The RBA’s August decision didn’t stack up for me. The virus is uncertain, so the risk management decision was to delay the taper and continue buying at 5bn per week until things with the Delta/COVID outbreaks clarified. The RBA’s view of how QE works is that it’s the stock of bonds that does the easing, so it would have been simple to course-correct by tapering at a later date if a larger stock of bonds was felt be ultimately undesirable.

The fact they didn’t suggested to me that there were costs of easing that they wanted to avoid. The two issues I can see are: 1/ the RBA’s growing footprint in the ACGB market (which can be fixed easily enough); and 2/ The hot housing market (which really should be managed by macro-prudential tools). Of course, it might have just been inertia.

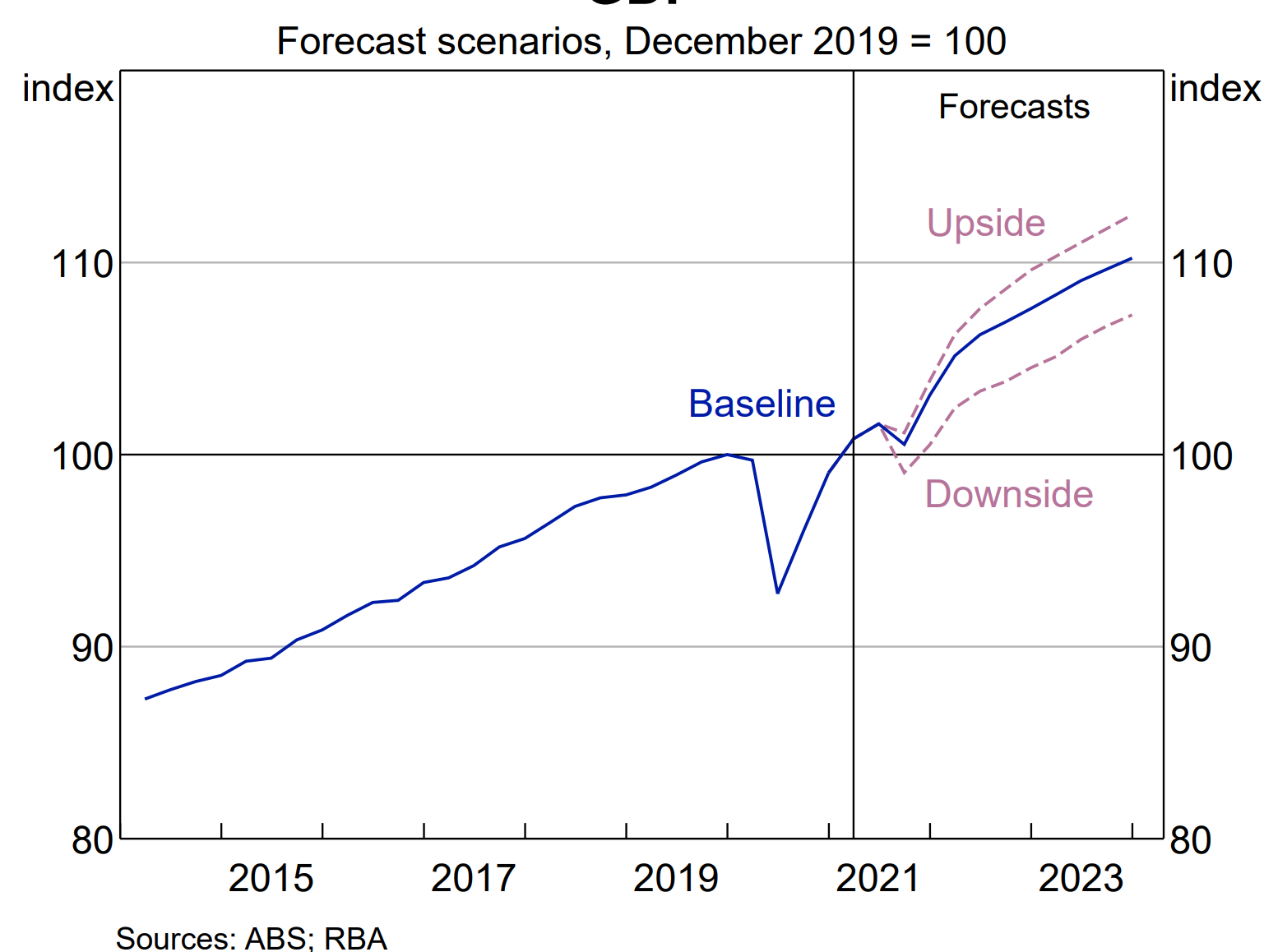

Not that they justified inaction in those terms. Instead, they used optimistic forecasts. The staff produced forecasts that had a small dip in Q3’21 (down ~1%qoq), and a strong recovery in Q4’21. They hung onto most of the upgrade from the stronger than expected Q1’21, and produced a GDP profile that is a bit above the May’21 SOMP baseline. This base case assumes ‘limited further lockdowns’.

There are now significant additional lockdowns.

