The Q2 Capex report was stronger than expected (+4.4%qoq v. mkt +2.6%), however it doesn’t change the Q2 GDP story much: GDP is still tracking ~0.4%qoq (but due to the magic of rounding is now 40bps below the RBA’s August SOMP forecast).

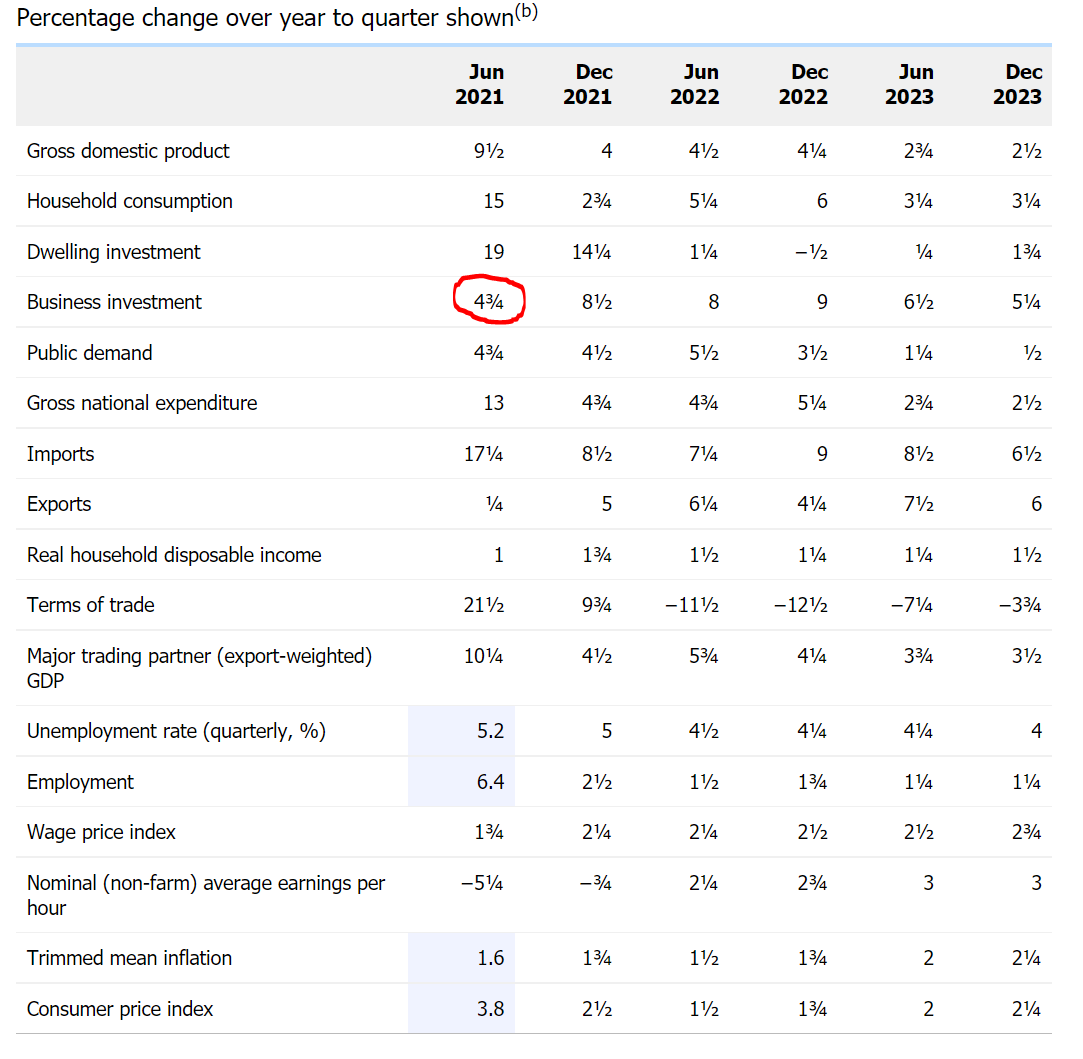

The main reason being that the Machinery and Equipment item from Capex (+4.3%qoq) is the only bit that directly impacts GDP. As it happens, the weakness in non-resi construction and engineering items (both from the Q2 Construction work done release), offset the strength in Machinery and Equipment. Adding it all up, the growth Business Investment for the year to Q2’21 looks to be running a touch below 4%yoy (v. RBA 4.75%yoy, see table at the bottom).

Combined with the weakness in Q2 Dwelling Investment, this puts my tracking of the RBA’s Q2 GDP forecast a touch below 0.4%qoq (9.1%yoy) … or ~40bps below their August SOMP forecast of 9.5%yoy.

