The RBA meets on 7 September, and will again consider the appropriate pace of their QE program. My hunch is that they will pre-commit to maintain the QE at 4bn per week until at least February 2022. There is little difference between this and pushing back the taper until November.

The decision is very much live. We can be pretty sure that the Board considered tweaking the pace of QE in August (and decided to stick with the taper). The structure of the post meeting statement was consistent with a decision, and the content committed the board to reviewing the situation in light of economic conditions and the health situation.

The Economy was strong in Q2, but looks to be much weaker than they expected in Q3’21. The length and futility of Delta-lockdowns means that activity in H2’21 will be weaker than the RBA forecast, and that the recovery will be a little more subdued than they forecast. Delta is weighing on the Global outlook as well, so this ought to be a factor depressing the outlook for 2022.

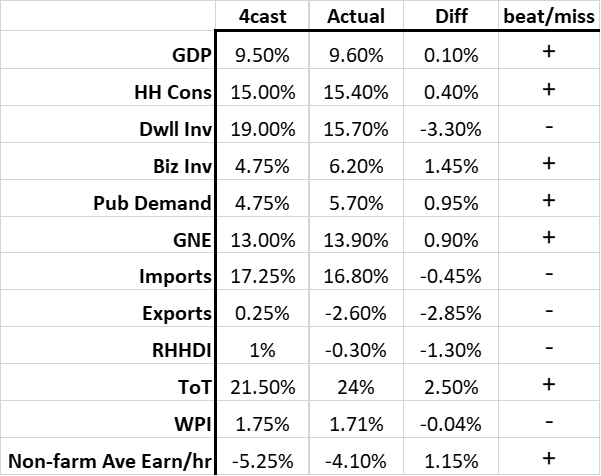

In Australia, Q2 data was around (or a bit stronger than) RBA forecasts. While there were some flukes in the Q2’21 headline GDP outcome of 9.6%yoy, the data when broadly considered fully justified the headline GDP print. In the details, Dwelling Investment missed (and I think will struggle to meet their forecasts), but Consumption, Business Investment, and Public Demand all beat, and the Terms of Trade were much better than expected (though have almost certainly peaked).

The main area of concern is the miss on Real Household Disposable Income (RHHDI). This means that Consumption was a bit of a confidence trick in Q2: by which I mean that Consumption was a little less income funded, and a bit more ‘savings funded’. That sort of consumption is more liable to reverse if there’s a shock that hits confidence.

