This trick has a finite life. As the basket rolls down, the RBA must tilt longer in each OMO to maintain the weighted average tenor. There’s some scope to do that in the long BPP basket, and the RBA may try to stabilise the weighted average tenor by shifting longer in the long BPP buybacks. It can work for a while, but the RBA is fighting gravity. The strategy has finite capacity.

The most obvious solution is to allow bonds to roll into (and out of) the envelope. If the envelopes were set periods from the present day, the long BPP basket would now include the Nov’32 and would soon include the April 2033. This would immediately add 30bn of capacity to the QE program.

However, adding the Nov’28s and Apr’29s wouldn’t do much for the short BPP basket as the RBA already holds a lot of them (59% and 40% respectively).

Problem 3: Semi’s want to issue longer

One common suggestion for how the RBA might extend the life of QE is to increase the proportion of Semis in RBA QE from the present 20%. Semis are a touch over 30% of the combined ACGB + Semi market, so there’s a case that the RBA is under-weight Semis. The RBA currently owns about 50bn of Semis, which is 13% of the total; and about 16% of the subset of Semis the RBA buys.

Semis appear to have more capacity at present. They have underperformed ACGBs by around 25bps over the last few months, so it’s fair to say that the Semi Government Bond market isn’t as tight as the ACGB market.

States generally want to issue long, as they are funding long-lived assets. In terms of the stock of bonds, around 20% are too long for the RBA to buy (the RBA only buys Semis that mature before May 2032). Increasing the tenor of QE would add just under 50bn of stock to the pool of potential assets.

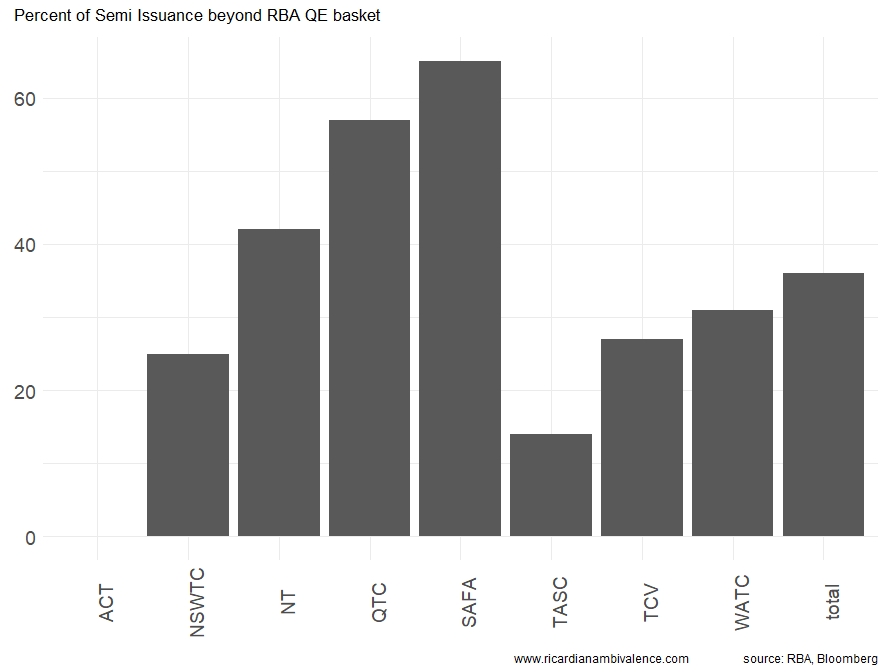

Issuance is a little more skewed. Since QE began in November 2021, Semis have issued just over 35% of their bonds beyond May’32. Looking across the states, this ranges from a high of 65% (SAFA) to a low of 0% (ACT don’t have a bond that matures after 2032).

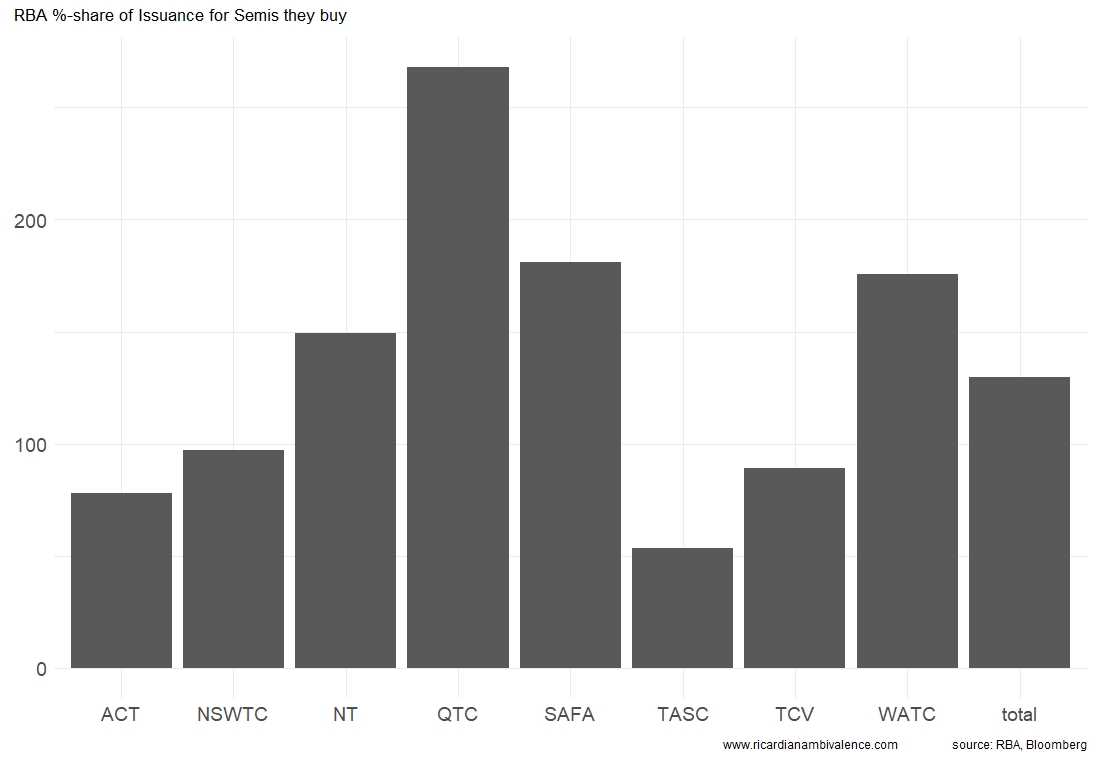

As a result, the RBA’s share of net issuance (excluding maturities) in the sectors they buy has been around 130% (50bn of buying v. 38bn of issuance since QE started in Nov’20). Across the states, this varies between 50% for Tasmania, to almost 270% for QTC.

If the RBA were to buy across the curve in Semis, the RBA’s share of the flow would decline from 130% to 83%. This would mean that ongoing RBA QE would not crowd out the Semi market. It would also better assist the the States to do exactly what the RBA wants them to do — support demand by spending on infrastructure.

5 comments

Comments are closed.