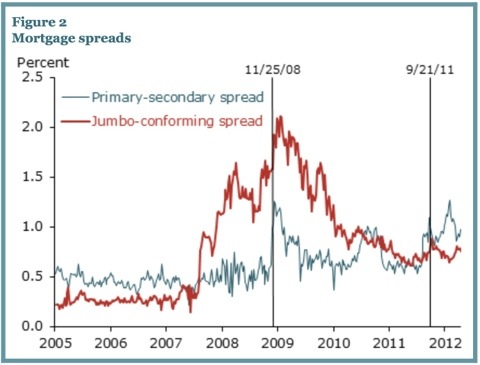

The financial crisis – and subsequent regulation – has increased the cost of financial intermediation. This FRBSF Fed letter covers the widening of retail mortgage spreads, relative to MBS, noting that:

Unconventional monetary policy actions can only be successful in stimulating the economy if they lower the interest rates that matter most for businesses and households, that is, the private borrowing rates that determine the cost of funds for the private sector

It sounds to me like the SF Fed is making an argument for QE3 focused on MBS buying.

It would run something like the argument for a 50bps cut at the May’12 RBA meeting – due to a widening of the spread between our policy rate and the rates that matter, we are not as easy as is appropriate.

My sense is that this dynamic has further to play out – in all markets.