[This post is the second of two on RBA QE. This post has solutions to the problems in the first post]

The solution: moving out the curve.

Let’s assume that the RBA wants to ease.

The minutes to the July RBA meeting report that “members agreed that there should be flexibility to increase or reduce weekly bond purchases, as warranted by the state of the economy”.

The economy is worse than expected, there’s evidence that firms in NSW are shedding labour in response to lockdowns, and there’s good reason to think that an endemic-COVID recovery might be less vigorous than the post-COVID rebound in H2’20.

So this a live issue.

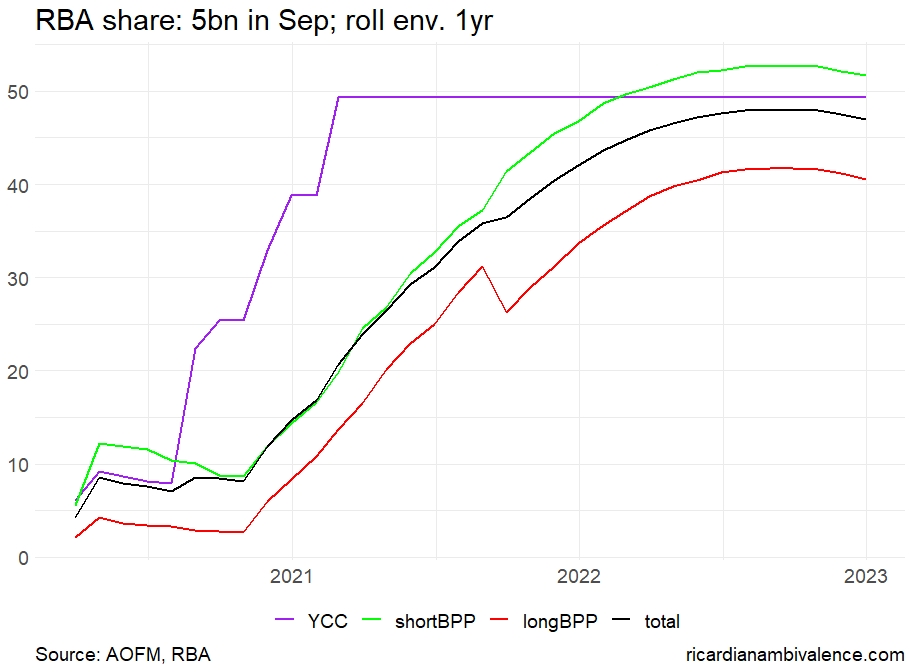

Let’s say that the RBA does this by pushing back their July taper, and sustaining the rate of purchases at 5bn per week at their September meeting (tapering 1bn per quarter starting at their November 2021 meeting). Peak concentration rises to 51% , with the RBA’s share of the problematic short BPP basket peaking at 54% (note: pre-commitment to QE at 4bn per week until February gives much the same result, with a peak concentration of 50% and a peak short BPP share of 52%).

A market share of 54% is too high. At that level, market function may become problem (as has occurred with the April 23s and April 24s).

The three part test the RBA originally laid out for QE was:

1/ Economy;

2/ Other Central Banks; and

3/ Market function.

So, the case for more QE may fail the original test on market-function grounds.

The RBA could fix this by simplifying their QE.

Buying across the curve would delay market concentration issues. Buying more Semis would further delay market concentration issues. Doing both would have the greatest impact: it would delay concentration problems and better align issuance patterns, in both ACGBs and Semis, with RBA purchases.

When QE was introduced in March 2020 (though this program was to stabilise the bond market), Gov Lowe said in QnA that there were no limits on what the RBA could buy. The RBA should use the flexibility they wisely gave themselves at that time.

However, change is hard. And such a large change might be too radical (until the next crisis).

