The sell-side /blogger reaction to Fed Dudley’s recent speech suggested that the Fed had made an unexpectedly hawkish move.

Tim Duy, for example, concluded from it that:

the baseline scenario should be that QE3 is not on the table

This was a surprise to me, as the data since the April Fed meeting has been a bit softer, and Bernanke had explicitly gone out of his way to say that QE remained on the table at the April presser.

So we have been very accommodative, and we remain prepared to do more as needed to make sure that this recovery continues and that inflation stays close to target … So those tools remain very much on the table, and we will not hesitate to use them should the economy require additional support

The street appears to have over-interpreted the following sentence in Dudley’s speech:

As long as the U.S. economy continues to grow sufficiently fast to cut into the nation’s unused economic resources at a meaningful pace, I think the benefits from further action are unlikely to exceed the costs.

But read in context, it is not hawkish. Dudley sees an immediate case for more action, based on the unsatisfactory outlook, but is worried about the possible costs of further easing.

Given our forecast of stable prices and a still slow path back to full employment, there is an argument for easing further. But, unfortunately, our tools have costs associated with them as well as benefits. Thus, we must weigh these costs against the benefits of further action.

As long as the U.S. economy continues to grow sufficiently fast to cut into the nation’s unused economic resources at a meaningful pace, I think the benefits from further action are unlikely to exceed the costs. But if the economy were to slow so that we were no longer making material progress toward full employment, the downside risks to growth were to increase sharply, or if deflation risks were to climb materially, then the benefits of further accommodation would increase in my estimation and this could tilt the balance toward additional easing.

The US data has been soft of late, and global conditions have been weakening, so the events are doubtless moving Dudley toward a vote for further policy easing.

Amidst all this QE3 hunting, folks missed a very interesting talk about the montary transmission mechanism and the fed’s risk management approach to policy.

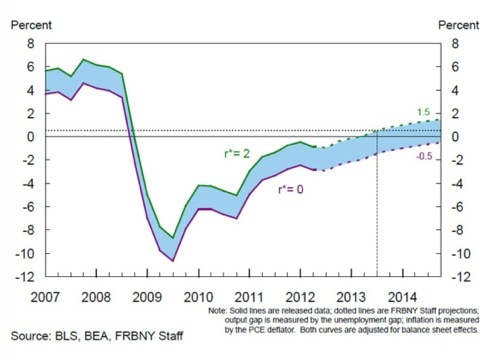

The most interesting part was Dudley’s judgement that the neutral real rate for the US economy had fallen – he cites work by SF Fed Williams and FRB Laubach that suggests it may be 0.3%.

This is around 170bps lower than ‘standard’ Taylor type rules suggest. Making such an adjustment means a Taylor 1999 rule suggests a first hike in 2015 – see the below chart.

My best guess is that there will be more balance sheet expansion this year, and that the first hike will be 2015 or later. The literature on the ZLB is clear that you should wait to lift rates until deflation risk has completely faded, so the Fed is going to be at the very least extremely slow to hike.

A rule of thumb that captures this is: if the optimal rate is below 1% go to zero (which in the Fed’s present case is 0-25bps). Looking at Dudley’s adjusted Taylor-99 chart, the trajectory suggests the optimal rate will not be greater than 1% until mid 2016.

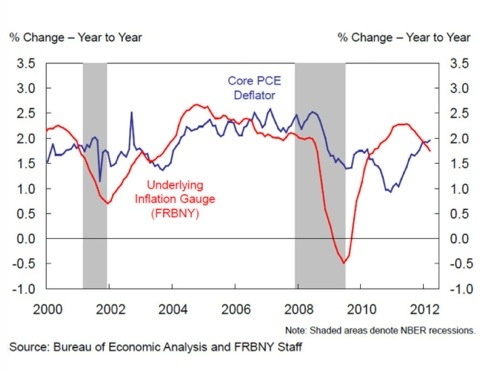

Inflation pressures are easing, and seem likely to decline further. Headline pressures are easing as commodity prices decline, and sub-trend global growth and a decent supply response seem likely to keep it this way. High unemployment and low headline pressures are likely to keep core measures tame.

The FRBNY has made the same judgement — their underlying inflation gauge is falling fast.

If I am right about the inflation outlook, we seem likely to see further balance sheet action from the Fed before the end of this year.

yep I think you are right.

with fiscal policy being either neutral or restrictive there is nothing other than another QE to do to help the economy.