Gov Lowe’s opening statement to the House of Representatives standing committee on Economics seemed to stick in his mouth a little. I imagine that it was a bit harder to say “she’ll be right, mate” today, with lockdowns being extended to regional NSW, and re-started in Victoria in the last 24 hours. The hole in Q3’21 GDP keeps getting bigger.

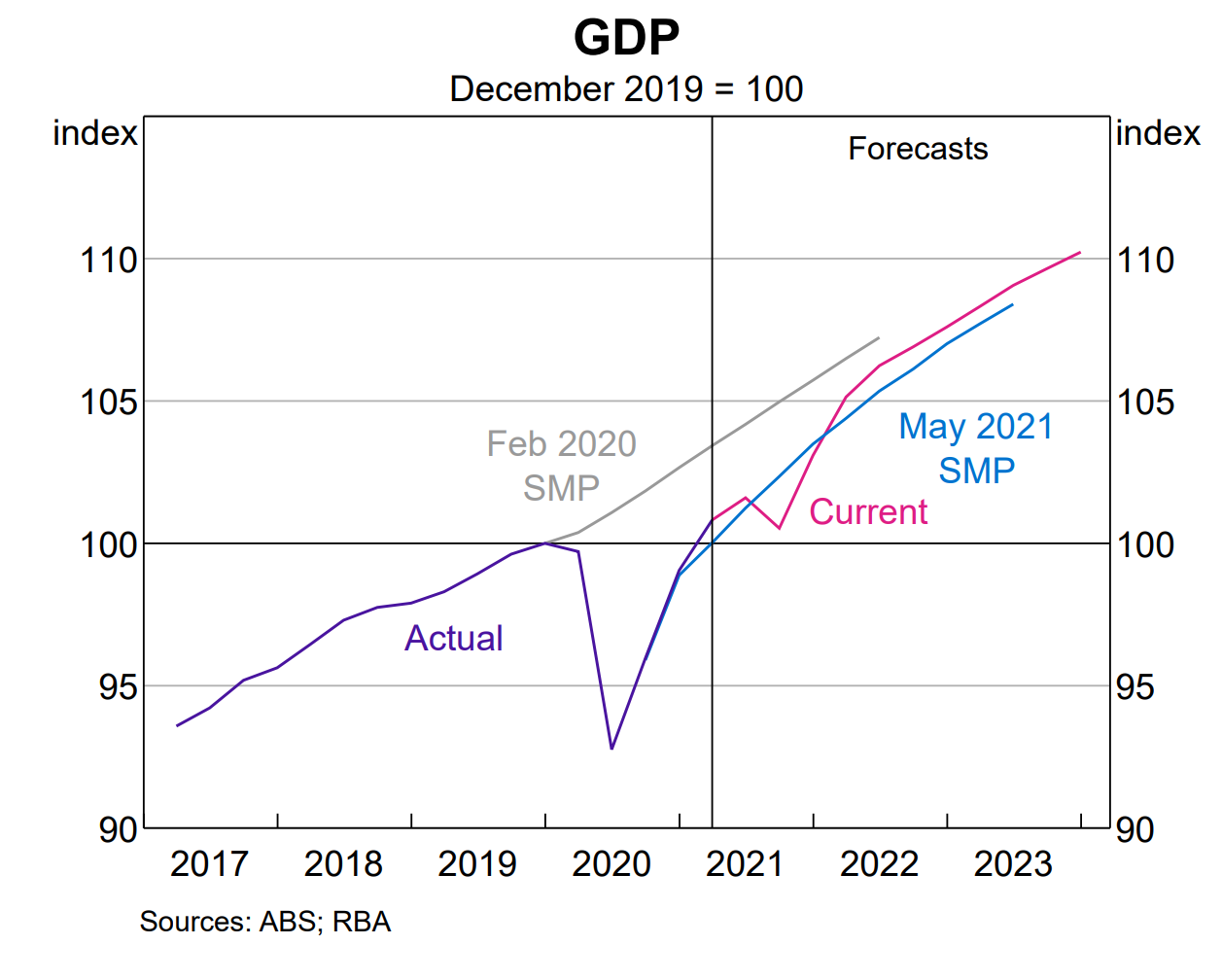

Still the Governor’s opening statement was basically a summary of the August SOMP, and those forecasts were (largely) set last week, so there was minimal wriggle room. The short summary of the August SOMP is that the RBA retained much of the upgrade they were looking at when they decided to taper bond buying (by 1bn per week to 4bn per week), but added a short-sharp contraction in Q3 due to the current lockdowns.