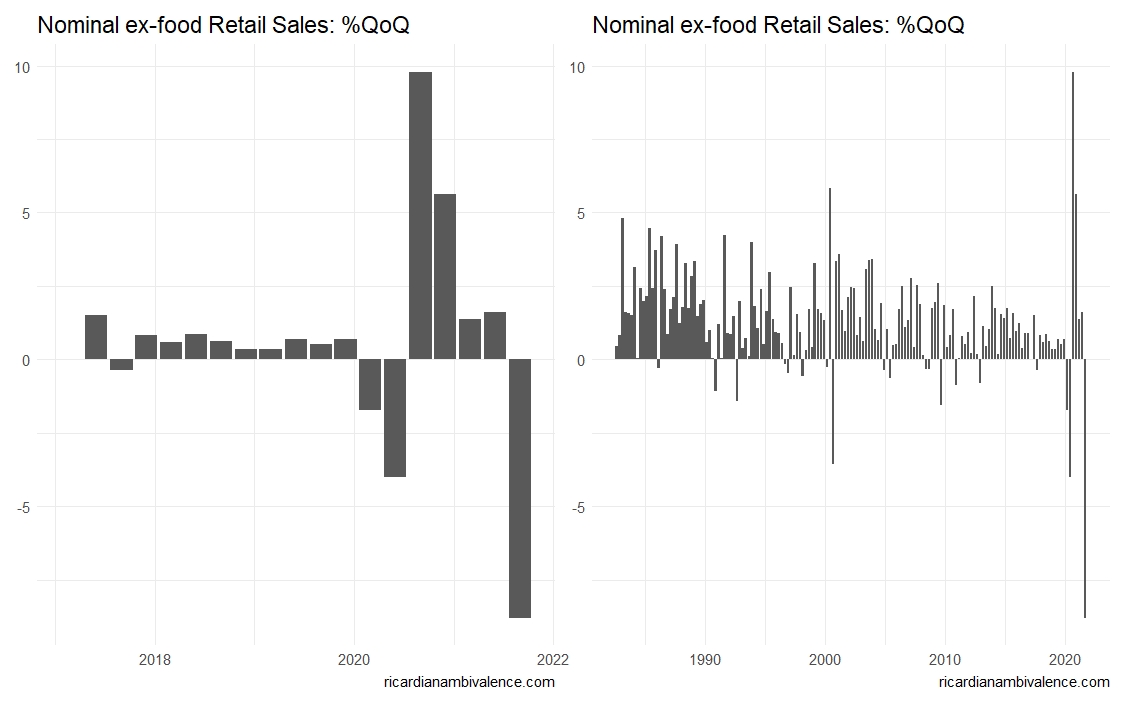

We’ve seen the leading edge of this unwind in the July retail sales data. The 2.7%mom decline in July, following a 1.8%mom drop in June, sets up Q3’21 for the worst every quarterly drop in retail sales. The charts below assume August is flat, which given what we know about lockdowns is way too generous. However I made that assumption to make the point. The retail situation looks terrible. This is consistent with the uptick of job-shedding in NSW in July.

