RBA Gov Stevens today gave a speech entitled The Lucky Country in which he laid out the RBA’s view of three bearish shibboleths.

In the speech, Gov Stevens first showed that on any number of metrics we have done well over the past few years. I have cut and paste the real GDP per capita chart, above (note the disaster in NZ – for shame Gov Bollard).

Next, he argued that while some of our good fortune is due to luck, we have also managed our fortune well. The decision to float the AUD (and to let it float), the regulation and supervision of Australian banks, and the bipartisan support for an independent central bank (which allowed aggressive rate cuts despite a weakening currency) and prudent fiscal settings were all given as

examples of how we have made the most of our luck.

I think that – for the most part – Stevens is right about this. We managed well from the 1980s to the end of the Howard era. Prosperity means that we have not had to see the price of the re-regulation of the labour market, but i think it will prove to have been a mis-step.

Onto the shibboleths: Stevens dealt with the risks from Europe; the risks from a China slowdown; the risks from Aussie house prices; and the risks from the structure of Aussie bank wholesale funding.

On Europe, the risks are undeniable. Gov Stevens seems much more focused on European risks than Q2 CPI. If the RBA is to validate current market pricing, this that would be the cause. He pointed to the financial channel (risk that financial markets freeze) as the transmission mechanism. It is worth noting here that Aussie banks are well funded – this is nothing like 2008.

Interestingly, he said that if the EUR were to break up, the capital flight to Australia might just soften this funding squeeze. I doubt it – i think it would be a proper crisis – but it would not be the first time i have been wrong.

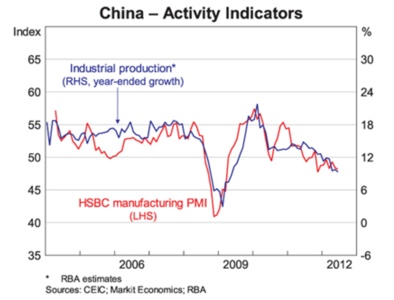

His assessment of China was that the so called slow down is 10% IP growth or about 7% GDP growth. This is the result of deliberate policy, and is something to be welcomed, as it makes their long run growth more sustainable. Moreover, the Chinese have recently taken timely and appropriate steps to ease policy, so this ought to be it.

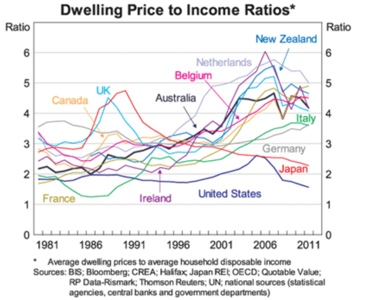

On house prices, he noted that the increase was global, and that we should look to global explanations – implying that the increased availability of credit may have been the cause. I think that there is good reason to doubt that the old price to income ratios were an equilibrium – though i also think that there is reason to think we have overshot.

What made me less concerned about the need for further ‘working out’ of high house prices is that house purchases have now become very affordable. Repayments as a share of income on an 80% LVR loan are ~3ppts below their decade average – thanks to higher incomes and modestly lower mortgage rates.

This development is a reason to think that the recent increase in house prices is a stabilization (see here for more).

I suspect that rising house prices raise the hurdle for further rate cuts.

Following the speech, in the Q+A, Stevens said that they had expected the unemployment rate to be higher by now, that he thought CPI would be around 2%, and that he thought that domestic monetary policy settings were ‘about right’.

Given this summary, i doubt that the RBA would cut rates even with Q2 core CPI at 0.4%qoq. The next cut will come when there is a clear indication that demand is weaker than they expect – and if Europe doesn’t implode, it is going to take time for that evidence to accumulate.

The bottom line – it is not really about Q2 CPI…

Unfortunately, I think you are right, Ricardo. The RBA is too busy fighting last decade’s battles and hasn’t realised we are living in deflationary times. Rates have only just moved below neutral after 18 months of excessive tightness. House prices have just started to stabilise and even Chris Joye concedes that an incipient recovery earlier this year was killed off by a mere 15 bp out-of-cycle increase by ANZ. I don’t think the Australian recession risk is significant at the moment, but the RBA is playing with fire. With most of the developed world in recession, they would be well-advised to take out some more insurance at extremely low cost. Far better to enter a US recession with 5-6% nominal GDP growth than 3-4%.