A lot of talk surrounding the high Q2 inflation print has been about the extent to which it was the result of a number of once off factors, and as such can be ‘looked through’.

Apart from the fact that the RBA has told us the measure of inflation they prefer (the 2q average of the trimmed mean, which is 3.7%y/y AR), and that the best thing a Central Bank can do to stabilise inflation expectations (and hence inflation) is to pick some metric and stick to it, I think it’s worth looking at global inflation to see if the Australian inflation pulse is markedly different from what we’d expect, given peer inflation.

By no means is this a new idea: RBA Board member and ANU academic Warwick McKibbin has spoken about this a number of times, and the ECB has published research on the subject, which concludes that about 60% of the inflation impulse is global.

As you’d expect, given that the core measures the RBA prefers are also high, the pace of headline inflation looks about right, given peer inflation. That is, the trimmed mean and the weighted median are probably accurate. This shouldn’t come as a surprise, given the amount of work that’s been done on the question.

The above chart shows that the standardised rate of Australian inflation is just about where you would expect given peer inflation (note, I removed the GST changes in 2000).

The nations I have used are somewhat disparate, however they are the ones for which the RBA publishes inflation rates – and I figure that the RBA picked them for some reason.

To make the various national inflation data more comparable, I subtracted the mean and divided by the standard deviation for each national series — thereby allowing for different inflation targets and inflation volatility among the members (the USA, Japan, EU, UK, South Korea, Taiwan, Hong Kong, NZ, and Singapore).

I also split the groups between our Developed Market peers (the USA, Japan, EU and UK), and our Asian peers (South Korea, Taiwan, Hong Kong, NZ, and Singapore).

Apart from the fact that the acceleration and level of Australian inflation looks pretty right given the acceleration and level of inflation in our peers, I note that this was also the case in 2007/8. So, in this important way, the present acceleration in inflation is just like 2007/8.

I find this worrying, as the 2007/8 inflation surge was both unusually coordinated, and unusualy sharp. If it happens again, and there’s no GFC to help central banks out, policy is going to get diabolical (just think how difficult it would have been to get inflation back to 2% if there were no GFC).

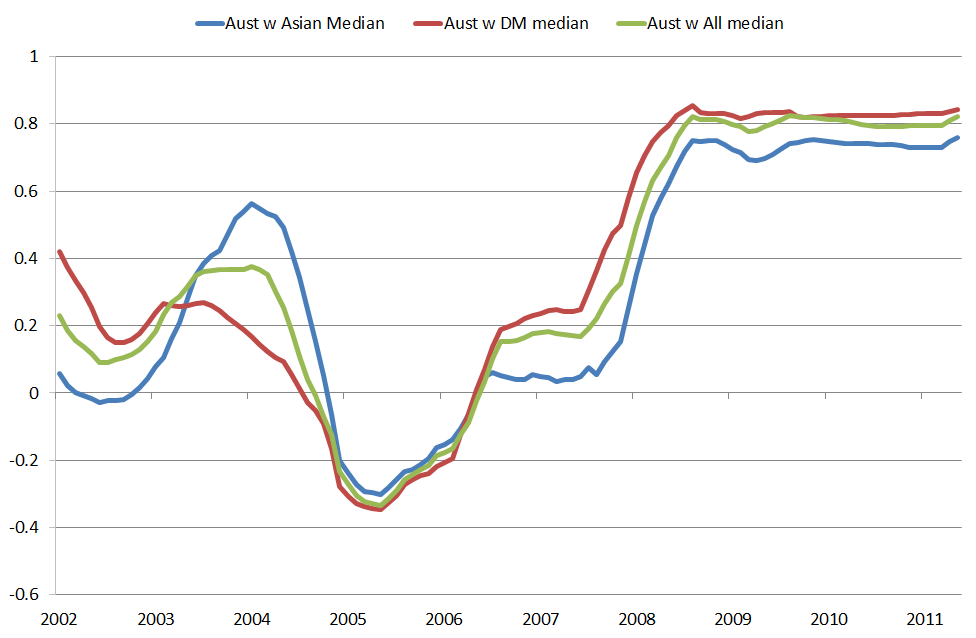

Finally, I think it is interesting to note that the cross market correlation of inflation has increased over the past ten years. The above chart shows the rolling 5yr correlation between Australian inflation, and the three global inflation measures I showed above (the DM median, Asian median, and All markets median).