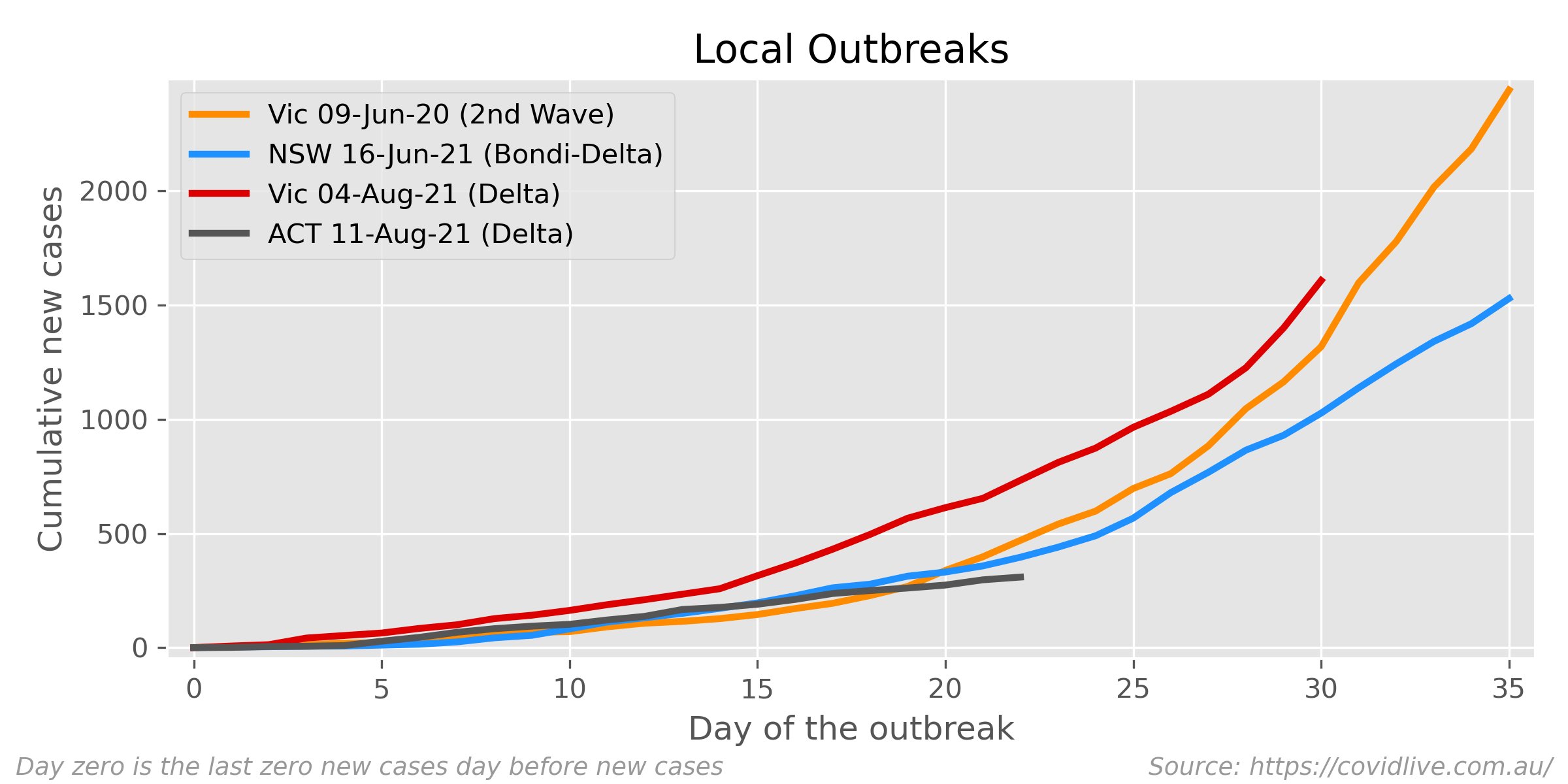

The reason is obvious: it’s Delta. Around 60% of the economy has been locked down. The Victorian experience with Delta shows that it’s very hard to stop with lockdowns (when measured against the NSW Delta outbreak, and Victorian second wave in 2020, the current Victorian path is worse; chart courtesy of the excellent Mark the Graph). That means the only path out of lockdown is vaccination. It also means that it’s very likely going to spread to the rest of Australia.