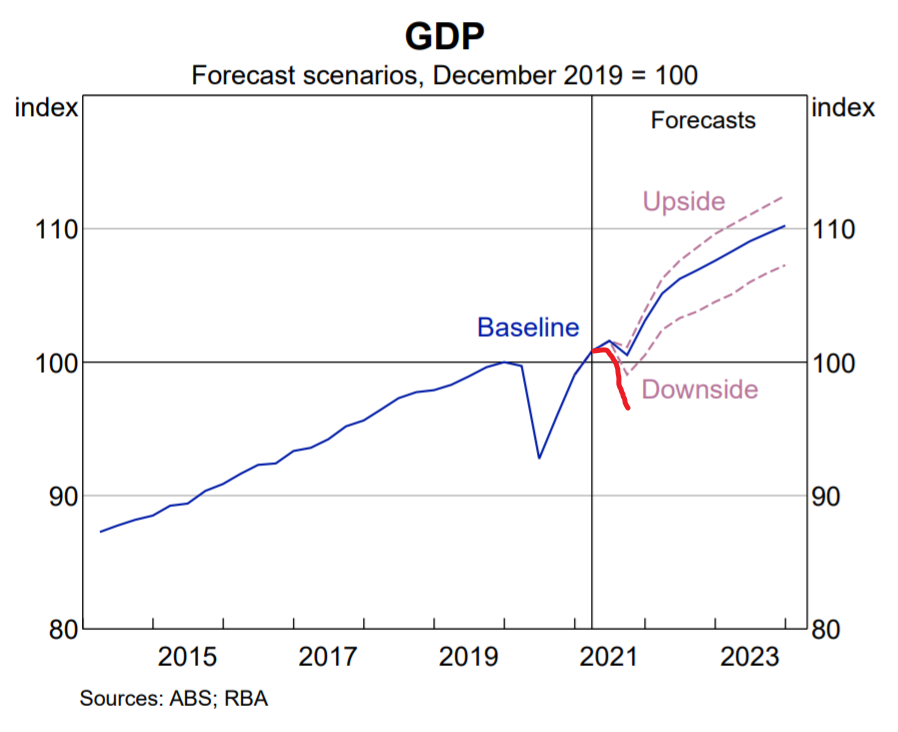

It’s not a bad number … it’s just not as good as the RBA expected. Their tracking estimate of Q2 private domestic demand would have declined by ~50bps to ~0.9%qoq. A decent number under most circumstances; but worse than expected (in their August SOMP). Throw in the Delta/lockdown-induced miss on Q3, and the level of GDP in Q3’21 will be about 250bps below the August SOMP’s baseline forecast.

The most likely Monetary Policy response is a promise to sustain QE at 4bn per week until at least February (50%); but dumping the taper (holding at 5bn/wk until at least Nov, 30%) seems more likely than no response at all (taper to 4bn per week and leave the November decision open, 20%).

There are downside risks to the Q2’21 GDP number. There was a large inventory build in Q1’21 and there’s some prospect of that being more fully unwound in Q2. Combined with a 50bps drag from Net Exports, it’s easy to imagine a negative outcome for Q2. It might cause a bit of recession hysteria, but that’d be noise (less inventories are almost always weak only in a headline sense). An inventories based miss is to be ignored.

Of course, the non-retail consumption item is both huge and a mystery. Weakness here would demand more attention from policy makers as it would disrupt their prior assessment that households were on a high confidence / high spending path pre-Delta.

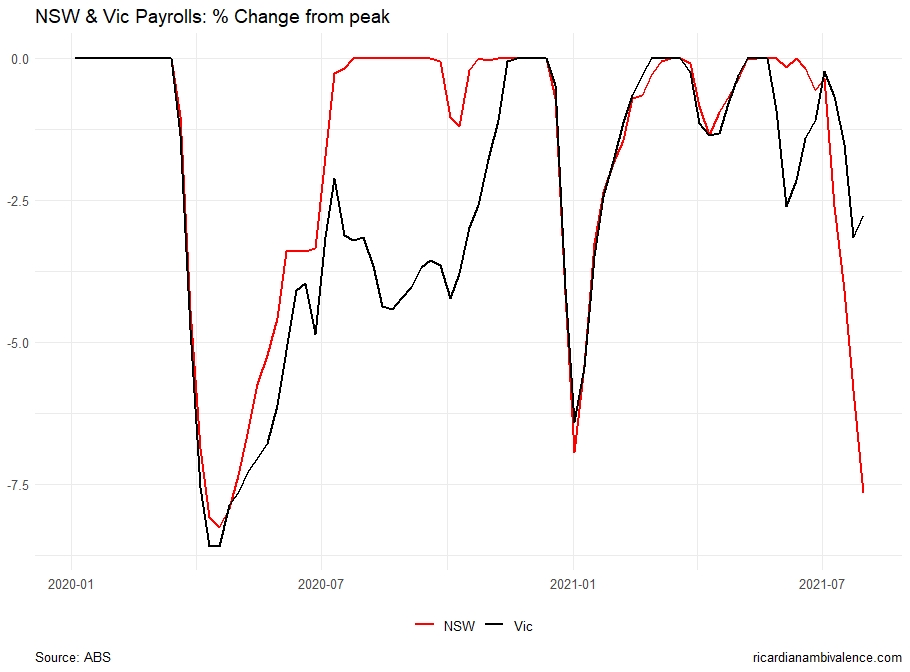

Policy-makers no doubt raised a few eye-brows at yesterday’s weekly payrolls report. Notwithstanding that the end point tends to be revised up (though a change in method this release should reduce this), weekly payrolls data suggests that job losses in NSW from the Delta lockdowns have been of the order of magnitude that we saw in the initial COVID lockdown — and much worse than the second Victorian lockdown (which seems to be the template many people are using).

Given the lags between policy asking and the impact on the real economy, the RBA’s focus is on the bounce. So the big question is how we recover from this dip.

A key difference this time is that the support programs are less wasteful generous. Of course, one person’s waste is another person’s cash, so less waste probably means a more mild recovery once the restrictions are eased. And an endemic-COVID recovery is likely to be more modest than the post-COVID bounce in H2’20.