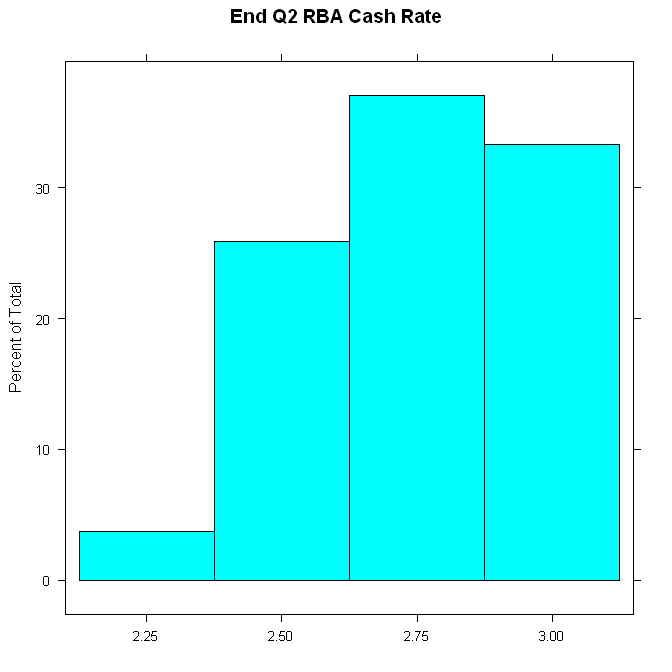

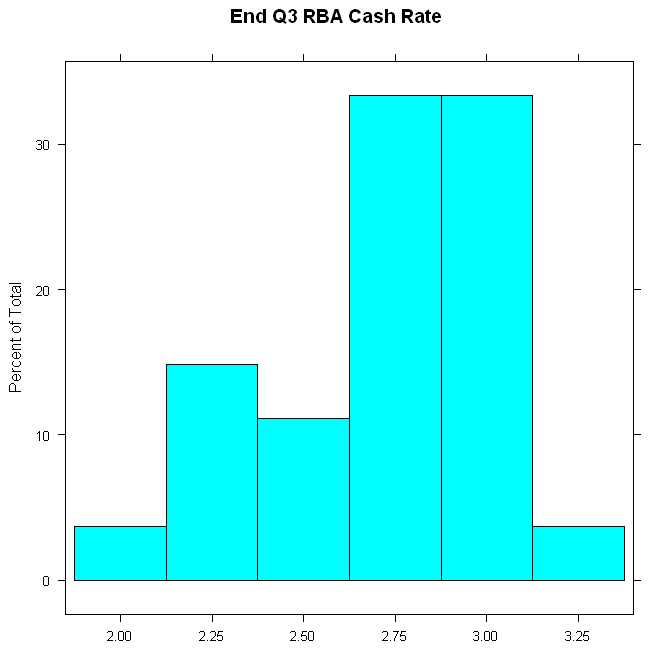

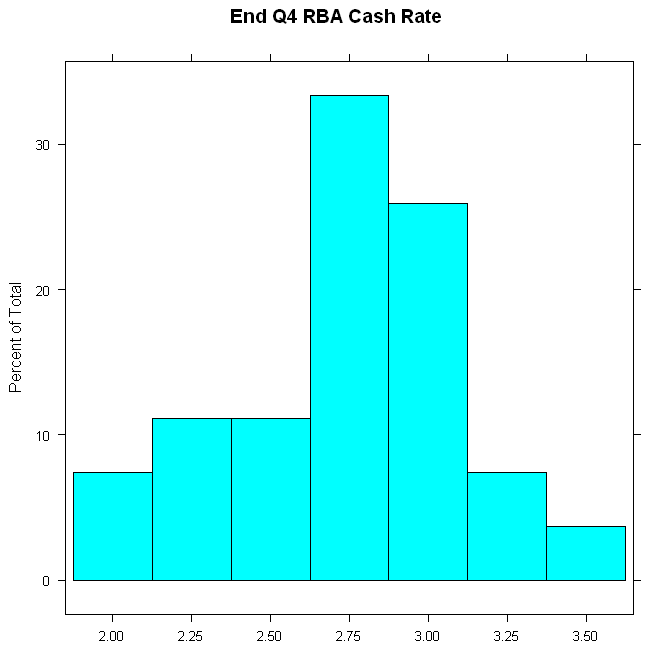

There’s currently a wide variety of RBA views in the Bloomberg survey — the widest i’ve seen in some time. The spread for the year end forecast is ~150bps (minimum at 2% and maximum is 3.5%).