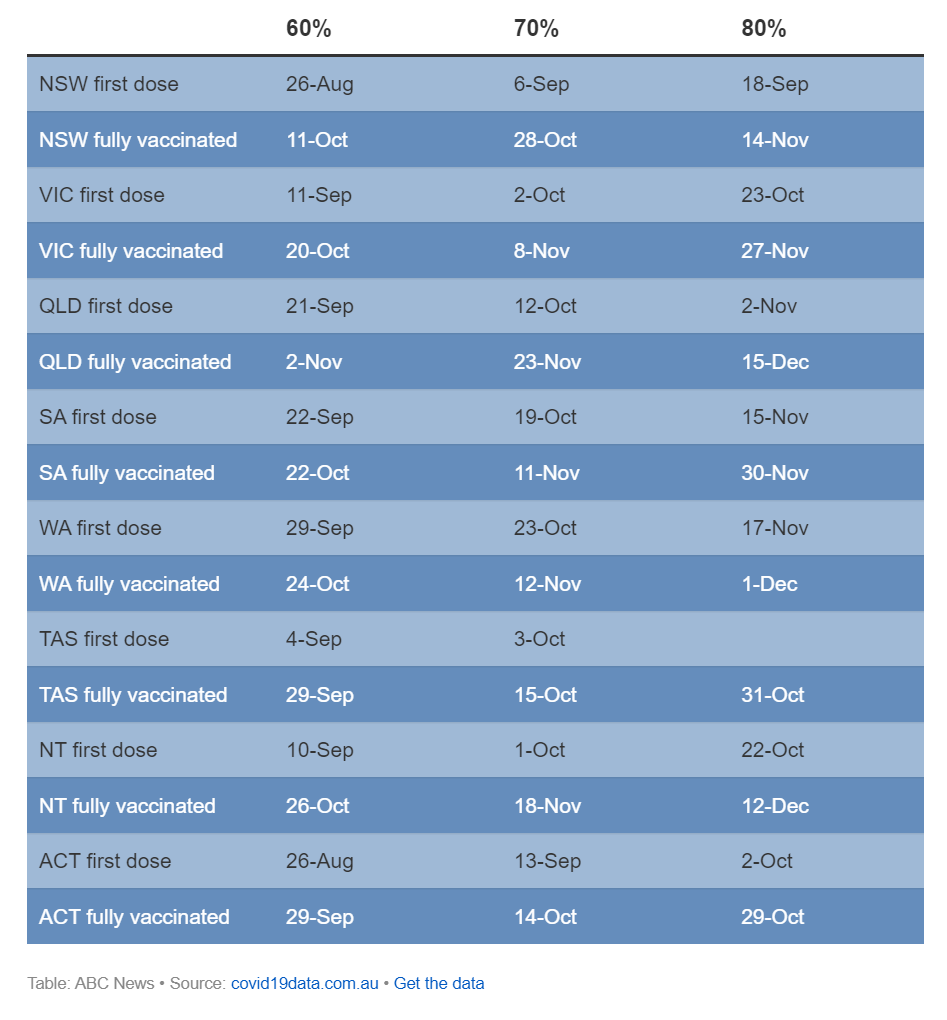

Given current vaccination rates, lockdowns should start to be relaxed sometime in Q4 (table below). There will be some relaxation in September, but for so many people the real game-changer will be the resumption of school-at-school. This is scheduled for late October in NSW (no date has been set for Victoria). Both NSW and Victoria are on track of 80% double-vaccinated in November. My guess is that the level of activity will start to lift modestly in November and more sharply in December. So the recovery should begin in the second half of Q4’21.

The ‘endemic COVID’ recovery will probably be a bit more subdued than the post-COVID bounce in H2’20. The experience in highly vaccinated nations overseas suggests that health capacity might be a bit of constraint. Indeed, with new stories about hospitals briefing doctors on ethical challenges arising when they allocate ICU capacity circulating, my guess is that some people will simply remain more cautious.

Summer should help get case numbers down and people out of their homes, but I’d expect some voluntary restrain from the vulnerable until it’s clear that things have settled down and hospital capacity is normal.

All told, this should deliver GDP growth of ~1%yoy in Q4’21, which is 300bps below the RBA’s 4%yoy forecast in the August SOMP. And while growth in 2022 will be strong (around 7%yoy for Q4’22), the reason for the strength is the size of the hole in H2’21. The level of activity is likely to be below the August SOMP baseline forecast until 2023.

What can the RBA do?

The RBA says that the QE policy is flexible, and the pace of purchases is under review in light of economic and health outcomes. It’s clear that health outcomes have been worse than they expected (they didn’t have a Victorian lockdown in their numbers), and while Q2 was a touch better than they’d expected (despite the Victorian lockdown) H2’21 is going to be worse than forecast.

It ought to follow that the RBA are going to ease policy by increasing the pace of bond buying — or at least not tapering to 4bn/wk.

That’s what I had thought in August.

But I now think it’s more likely that they’ll pre-commit to holding the pace of QE at 4bn per week until at least February (essentially making the November decision early, something they’ve done a few times in the 2021). There’s actually not much difference between the two policies.

Following the August meeting, we learnt that the lags in monetary policy were an impediment to easing. First, the excellent James Glynn reported that RBA Board member Harper said “all you would be doing is pouring lots of fuel into an open carburettor” if you eased. Governor Lowe repeated the same sentiments in more academic language at the House Economics Committee, and the August minutes also emphasized the lags in monetary policy when they discussed easing.

The bottom line from all this was that growth was going to be strong in 2022, and that the lags in QE meant that that was when the easing would likely have the maximum effect at that time.

Though H2’21 will be worse then they expected, base effects mean growth of 7%yoy in H2’22 is likely. So they could run the same argument again in September. The rising vaccination rates give them reason to be confident about the bounce.

However, I doubt this is the whole whole story.

Firstly, we’re talking about a relatively small quantity of bonds. The evidence for QE is so loose that you couldn’t say for sure that an extra 10bn of bond buying in H2’21 would have any effect on 2022. Also, according to the RBA (and most academics) it’s the stock that does the work. So if precautionary easing in H2’21 turned out to be more than was required, they could taper faster in 2022 to land at the same stock of bonds by mid’22.

