The Anika speech is often a pivotal speech for the RBA. They used it to signal the November easing in 2020, and the 2021 speech was used to deliver three key messages to the market.

Those messages are that the outlook for QE is further tapering, that they want CPI near 2.5% before hiking and that the market is wrong in pricing rate hikes in 2022 and 2023.

1/ The pace of QE will be tapered in Feb’22.

The decision to continue purchasing bonds at 4bn per week until February was characterised as an increase that provided some insurance against downside risks. When they next make their decision the economy will be in the sharpest phase of the recovery from Delta — so it’ll feel really strong.

The only decision will be how much to taper. My guess is that they’ll trim 1bn, to 3bn per week, but it could be a sharper reduction. There’s more risk of a 2bn taper than none at all.

2/ They are aiming for 2.5%

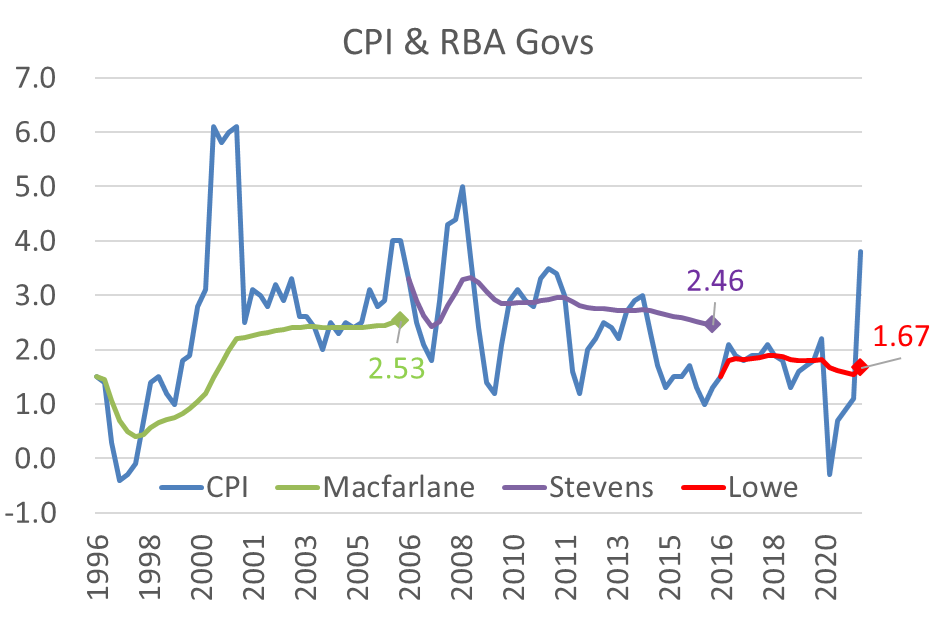

Yesterday Gov Lowe confirmed that he was aiming for the mid-point of the 2% to 3% target band before raising rates. This might seem obvious, given the 2% to 3% target range, but it wasn’t (I’ve been using 2.25% in my models). Lowe’s historical tolerance of low inflation, and preference for blurry language such as two-point-something, had made people think he would move early, especially against the backdrop of rising house prices.

Yesterday we learnt that he would not do that.

the Board has said that it will not increase the cash rate until actual inflation is sustainably within the 2–3 per cent target range. It won’t be enough for inflation to just sneak across the 2 per cent line for a quarter or two. We want to see inflation around the middle of the target range and have reasonable confidence that inflation will not fall below the 2–3 per cent band again.

RBA Gov Lowe: Delta, the Economy and Monetary Policy

Up to now, Gov Lowe has simply said that 2.1% wouldn’t do the trick, and emphasised that wages growth above 3%yoy is required to make him confident that inflation above 2% will be sustained. The 2021 Anika speech is the first time he said they need CPI to be ‘around the middle‘ of the target range before hiking (he went some of the way there in QnA following the August 2021 House of Reps testimony).