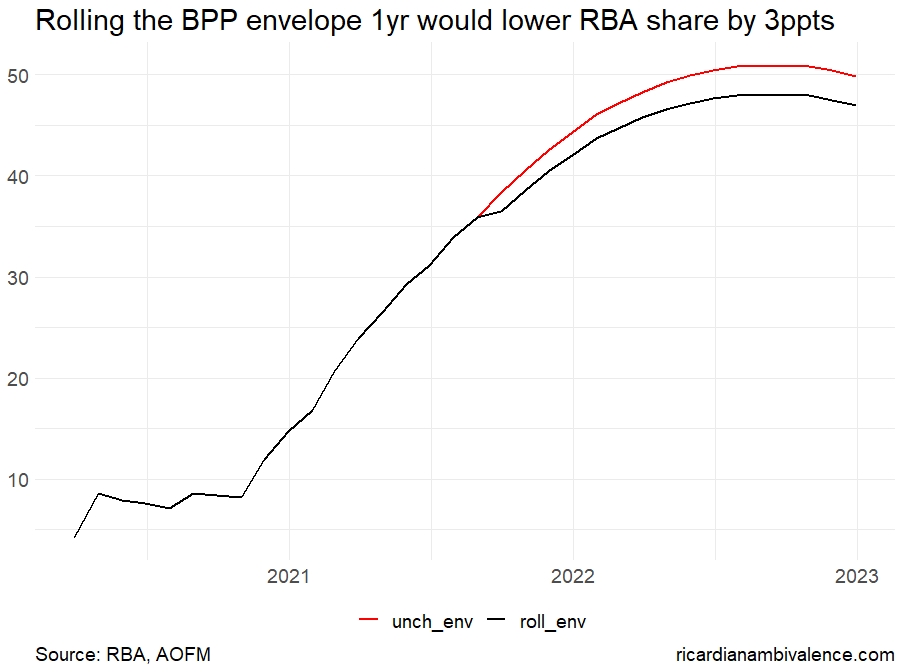

A more modest ‘fix’ would involve moving from a static to a ‘rolling’ QE envelope. The Bond Purchase Program is about a year old; and yet the longest bond remains the May’32. Rolling the long BPP basket out by a year, to the April’33 , would immediately add capacity.

Solution 1: Rolling the QE-envelope

If the envelope of QE rolled with the calendar, the short BPP envelope would soon extend to the April 2029s and the long BPP envelope would soon extend to the April 2033s. If we make this change, it adds ~30bn of stock to the QE-pool (plus some issuance) and the peak RBA share of the market falls by 3ppts to peak at 48%.

This does not solve all the problems. The concentration issues in the short BPP basket remain. The RBA already holds a large proportion of Nov’28s and Apr’29s, so the roll-down of those bonds into the short BPP basket doesn’t help. As a result, the RBA’s share of the Short BPP basket rises to 53%.

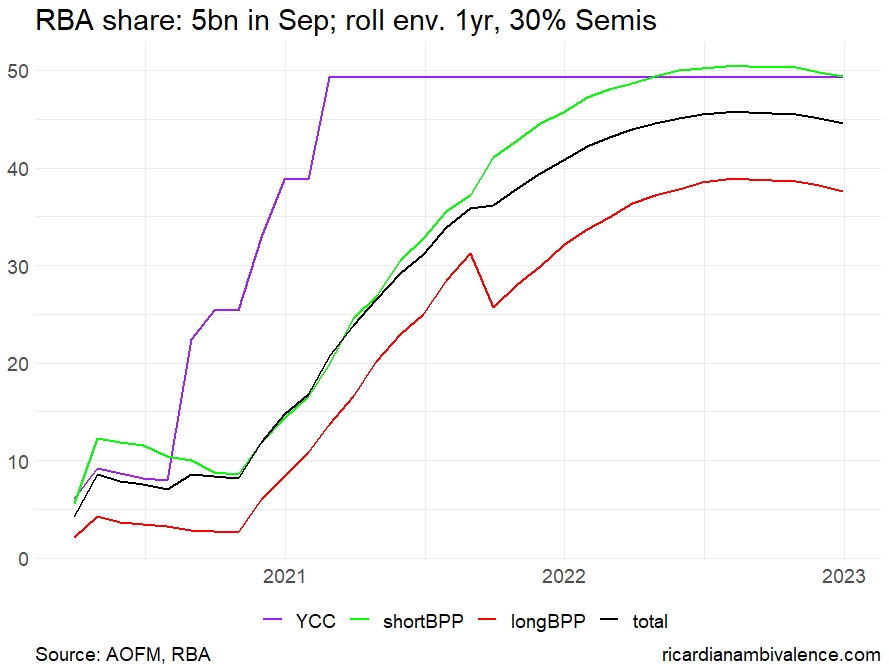

This could be fixed if the RBA lowered the share of purchases in the short BPP basket to 35% of QE. In this case, the RBA’s peak share of the short BPP basket does not exceed 50%.