Clearly there’s some impediment to doing so — because that’s not what they are saying (or doing).

I think they are worried about their footprint in the ACGB market. They are already distorting things, particularly in the short basket (Nov’24 to May’28). This makes an acceleration, at least in ACGBs, hard to see. The AOFM is currently issuing only 2bn of nominal Bonds per week, and probably want to tap up the Nov’32s, so supply isn’t going into the BPP sector to ease the squeeze (or at least not yet).

Under either of the likely scenarios, the RBA’s share of the bonds they do buy (April 23 to May’32) will rise to around 50% by mid 2022. I think the most likely outcome is that they ‘pre-commit for November’ (buy at 4bn/wk until at least Feb’22), in which cash their share of the sectors they buy will rise to ~50%. Under the ‘pushback the taper’ (5bn/wk to Nov and then taper to 4bn/wk) scenario, it rises to ~51%.

So there’s little difference between the two policies.

Holding the taper and pre-committing to buy at 4bn per week until at least February 2022 also has advantage of being better for their pride (and I do think this matters).

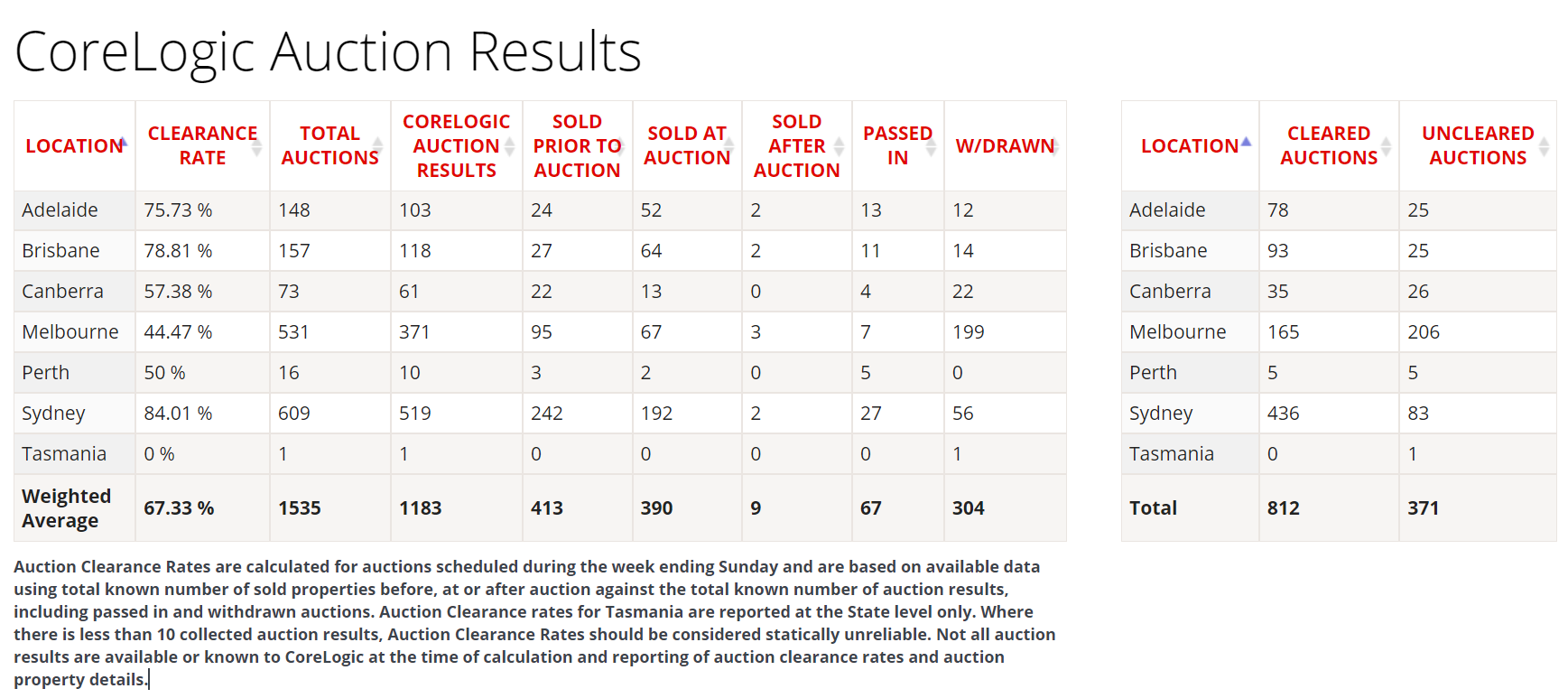

