I’ve riffed on the importance of housing to the H2’20 recovery, and how it’s peaked before. It’s fair to say I had a bit of confirmation bias following the weak Q2 Construction Work done release. Housing was a tailwind in H2’20 … however while house prices might keep rising, housing construction will do well to be flat in terms of it’s contribution to growth over the next year. This is a reason to think the rebound from this lockdown isn’t likely to be as vigorous as the RBA hopes (endemic COVID is the other main reason).

However, the Q2 CWD release is chiefly of interest for what it means about Q2 GDP, and particularly the RBA’s Q2 GDP forecast. Flat Private Dwelling construction is a big miss for the RBA, and will have lowered their tracking estimate of Q2 GDPe by ~30bps, to 0.4%qoq.

Allow me to explain …

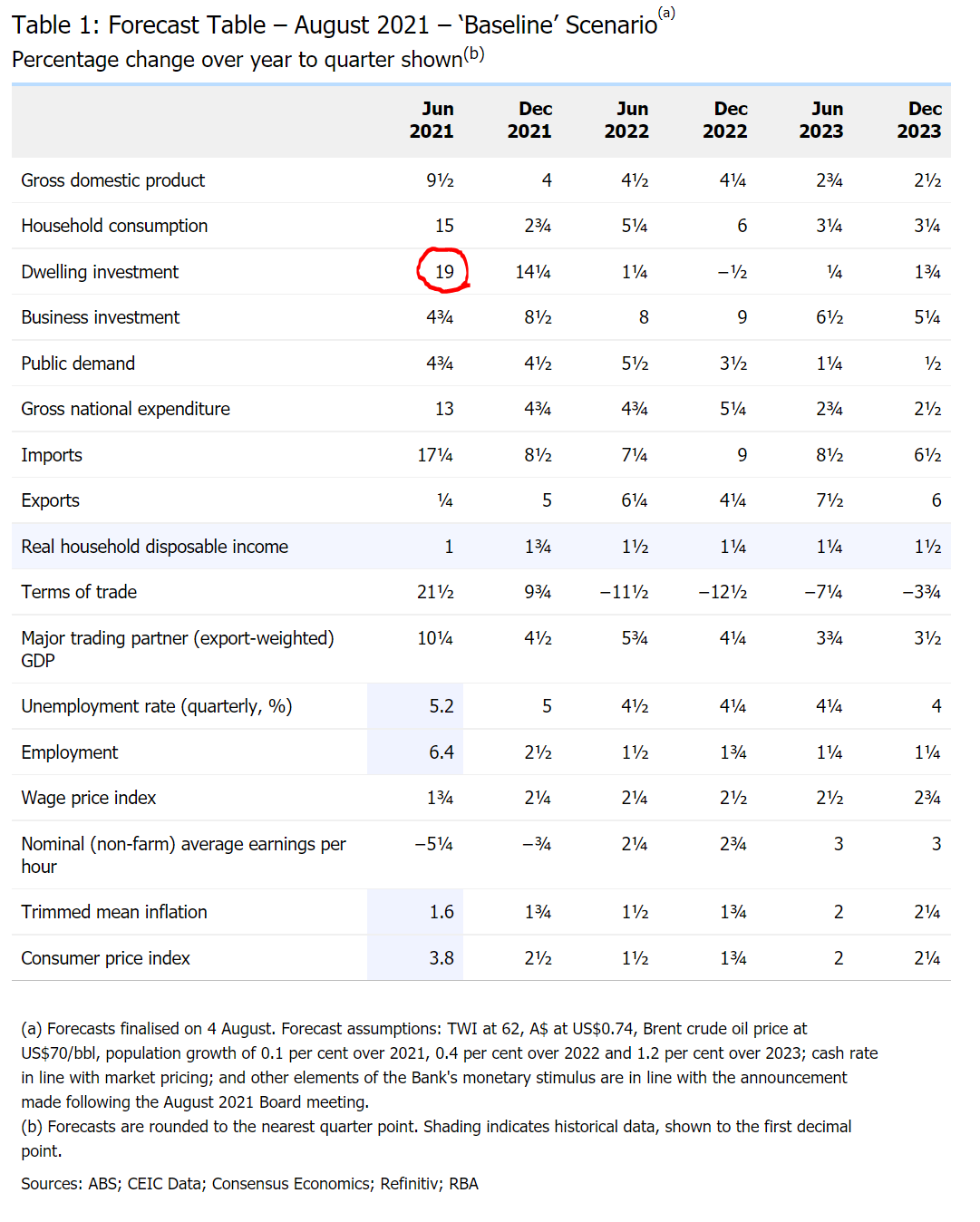

The RBA’s forecast of 9.5%yoy growth in Q2 equates to growth of around 0.75%qoq for Q2. Just under half of that 75bps of growth came from the assumption that Dwelling Investment would grow by about 5.5%qoq (Dwelling Investment growth of 5.5%qoq was required to hit 19%yoy). Private Dwelling investment is about 5.5% of GDP, so a 560bps miss (it fell 10bps in the Q2’21 CWD release yesterday) shaves 31bps off my tracking estimate of Q2 GDP (now 0.4%qoq).