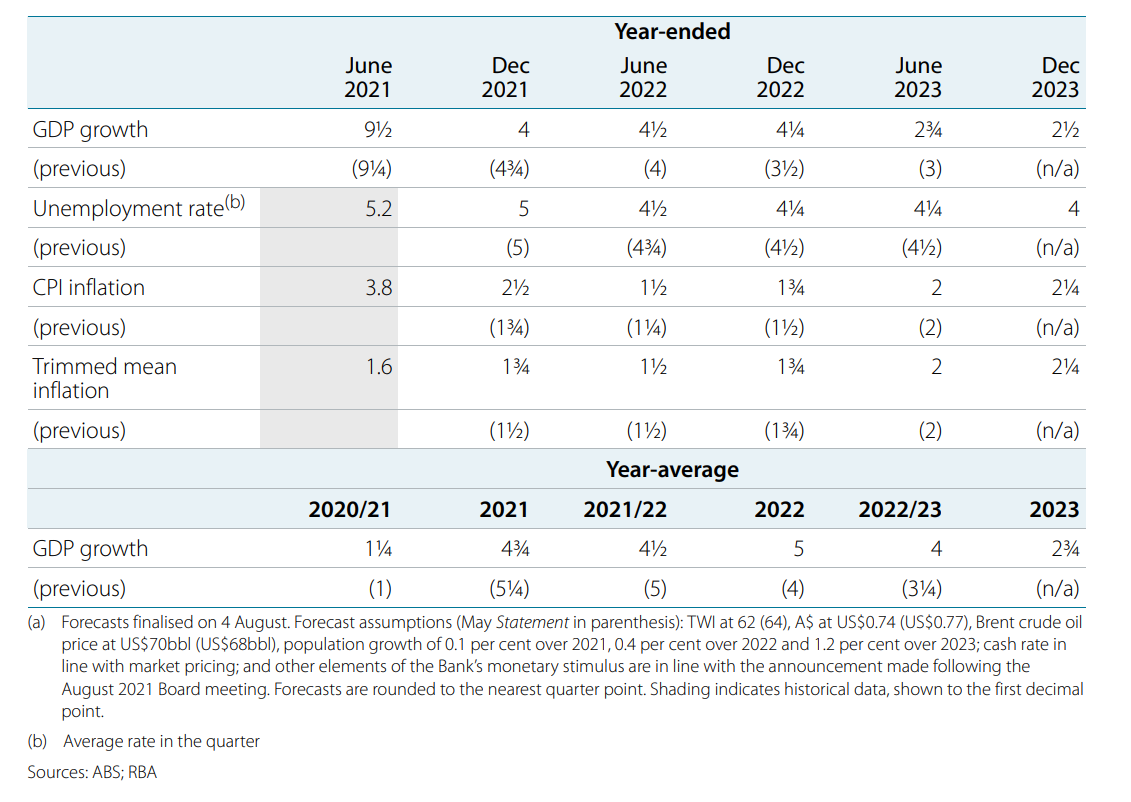

The upshot of all this is that the unemployment rate is a touch lower in 22/23 (by 25bps in both Q2’22 and Q2’23), and declines to 4% in Q4’23. The lower level of unemployment means that trimmed mean inflation is a bit higher. Trimmed mean inflation now hits 2% in mid-23 (it only rounded up to 2% in the May’21 SOMP, but was a touch below) and continues to rise to be a touch above 2% in Q4’23.

This is the key reason that the RBA didn’t want to loosen monetary policy by deferring the tapering of their bond-purchase program (by 1bn/wk, to 4bn/wk) in August. As far as they are concerned, their forecasts are on track to hit their targets — which means that monetary policy is appropriately calibrated.

These forecasts will have to be downgraded to get an easing. I think that’s possible — but it’ll take a while for the data to make the case (absent a larger COVID shock).