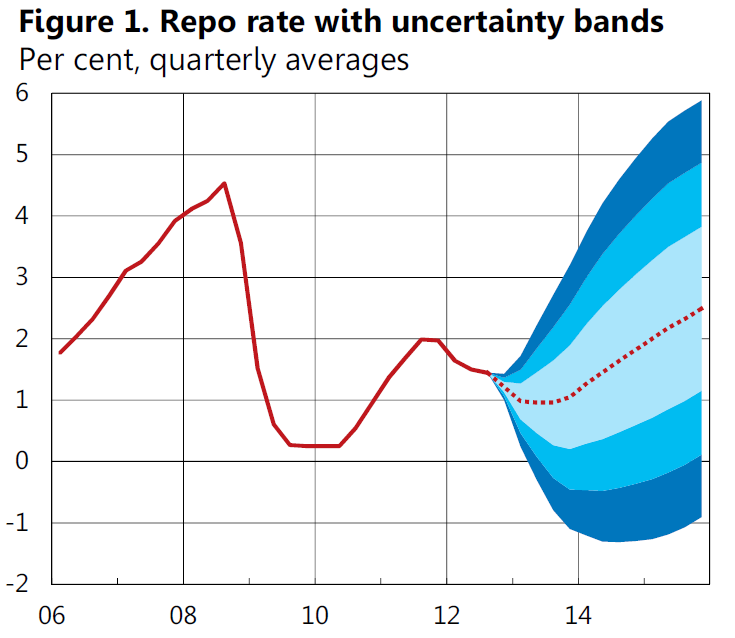

This may seem like a large spread, but real 90% confidence intervals are ~400bps for 1yr ahead cash rate calls … the Riksbank is as good as anyone at this stuff (i would wager that their forecasting attempts are a little more serious than your average bank economist’s), and that’s what they get.

There just isn’t really much difference between a 2.5% call and 3.0% call for 1yr ahead.

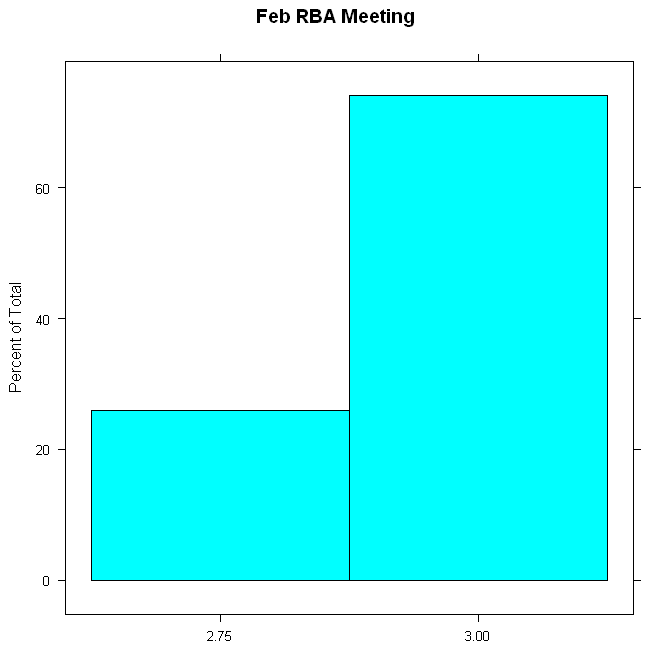

I thought they would not cut in Feb, but then we saw the unemployment situation clearly worsening, CPI still benign and govt still on “austerity” mode. I now think they will cut in Feb since there was no Jan cut. Then a pause next month. Housing is still not responding to cuts, the only positive data since last meeting is the global mood and iron ore, but it’s not enough IMO. Dollar still a drag.

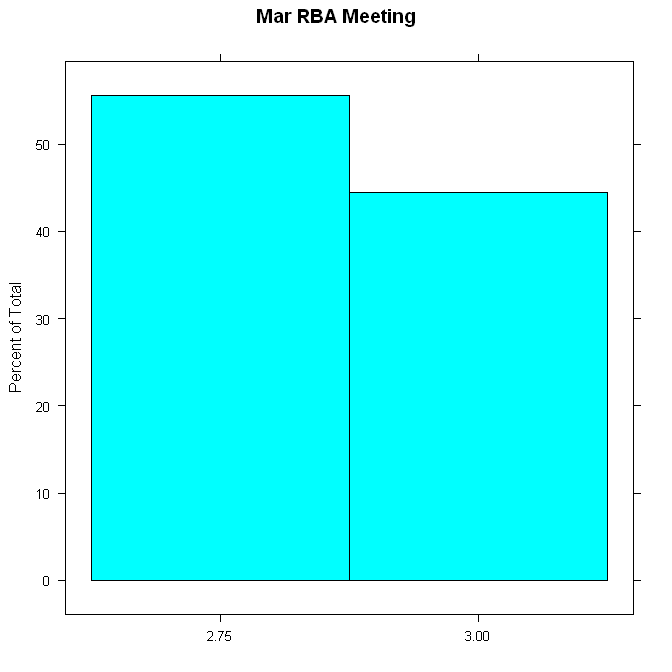

… and banks will pass cut in full this time, so not cut in Mar after Feb cut.

The TWI is actually up substantially — thanks to the big move in AUDJPY it’s near the top of the range over the last few years.