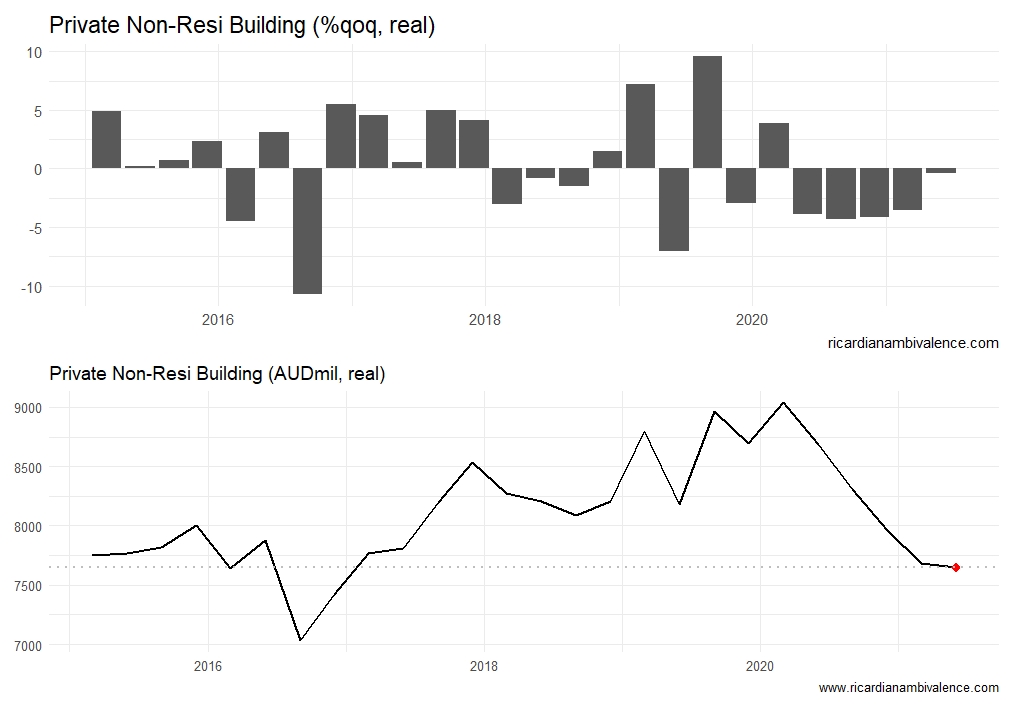

We will find out more about business investment from today’s capex report, however the indication from the Construction Work Done release is soft. The RBA forecast growth of 4.75%yoy for Private Business Investment. This equates to quarterly growth of 1.1%qoq.

The ongoing decline of Private non-Resi building makes growth of Private Business Investment seem like a stretch. Private non-Resi building continued its decline in the Q2 CWD release, shrinking by another 0.4%qoq. Other components of Capex might offset (and at times the Capex measure is notably different to the CWD measure) — but the prospect of private business making up for the weakness in Dwelling construction seems dim.

We’ll find out more over the next few days — but it looks like Q2 will be 25bps to 50bps softer than the baseline forecast. And of course, Q3 GDP will be around 200bps weaker (likely -3%qoq v. RBA -1%qoq). So the level of GDP is likely to be around 250bps lower than they forecast when they meet.

Unusually, the RBA will have Q2 GDP (released 1 September) when they meet on 7 September. This makes a policy response very likely.

What will they do?

Capacity in the bond market means that it’s hard to accelerate QE. Also, there’s little difference between promising to sustain QE at 4bn per week until at least February and pushing back the taper from 5bn per week to November.

The easier, and therefore most likely, decision would be to pre-commit and make November’s decision in September. Let’s say it’s a 50% chance. The probability of pushing back the taper (sustaining 5bn until the Nov review) is higher than the probability (30%) of no change at all (20%).

2 comments

Comments are closed.