Gov Lowe’s opening statement to the House of Rep shed some light on what happened during the taper-debate at the 3 August board meeting. His explanation was that the lags in monetary policy meant there was little point in easing. Their expectation that the economy would quickly recover from the current lockdowns, and the lags inherent in monetary policy transmission, meant the main impact of a policy change would have been felt too late. Board member Harper said as much in his interview with the WSJ, where he said “all you would be doing [by deferring the taper] is pouring lots of fuel into an open carburettor”.

This rings a bit hollow to me. Australian GDP is about 2.1tn per year (and growing). Buying an extra 10bn or 20bn of bonds (less than 1% of GDP) would had an almost indistinguishable impact on the RBA’s economic forecasts. After undershooting for so long, are they really so worried worried about causing too much inflation that they can’t give a little confidence boosting tap?

The main value of a policy tweak would have been to show that the RBA remains ready, willing, and able to help during the pandemic. The RBA’s behaviour in 2020 was both responsive and aggressive. Not easing, against market expectations, in response to the current pandemic is a change of behaviour.

This change of the RBA’s reaction function is a reason to be cautious about the recovery. The RBA’s assumption that the recovery will be vigorous in Q4’21 is a key part of the reason they didn’t dump the taper in August. The H2’20 recovery was very vigorous and far in excess of staff forecasts. However, as often happens, the RBA may have over-corrected and now swung to the optimistic side.

The recovery in H2’20 had a tremendous tail-wind from housing. A house price boom caused by record low interest rates (particularly fixed rate specials) and a house building boom caused by both low rates and targeted fiscal stimulus spilled over the to the rest of the economy. The feeling that things were good created a self-reinforcing virtuous cycle that spread outside of housing markets. That’s not going to happen again.

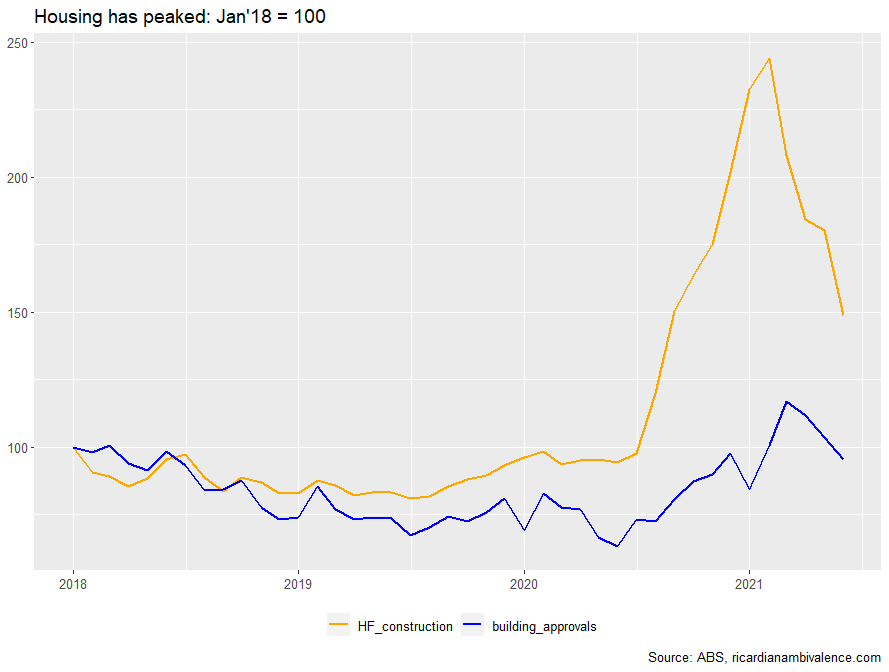

This time, house building is slowing and house price appreciation appears to also be slowing. The end of fixed rate specials mean that mortgage interest rates are rising, and macro-prudential policies to slow the housing market are more likely than a loosening of non-price conditions (Gov Lowe suggested they were coming in QnA).

Finally, there’s little capacity (and no political appetite) to repeat the targeted fiscal supports for house building. Both Housing Finance and Building Approvals are declining, and look set to decline further. The number of loans granted to first home buyers is down 15% since the Feb’21 peak (buying your first home drives retail spending).