But what should the RBA buy more of?

Solution 1B: boosting Semis to 30%

For a fixed QE program, there are only two ways of lowering the share of short BPP bonds in QE:

1/ Buy more of the long BPP basket bonds; or

2/ Buy more Semis.

I favour buying more Semis. Semis are about 30% of the combined Australian Government Bond market, so the current allocation of the RBA’s Bond Purchase Program is a bit underweight Semis (the RBA buys 20% Semis and yet Semis are just over 30% of the combined ACGB + Semi market).

The recent underperformance of 10yr Semis relative to bond also suggests that there’s more capacity in Semis than in ACGBs.

Assuming the RBA boosted the share of Semis in QE by 10ppts to 30% and that the 70% of ACGBs buying is split evenly between the short and long BPP buybacks, the RBA’s peak share of the ACGB market declines to 2ppts to 46%. The RBA’s share of the problematic short BPP basket declines 3ppts to a peak of 50%; and their share of the long BPP basket peaks at 39%.

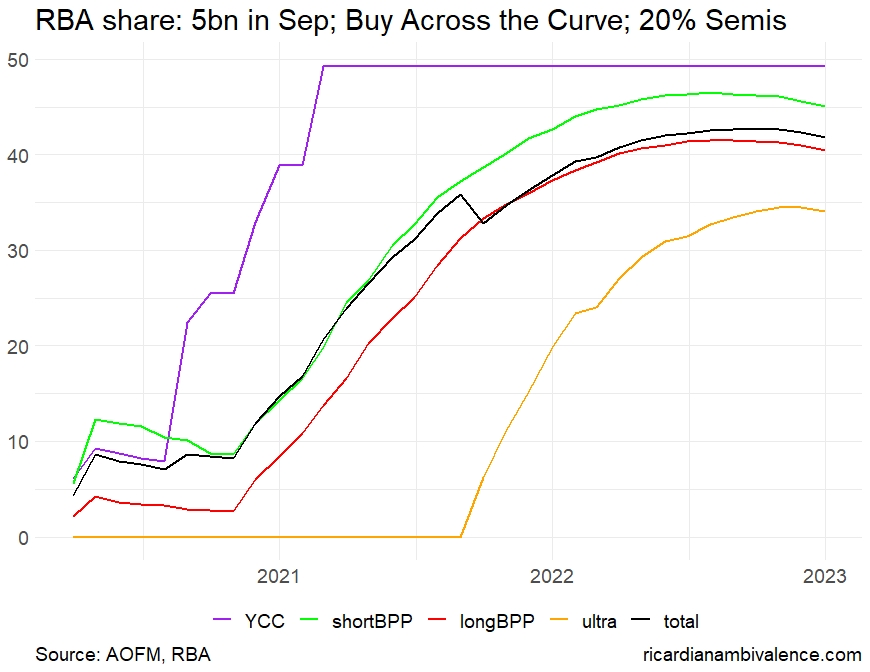

Solution 2: Buying beyond May’32

My preferred solution is for the RBA to remove the tenor cap on QE purchases and buy across the curve. Doing so would add maximum capacity to the RBA’s bond buying program and prevent the RBA’s share of the market (or of any particular subset of the market) from breaching 50%.

In our baseline, where the RBA delays the taper from 5bn until November, buying evenly across the curve (27% short; 27% long; 26% Ultras; + 20% Semis) means the RBA’s share of the short BPP basket peaks at 46%, their share of the long BPP basket peaks at 42%, and their share of ultras (bonds that mature after May’32) peaks at 34%. Their share of the total market (from the April 2023 bond) would peak at 43%.

