The minutes to the RBA’s August meeting confirm that the Board did discuss reversing July’s decision to taper bond purchases to 4bn per week, and that policy remains under review. My guess is that they push back the taper in September, and maintain the pace of purchases at 5bn per week until things clarify.

The minutes lay out a two-part test:

1/ is the health news worse?

2/ will it delay the recovery?

The Board would be prepared to act in response to further bad news on the health front should that lead to a more significant setback for the economic recovery.

August’21 RBA Minutes

I think we can fairly confidently answer both questions in the affirmative.

The Health News is worse than expected

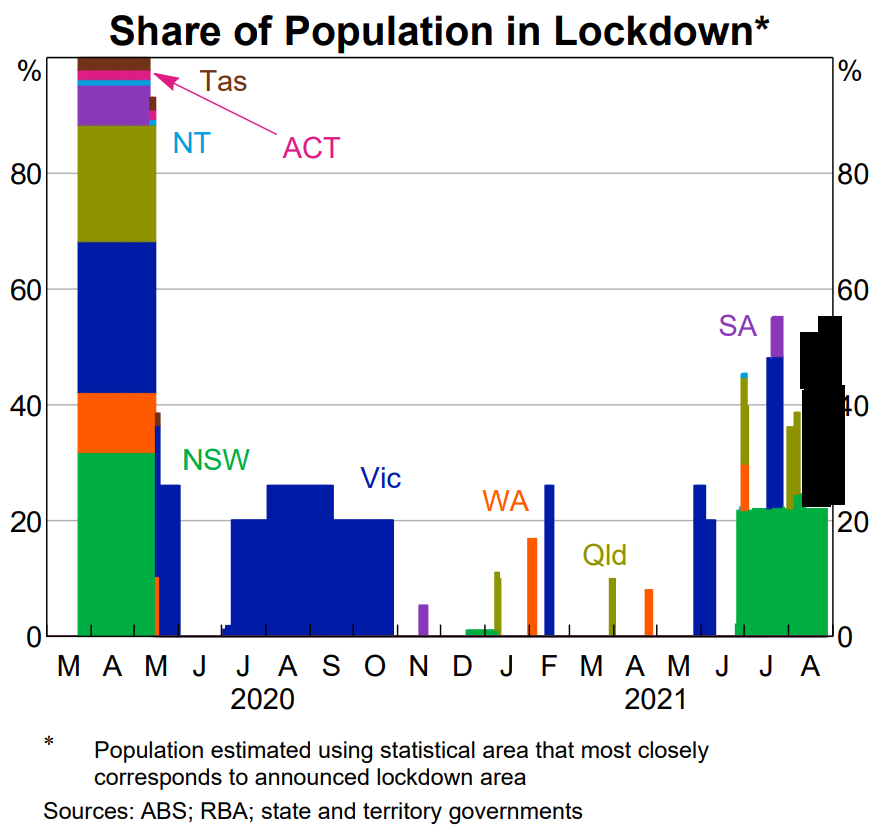

The forecasts in the August SOMP assume that only Greater Sydney would be in lockdown. Things are about twice as bad as they expected. Since they published the SOMP, South East Qld has gone into and out of lockdown; Melbourne went into lockdown and remains with it being extended their lockdown again and having further tightened restrictions; regional NSW was added to greater the Greater-Sydney lockdown; and the ACT lockdown went into a snap lockdown that was almost immediately extended for a further two weeks as the cluster grows.

Q3 GDP is on track for their downside scenario

Forecasting the RBA’s forecast is always hard (I got the August SOMP forecasts badly wrong, for example), but this time we have the Governor’s help. In Testimony, Lowe said that they subtract about 15% of consumption from the baseline when a region is in lockdown.

Given what we know about lockdowns, this gives us a ball-park estimate of -2.75%qoq for Q3’21 GDP. This is just below the -2.5%qoq that the RBA had penciled in for their downside scenario.

The labour market is always more important to Lowe, but the minutes tell us that the labour market forecast is basically a function of “health outcomes and the duration of the lockdowns”. We know that health outcomes are worse than expected, and that the lockdowns are being extended (as Delta proves hard to control).

The much higher transmissibility of the Delta variant also gives a good reason to think that the eventual recovery might be more subdued. This is a risk that is highlighted in the minutes:

The high transmissibility of the Delta variant raised the possibility that a more gradual reopening of the economy in affected areas would be needed compared with earlier episodes of lockdown restrictions.

August’21 RBA minutes

Australia was previously on a high-confidence post-COVID-pandemic growth path. It will likely now be on endemic-COVID + vaccination (and booster) path. A recovery with endemic COVID must be associated with a higher degree of caution, which means lower consumption and investment.

That’s a real difference.

I have also argued that the initial recovery was flattered by the housing stimulus, and that the absence of this tailwind will make this recovery a little more subdued. Don’t buy the “still at a high level” shibboleth — if it’s peaked, and house building has peaked, there is no further growth to come from this source.

Will easing hit in time?

The lags in monetary policy seemed to be the main argument against easing.

Members therefore considered the case for delaying the tapering of bond purchases to $4 billion a week currently scheduled for September 2021. They noted that the outlook for the economy is for a resumption of strong growth in 2022. Members judged that any additional bond purchases would have their maximum effect at that time, with only a marginal effect at present, which is when the extra support might be required.

August’21 RBA minutes

This is always true. Monetary policy works with a lag.

What’s needed to overcome this obstacle is sufficient uncertainty about the outlook. If you can’t be sure about the recovery, you do the risk management thing.

There’s more than enough uncertainty to pass this test. The difficultly controlling Delta in locked-down areas, leakage into across geographies despite movement restrictions, and the re-introduction of (modest) restrictions even in highly vaccinated placed like Israel, all increase the uncertainty about the outlook.

Anyhow, the RBA tells us it’s the stock of bonds doing the easing — so if they buy too many bonds in H2’21, they can always taper a bit harder and get back on track in 2022.

Conclusion

It seems fairly clear that the two part test (worse health outcomes and a worse economic outlook) laid out in the August minutes will be met in September. I’d say that it’s a 75% probability (though some might note that’s what I thought after the July minutes!).

It’s not 100% as there are other confounding factors. It’s worth remembering that the broader QE policy-decision is driven by:

1/ The Economy;

2/ What other Central Banks are doing; and

3/ Market function.

Other central banks are closer to tapering, and market capacity in the ACGB market is a looming issue (buying more semis would help).

The likelihood that the RBA will buy more bonds, for longer, means that they should think carefully about the design of their QE program. For example, they have been buying out to May 2032 since the program started. Should the envelope roll out with the calendar? That’d be helpful.

But that’s the subject of another post …

2 comments

Comments are closed.