What’s this all about? I suspect that global output gaps are now playing a much larger part in the initial inflation impulse.

For the (broken) North Atlantic nations, they can probably afford to ignore this inflation surge, as the real wage loss to workers is a larger concern. Their slack labour markets mean there is low risk of second round inflation.

In Australia, we don’t have that luxury (note, it’s the luxury of starting in a lousy position). We have a tight labour market and wage growth that is already at the limit of what is consistent with the RBA’s 2% to 3% inflation target, given weak productivity growth.

Thus, the RBA probably cannot afford to tough it out. What if they are right about the mining boom? Then they’ll be starting with inflation at 2.75%y/y and trying to keep it at that level through a huge growth surge.

That’s both a herculean task, and bad place to start!

Given the above, I suspect that the recent surge in Australian inflation is probably not about floods, or cyclones (or a stupid banana quarantine laws). Australia’s inflation outcomes are about what you’d expect given peer inflation outcomes.

Fast growth in Asia appears to be a part of the explanation for the global inflation surge. Asia is exporting inflation as their fast growing economies press against global capacity constraints. Another way of saying this is that Asia is transferring real resources away from us, by bidding up their price – and that we take a real pay cut as a result.

On net, Australia is a beneficiary of this surge – via the terms of trade – so the correct policy response is relatively clear — to tighten monetary policy.

Unfortunately, that hurts those who are not direct beneficiaries, but then, that is all part of the adjustment process… and in the long run it’s better than accommodating inflation, and having to wrestle it back later by inducing recession.

{kind=link}

{kind=link}

brilliant mate

it’s oil

Come on mate, it is more than that. And in any case, if it were oil, do you really think accommodation, as we tried in the 1970s is the welfare maximizing policy?

overlap your (very nice, i agree!) global inflation graph with oil prices and you’ll see a spike in 2008 , then drop in 2009 and a new spike in 2011. it’s very clear. i do not understand why you want to ignore the fact that last quarter inflation without food and fuel was only 0.5% and slowing down. They had higher non-volatile ‘core’ inflation in the USA last quarter with 9% plus unemployment! reality is that oil and all commodities were up last quarter, worldwide, combine that with the local natural disasters and you get ladt quarter numbers. hiking without knowing Q2 gdp numbers seems adventurous to me. we shall see what they decide!

I dislike exclusion measures, because they have been shown to be inferior to trims.

Additionally, I think the theory behind the use of exclusion measures is broken. Few still think that real price of commodities (food and fuel) will trend lower forever, and that price rises therefore reflect temporary supply shocks.

These prices move with demand, reset daily, and are very sensitive – so there is, in addition to lots of noise, also lots of leading signal in there too. This was proven (yet again) by the Asian experience of the last few years – the inflation problem showed up first in fast moving prices, and then lat in slower moving prices.

Finally, i find it annoying that folks are moving the goal posts and being quite ad hoc. Shall we subtract the increase in fruit increase and leave in the drop in vege prices?

Do you think the RBA will revise down their CPI projections following this number? I doubt it.

The best thing a central bank can do is to pick some measure and stick to it. That much is clear.

Sent from my iPad

The best thing a central bank can do is to use all the data that is available.

You said it as an aside.

There is no global inflation surge.

Inflation rose on one of factors in both the USA and UK and is falling now as one might expect given their output gaps.(Woken up on this yet Chris?)

Similarly inflation is not a problem in Europe or Japan.

It is a problem here and in many Developing nations because the output gaps are small or non-existent.

So inflation is certainly not a global problem at all. It is almost a ‘Developing’ problem.

Miraculous coincidence that correlation…

Sent from my iPad

now if Chris had read this piece he wouldn’t have egg all over his face.