This policy mix would both defer concentration problems and allow the RBA to ease further (if they wanted to do so).

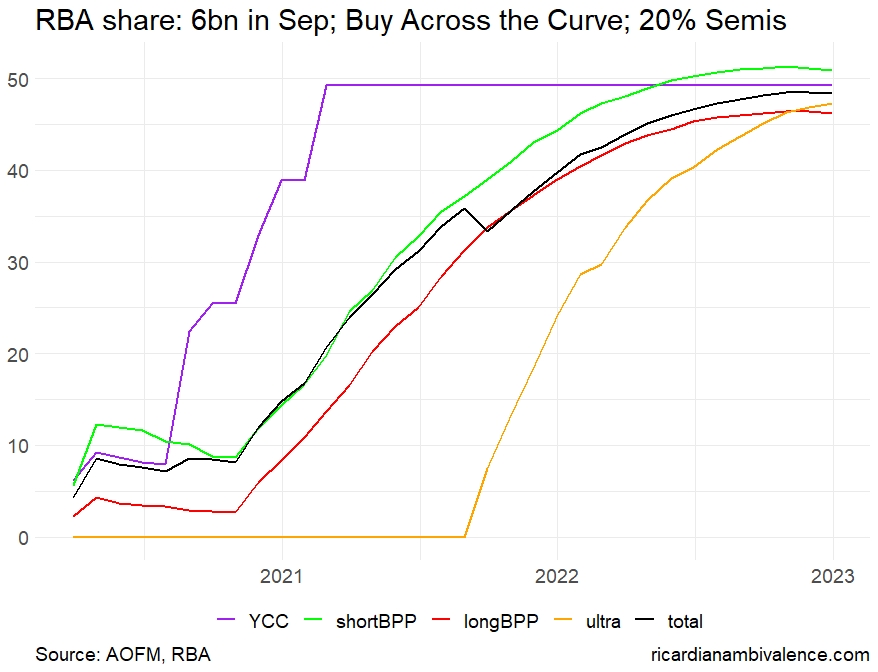

For example, if QE were increased to 6bn per week at the RBA’s September meeting, and tapered at 1bn per quarter thereafter, the RBA’s share of the short BPP basket peaks at 51%; their share of the long BPP basket peaks at 46%; and their share of ultras peaks at 47%. Their share of the market (from the April 2023 bond) would peak at 48%.

Solution 2B: boosting Semis to 30%

As discussed above, the relative performance of ACGBs v. Semis suggests that there’s more capacity in the Semi market than the ACGB market. A straightforward fix is to increase the share of Semis in the QE mix. This would align the share of Semis in RBA QE with the share of Semis in the consolidated Government Bond market.

