Stats NZ today heavily revised NZ GDP. The revisions suggest that the recession was smaller than expected, but that the recovery has recently been weaker than thought.

Most of the slump is in the last six quarters. The revised production side data show ~1.5% GDP growth over the past six quarters, down from ~2% in the prior data. The revised expenditure side data show growth of only ~0.2% over the last six quarters, down from ~2% in the prior data.

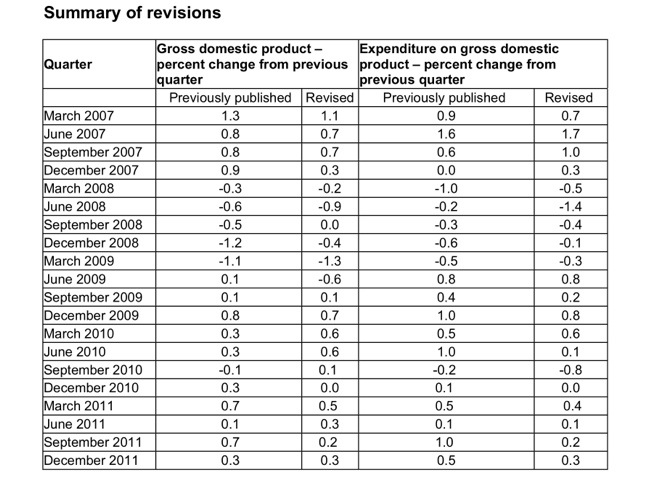

On the production side, Q4’11 was unrevised at 0.3%qq (RBNZ Q1 MPS est 0.6%qq); Q3’11 was revised down to 0.2%qq (prior est 0.7%qq, RBNZ Q1 MPS 0.8%qq); Q2’11 was revised up 20bps to 0.3%qq (RBNZ and prior 0.1%qq); Q1’11 was revised down 20bps to 0.5%qq (RBNZ and prior 0.7%qq).

Through the year growth is now estimated to have been 1.1%yoy, down from the prior estimate of 1.4%yoy and 80bps below the RBNZ’s Q1 MPS forecast of 2.2%.

On this basis, it seems likely that the NZ output gap has been widening for at least 6 quarters, despite the 2.5% OCR.

The case for easier monetary policy is fairly straightforward. Low inflation, sub-trend GDP, no decline in the unemployment rate since the crisis ended.

I expect a 25bps cut at the RBNZ’s 14 June meeting, and another at their 26 July meeting – taking their offocial cash rate down to 2%