At first blush, the August RBA meeting seems a little boring – however i think that it is a mistake to see it that way. For, while the OIS have only 2.5bps (a 10% chance of a 25bps cut) priced in for August, there is much that may be learned about the near term outlook from tomorrow’s statement.

I am particularly looking for hints about the RBA’s new forecasts. For example, there is strong evidence that the economy was stronger than they judged it to be in H1’12 — and i would like to know how that feeds through into their inflation forecast.

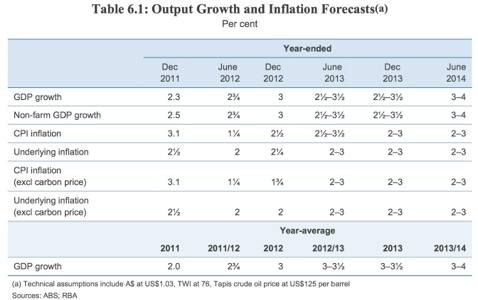

The RBA’s Q2 SOMP forecasts, below, show growth battling back to an above trend pace in H1 2014, but new information suggests that the economy was above trend in the year to H1’12. It is plausible that the upgrade to H1’12 will be a full 75bps (to 3.5%yoy) and the better start to the year ought to see H2 brought up to at least 3.25%yoy. I estimate that trend growth is between 3%yoy and 3.5%yoy, so these numbers are around potential.

There is a lot of skepticism about the true strength of growth out there – both among bank economists and the man on the street – so how the RBA treats this growth surprise is key. They might assume that the data is bad, or that the momentum will not be sustained, and therefore leave their growth and inflation forecasts unchanged – but i think that is unlikely.

More likely, they will bump up the H1’12 estimate to 3.5%, and assume that some of it is the catch up growth that they were expecting later (and therefore assume that momentum fades a little).

Even doing this, it is very likely that the inflation forecast will rise a little.

Prior stronger growth means that their estimate of the output gap will be a little smaller – Gov Stevens already told us this, in a fashion, when he said that they were expecting the unemployment rate to be higher by now.

So with better initial growth momentum, and a smaller output gap, we are likely to see a modest upgrade to the RBA’s inflation track. They would signal this by changing their inflation forecast bands back to point estimates, and moving the mid-point above 2.5% (they would most likely do this at the right tail).

Does this mean the next move is up? No. It just means that the hurdle for cuts has got higher, due to the fact that the RBA has taken on a more neutral bias.

Job ads still look weak, so i would expect the unemployment rate to keep trending up into year’s end – particularly as that is when the recent fiscal sweetener will fade, and the real work of the chunky fiscal contraction will begin.

I am unsure if we will see evidence of that this year – but my current guess is that we will, and that the RBA will be back in November, cutting their policy rate and re-downgrading their outlook. My current estimate is -50bps in Q4, and a further -50bps in H1’13, for a cash rate of 2.5%

The risks i see to this are balanced – Europe could blow up and bring the cuts forward, or it might take longer for the unemployment rate to break the range we have been in for the last few years (due to the fiscal sweetener taking longer to wear off).

Great post. BTW, any thoughts on McKibbin’s suggestion to sell dollars one month after saying rates should go up? Is he becoming the Australian Allan Meltzer?

Relevance starved? Seems unlikely to me.