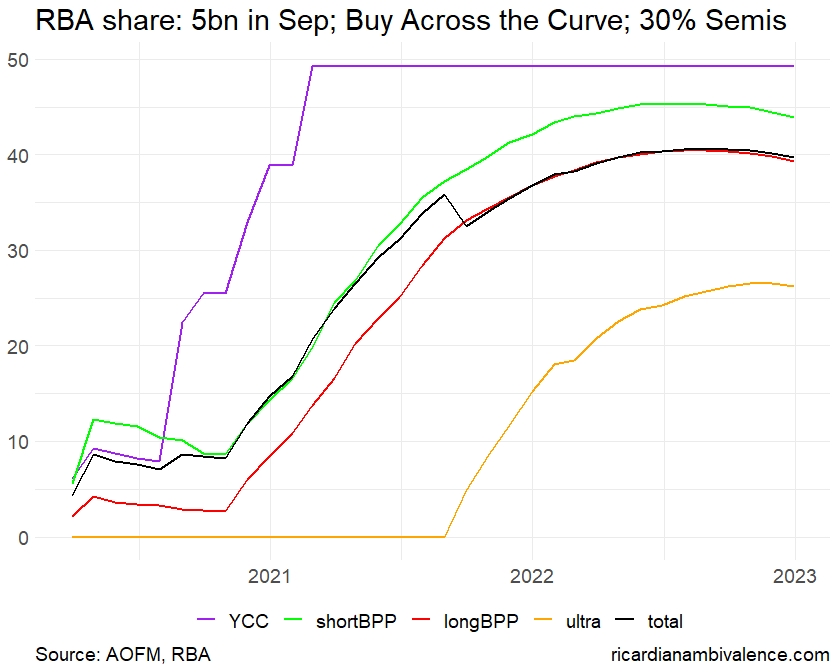

Assuming that the share of Semis is increased 10ppts to 30%, and that the RBA continued to buy at 5bn per week until November, the RBA’s share of the short BPP basket peaks at 45%; their share of the long BPP basket peaks at 40%; and their share of ultras peaks at 27%. Their share of the total market (from the April 2023 bond) peaks just under 41%.

As was the case above, this policy mix would both defer concentration problems and allow the RBA to ease (if they wanted to do so).

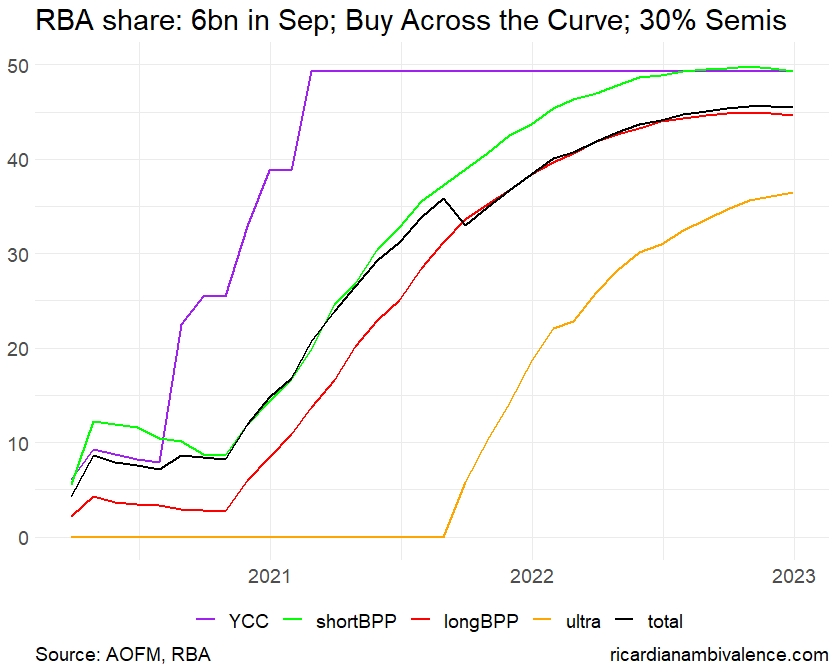

If QE were increased to 6bn per week at the RBA’s September meeting, and tapered at 1bn per quarter thereafter, the RBA’s share of the short BPP basket peaks at 50%; their share of the long BPP basket peaks at 45%; and their share of ultras peaks at 36%. Their share of the market (from the April 2023 bond) would peak at 46%.

Conclusion

The current design of the RBA’s QE program pretty much guarantees that any further easing will be some combination of extending out the curve in the ACGBs or buying more Semis. Probably both.

Extending the tenor of the QE envelope would better align RBA buying with desired issuance, particularly for the State Governments (Semis). Increasing the share of Semis would better align QE with the relative size of the ACGB and Semi bond markets. Doing either, or both, would push back the date at which market function becomes a constraining factor for QE.

Regardless of what you think about the case for easing right now, there a strong argument for the RBA to get ahead of these problems and to maximize both their easing credibility and the life of their tools. They need not do so at the September meeting, but maintaining QE at 5bn per week from September to November would make the issue more pressing.

The November 2021 RBA meeting seems a natural time to review QE. It’ll be a year since QE started and, particularly if purchases are ongoing at 5bn per week, it would make sense to at least roll the envelope out by a year, to adjust for the passage of time.

Regardless, the RBA should remind the market that it can buy across the curve, and that it may review the issuer-mix.

2 comments

Comments are closed.