The bottom line is that we should expect the recovery from the Q3’21 lockdowns to be a little more subdued. The housing market is likely to be a headwind this time. Also, retailers report that people aren’t buying like they did in 2020 (they are lobbying for a return of JobKeeper).

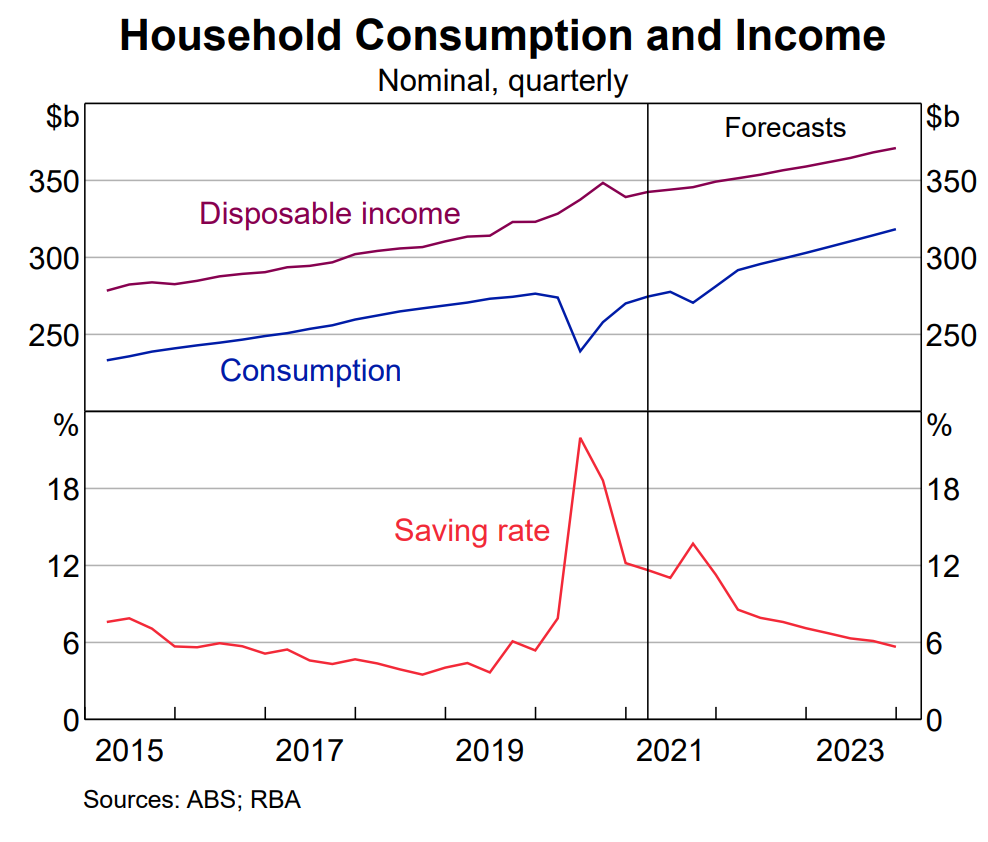

The lack of JobKeeper is an important change. It may have been wasteful, but the waste was stimulatory. As you can see from the below chart, the Q2’20 recession was very unusual, in that disposable income rose even as GDP contracted sharply. This won’t be repeated in Q3’21.

The disposable income boom in Q2’20, and the halo effect from housing, are a big part of why the economy did so well in the prior recovery. So if you have based forecasts for the next recovery on the prior recovery, I think you’re likely to be disappointed.

Looking forward, it’s possible that the RBA will use the flexibility in their bond purchase program, to buy more bonds — but it seems remote. Either the health situation is going to have to get really bad; or they are going to have to be persuaded by the data that the recovery isn’t going to be so good. The latter could take some time.

Finally, there were a few answers that encouraged my hunch that the capacity of the bond purchase program is on their mind. In QnA, when speaking about the possibility of accelerating the bond purchases, Gov Lowe said that “there is a limit to how much you can do that”. Similarly, in answering a question about winding down the CLF, Gov Debelle said they “don’t want banks holding all the bonds”.

2 comments

Comments are closed.