The resilience of the AUD has come as a surprise to many in the market, particularly as the foreign exchange value of the AUD has remained elevated despite the decline in interest rates (both in absolute and relative terms) and the decline in the terms of trade (mostly due to declining Australian export prices).

I have nit-picked before, noting that neither ‘broken relationship’ is sufficient to demonstrate that the AUD is overvalued, but today i want to give an alternate view.

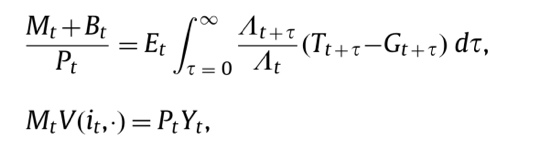

The view is set out by John Cochrane, in his 2011 paper Understanding policy in the great recession: Some unpleasant fiscal arithmetic. The paper is in the spirit of Sargent and Wallace (1981), and is based around the following two equations:

The top equation does most of the heavy lifting – it states that the real value of consolidated government liabilities (Money and Bonds) is equal to the net present value of future government surpluses.

Once you start thinking of both Money and Bonds as liabilities of the Australian Government, it clears things up. In particular, it makes clear that if the credit quality of Australia improves, both the foreign exchange value of the AUD and the price of her bonds might increase.

If we allow capital lambda to include a risk premium, and have global capital markets, then we have what we need to explain the recent data – a decrease in the relative riskiness of the Australian Sovereign has increased the relative valuation of her liabilities.

When this occurs, we should expect that both M and B will increase in value – and that is what we have observed.

While i am being a bit of a fan, you should check out his excellent blog. If you do not have time for another blog, at least read his wonderful Krugman critique from 2009.

Japanese bond prices and the Yen have also risen over the last 2 and 3 years. Can you also say about Japan that its relative sovereign riskiness has decreased over that time? And Japan is one of the few countries where bond prices and the currency typically move in the same direction concurrently – it’s a ‘risk-off’ country. In most ‘risk-on’ countries like Australia, bond prices and the currency typically move in opposite directions in the short term (eg the last couple of weeks).

Isn’t the recent strength of the AUD really due to the market pricing in greater chance of monetary easing in the US and Europe and less chance here? After all, the AUD has strengthened more against the USD and EUR than against the JPY.

Well, the nominal value of the JPY had to rise as they have had lower inflation.

But thinking in real terms — yes, i would say that the relative riskiness of JGBs and JPY denominated investments has declined since 2008.

Wouldn’t you?

Well, both the US and Japanese budget balances have deteriorated by about the same amount since 2008. But since 2010, the Japanese budget has improved by somewhat less than the US budget.

My impression is that everyone has been catching down to the Japanese, but i am not an expert on Japanese fiscal policy.

I am surprised you think Cochrane’s critique of Krugman has legs.

He got slam dunked by quite a few over some of the comments.

He used to be okay but since the GFC he has simply put out Republican propaganda and not very good propaganda at that.

It has even spread to Alan Meltzer now.

Post the links to the critique please.

whoops,

Japan originally got into their present state because of preamture austerity as both Posen and Koo have shown.

I did do a spell check but what happened?

not sure mate. i edited them to remove the typos.

– start of rant –

High AUD benefiting consumers???? Look, a lot of businesses are still to pass on the benefits. Examples?

Adobe software products (DOWNLOADS ONLY) are all 50% more expensive in Australia. Why???

http://desktopmag.com.au/news/adobes-cs6-pricing-explanation/

or

VMware workstation DOWNLOAD – in the US?: US$ 199 – In Australia ? AUD 291.50

Why? Because they can, Certainly these products are not made or supported in Australia.

– end of rant! –

good points. but what does that tell you? That we need tighter monetary policy to squeeze the inflation out? or easier money to accommodate the higher prices? Clearly, these vendors are pricing to market, but what to do about it, and what it means, is not so simple… at least in general, a higher AUD means lower import prices, and that benefits households and importers.

Well, a higher AUD means lower import prices… partly.

If there is competition here in Australia for a product or service OK. But otherwise a high AUD just goes into profits of the company exporting into Australia… because they can. Also a lot of importers are importing cheaper, yes, but not necessarily passing the difference to households. So the benefits of a higher AUD for the whole of Australia must be carefully balanced vs the disadvantages of a high currency.

Since everybody LOVES the AUD, we could just print lots of it and start buying all sort of foreign assets, that are so cheap right now.

These are all transfers, right? It annoys me that folks talk about it like it is a free lunch. If the CB sells the AUD to buy foreign assets, we all pay for it with lower real spending power due to the lower AUD. It might be appropriate – and net stimulatory – to do so, but just like lower rates hurt savers, selling the AUD to lower it costs those of us who are net importers.

You are right, but a high AUD is not a free lunch either, no worry about that. When you tell Europeans that a cappuccino in Australia is now almost 4 euro they fall off the chair! :)

My australian mates who live in London complain about the cost of living when they come home – and they are fairly well off. I have to say, Zurich kills me and i live here!

Nice Article! I am wondering how the big Fx investors determine value of a currency before placing trades. I hear terms like overnight swaps, COT etc., what is the real valuation process for fx…Any ideas, Any books or disciple that can be learned?

for Australia, the big FX investors seem to be the large bond funds — mostly sovereign wealth funds / central banks. Obviously, there are a variety of valuation techniques, however i think that these medium term budget constraint approaches have more traction with the somewhat more academic approach of these investors. Another approach is to match FX holdings to import shares — a similar approach matches FX to import costs, so for example a commodity importer might purchase Australian Dollars, as they figure that their AUD portfolio will be correlated (somewhat) to their commodity import bill.