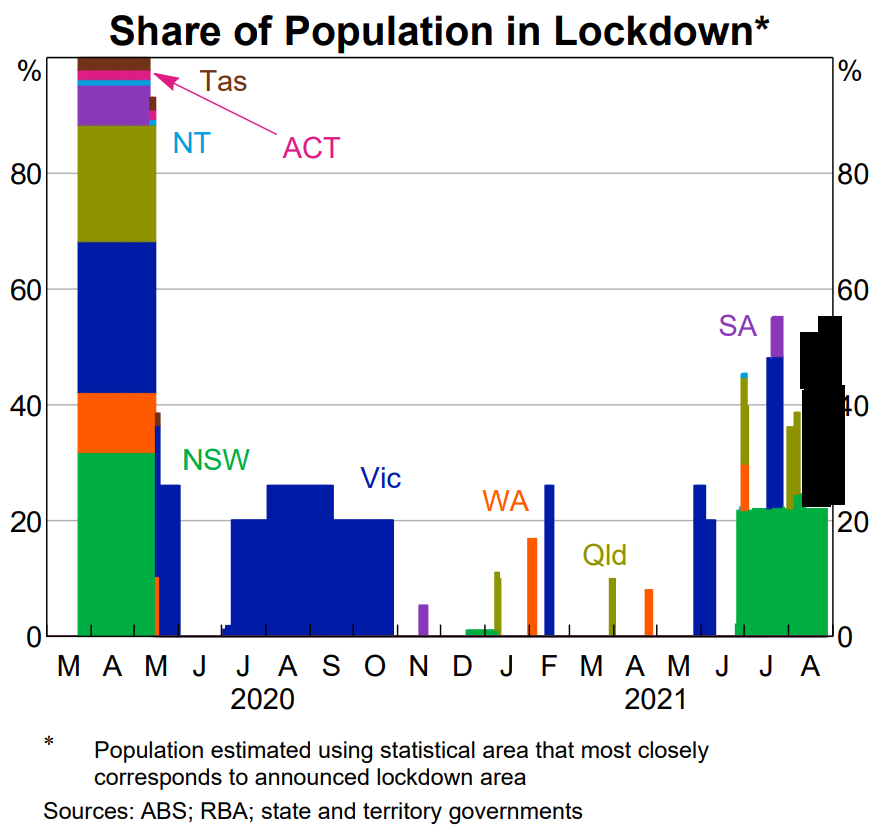

With all of NSW now in a snap 7-day lockdown, fines & compliance measures being tightened (meaning the economic consequences are larger), the NSW Premier saying we’re less half-way through the current episode (which puts re-opening in October, at the earliest), media reporting that the Melbourne lockdown will be extended for ‘at least another two weeks’, and even the ACT in a snap 7-day lockdown, it is straightforward to say that the Australian economy is currently operating below the base-case in the RBA’s August SOMP. [Update: the Victorian lockdown has been extended to 2 Sep + a curfew from 9pm to 5am has been announced; ACT has extended their lockdown for another two weeks; Darwin, Palmerston and Catherine have also been placed in 3-day snap lockdown due to a local case].

The SOMP included a nice chart showing the lockdowns to date. I’ve updated it (below) for the Melbourne, Brisbane & regional NSW lockdowns (Brisbane went in and out, regional NSW went in piecemeal until a snap 7 day lockdown of the entire state started on 15 August). It’s not supposed to be pretty (or 100% accurate) — it’s supposed to give you a feel for how much worse the situation has become in the last two weeks. It’s a little over twice as severe as the RBA expected.

But is it enough to get the RBA to act?

My judgement is that if they downgrade to something like their downside scenario, the RBA will push back the taper (holding bond purchases at 5bn per week until at least November) at their September meeting.

During QnA at the House, Gov Lowe said that lockdowns depress consumption by about 15 per cent. We can use this to guesstimate their revised Q3’21 GDP number.

Assuming that NSW is locked down for all of Q3 (which is probably only true for Sydney), that Victoria is locked down for only one third of Q3, and that all other states have Consumption growth of about 0.5%qoq, Q3’21 GDP is shaping up to be about -2.75%qoq, which is 25bps below the RBA’s downside case. Another way of coming at this is to double the shock: the RBA said lockdowns had knocked 2ppts off GDP (from +1%qoq to -1%qoq); if we double the shock that puts GDP near -3%qoq in Q3’21.

Of course, there will be offsets from increases in inventories (stuff you can’t sell adds to GDP) — however I haven’t subtracted anything for the temporary halt to construction or other negative-spillovers, so I think that -2.75%qoq is a reasonable approximation.

This puts us squarely in the downside scenario (and approximately where I had GDP going into the August meeting). It follows that there’s a high and rising probability that the Board comes to a different decision with regard to QE at their September meeting.

Moving to the more qualitative, their downside scenario sure sounds a lot like the current reality. NSW + Melbourne is over 50% of the Australian population, and a larger share of the Economy. We don’t know about Q4 lockdowns, but all time record high numbers for NSW despite a seven week lockdown make Q4 lockdowns seem plausible.

A slower economic path than the one envisaged in the baseline scenario is possible if the spread

RBA August SoMP (p. 75)

of the Delta variant (or other new variants of the virus) in Australia results in more extended

lockdowns than assumed. The downside scenario assumes that around half of the Australian population experiences rolling lockdowns during both the September and December quarters of 2021, and that a full opening of the international borders is delayed until later in 2022.

Of course it’s possible that they’ll hang onto their optimism and the rosy long-run forecasts, but I doubt it. Undershooting the published downside scenario, combined with the claim that QE is flexible and their assurance that the pace of purchases will be reviewed in light of the evolving health situation, makes it hard to do nothing.

If the the tool really is flexible, this is the time to show it.

Finally, I just can’t buy into the line from RBA Board member Harper, about how easing would be like ‘pouring fuel into a open carburettor’. Sustaining QE at 5bn per week for a bit longer would simply bring forward 10bn of bond purchases. A sharper taper later would put RBA asset holdings back on the prior path, if it proved to have been unnecessary. And the available evidence suggests that an extra 10bn of bond purchases would have little impact on the economy.

Let’s see what we discover in the minutes …