Finally, housing seems to be an impediment. There was a change to the August post-meeting statement to say that housing IS under scrutiny. Auction clearance rates outside of Melbourne holding up just fine (you can’t do physical house inspections in Melbourne). So I don’t see anything that would reduce the RBA’s concerns about housing.

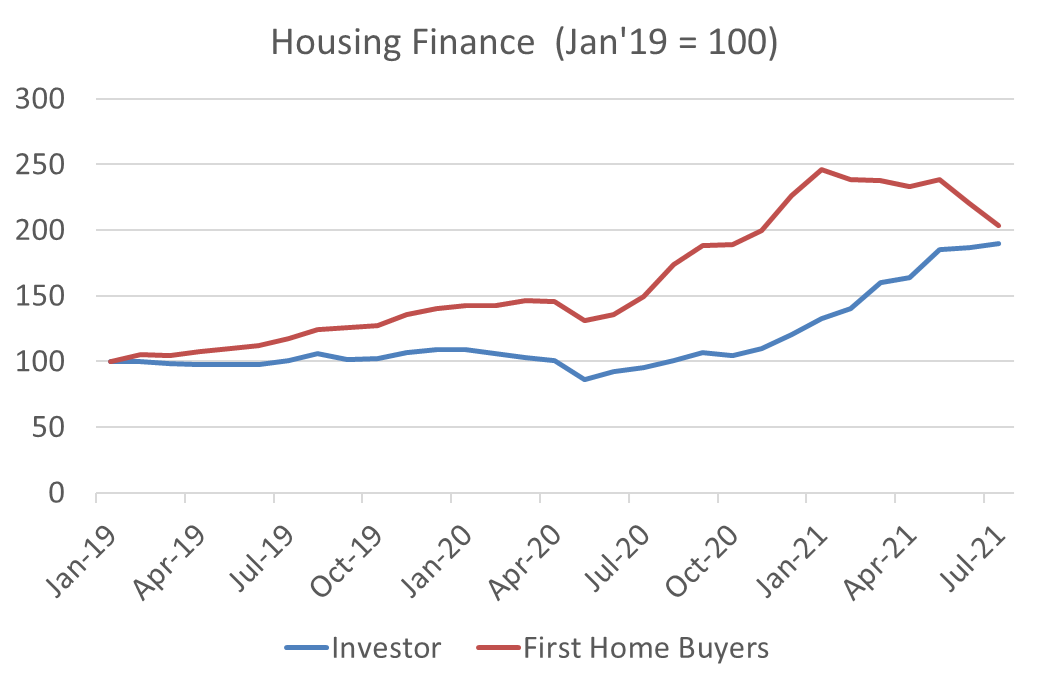

If anything, housing information is getting more concerning. The handoff from first home buyers to housing investors would be most unwelcome by the Bank. Experience in other jurisdictions suggests that this portends trouble.

Conclusion

In conclusion, the most likely outcome of the September RBA meeting is them pre-committing to 4bn per week until at least February 2022. I think this ~50%.

Pushing back the taper, and holding at 5bn per week until November is a 30% chance; doing nothing is a 15% chance; and accelerating to 6bn per week is a non-starter due to capacity problems (5%).

Re-designing QE is something they should do, and they could deliver an acceleration if they did so — but it seems too soon. And there are no speeches announced for right after the meeting, so i don’t think it’s happening this month.

In the case they do deliver an acceleration, increasing the proportion of Semis to 30% is probably the easier change. Though I think they need to at least start allowing the envelope to roll with the calendar, which would mean buying out to mid’33 right away.