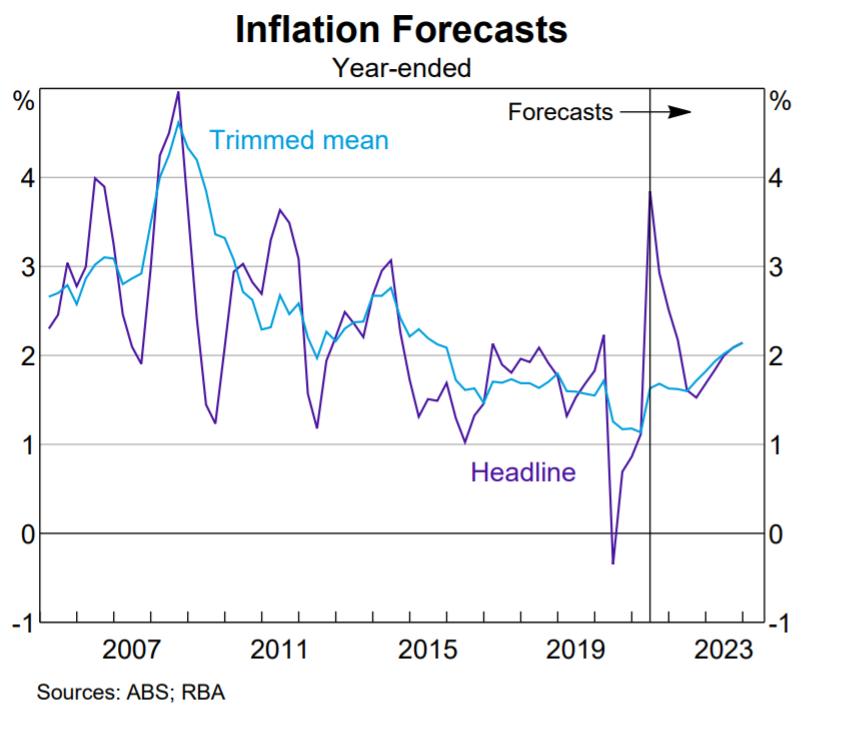

If you look at the August SOMP, you can see while inflation rounds up to 2.25% in the forecast table, it’s still below 2.25%. If they are aiming for 2.5% inflation before hiking, that was unlikely to happen before 2025 even on the August SOMP forecasts (and these forecasts will likely be downgraded in Nov).

I wonder if Lowe’s legacy is starting to become a factor: his initial seven year term runs from September 2016 to September 2023 (he may have an option on a 3yr extension) and given his performance to date there’s little prospect of him ending with an inflation rate that has a two in front of it.

3/ Rate hikes are further away than you think

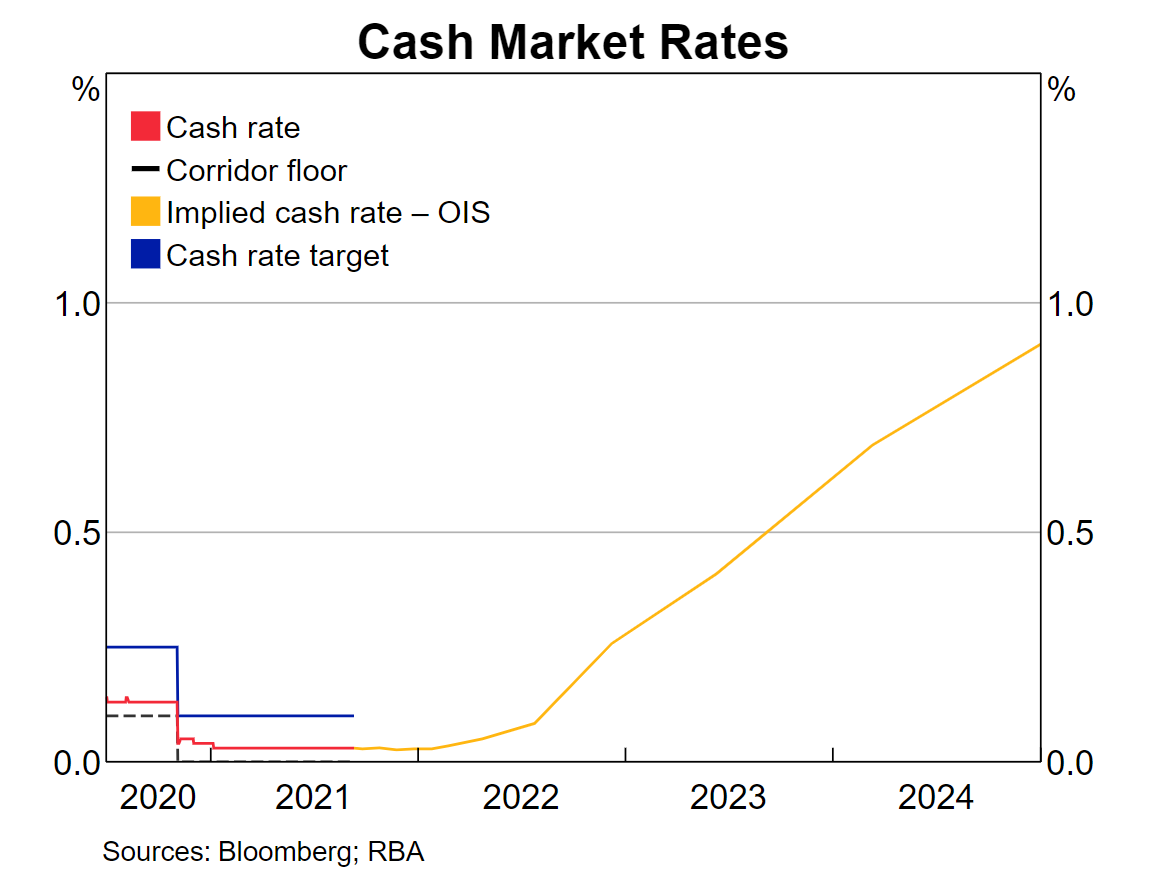

Gov Lowe made a rare comment on market pricing, saying that he he finds it difficult to understand why the market is pricing in hikes in 2022 and 2023.

This is closely related to the second point — that the target is 2.5%

One reason the market is pricing in hikes is because no one believes that Lowe’s really targeting 2.5% inflation. History shows us that Lowe didn’t care much about low inflation between 2016 and 2018 (partly due to rising house prices). Lowe also said that they won’t be raising rates to cool the property market.

Carry on?

The short end of the Aussie curve rallied following this speech and it can rally further. The RBA’s current forecasts have CPI barely above 2% at the end of 2023, and increasing only gradually at that time. Delta means those forecasts will be downgraded again in November. So the return to 2.5% CPI on the RBA’s own models will be delayed. The RBA’s historical forecast bias has been to over-predict inflation, so the risk is that it happens even later than 2025.

Personally, I find it hard to see CPI near 2.5% before 2025. All of which means that there’s plenty of value left in the short end of the Aussie curve.