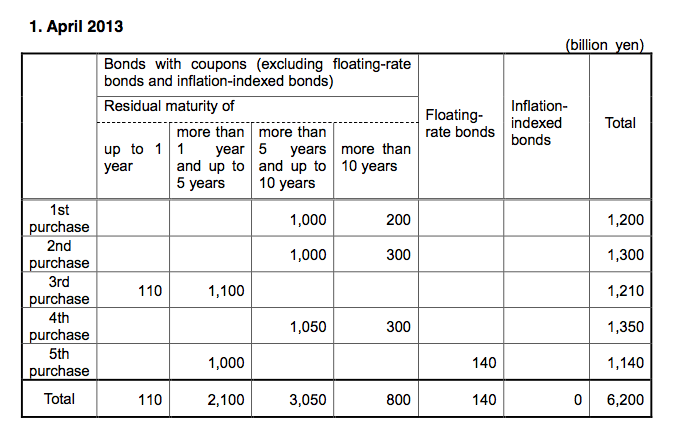

The Japanese Business paper Nikkei reports that the Bank of Japan will kick off their easing campaign with Y1.2tn of JGB purchases this week. The indication is that their purchase programme will be a reverse tender process — just like the one the Fed has used.

The memo posted following the 5 April decision, contains a schedule that shows the tenor buckets they plan to buy at each OMO — but not the exact days. Expect prices to squeeze up into the buybacks, on the days that one has been announced (most likely ~10am Tokyo time).

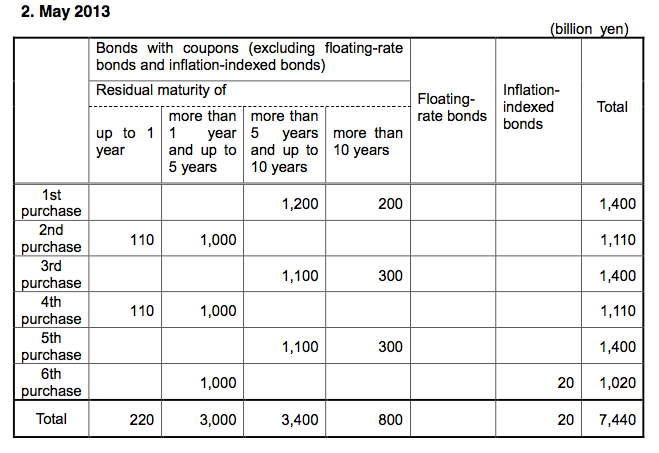

In April, the BoJ plan on buying ~Y6.2tn of JGBs in five OMO. The above schedule shows that it will be mostly in the 5yr to 10yr sector. In subsequent months, there will be six OMOs, and purchases will be ~Y7.5tn (the May schedule, below, shows ~Y7.4tn per month, with the majority in the > 5yr bucket).

There’s already some odd stuff floating about wringing hands about what it might mean if the BoJ is unable to buy Y1.2tn of JGBs.

In my view, this point of view misses the point entirely. It doesn’t matter.

Japanese Banks already hold Y47tn in BoJ current accounts — so there is no sense in which they are reserve constrained in their lending. Thus, the quantity of base money the BoJ supplies is unimportant.

What is important is the market’s assessment of how committed the BoJ is to their policy framework. If the market REALLY believes the BoJ, and does not bid Y1.2tn of JGBs into the reverse auction (so that the BoJ is unable to buy Y1.2tn of bonds at any price) does it matter?

No, because if they happens, the BoJ will have hit all bids, and their known excess demand for JGBs will cause the market yield on JGBs to decline even further — a victory for the BoJ!

For while the quantity of base money is now the BoJ’s target, it meaningless in terms of the operational macro-economic efficacy of this policy. Banks simply are not reserve constrained in their lending – so the quantity of base money has no operational impact on their lending activity.

The import of the base money growth target is that it commits the BoJ to a policy over time (in this case a purchase plan) — this gives their policy rule credibility.

The greater the policy rule’s credibility the weaker the JPY and the lower JGB yields — which will boost expected returns from investing in Japanese firms (and lowers returns from investing in risk free assets). This should boost the Japanese economy via both consumption and investment channels.

Should JGB yields collapse on day 1 due to a ‘failed’ buyback it would signal that the policy has very large credibility.

Sure, that means the BoJ will have supplied less base money at the first auction, but that’s not important. If this auction fails, they can ‘catch up’ later.

So if we do see a failed buy-back the JPY should weaken and JGBs ought to bull-flatten, as it will show that the BoJ’s new policy already has strong credibility. The better the credibility, the lower yields ought to be, and better the policy will work.

This is going to be a failure if japanese y/y inflation, one year from today, is not above …. what … 1% ?

I insist there will be many countries that should be upset about this ongoing currency war! including Australia.

I think 0.5%yoy would be a good first year. These things work with a lag.

and second year at 2%? unlikely

yeah, i think moving it 0.5ppts a year would be a good result. i used to be very sceptical about policy all together — if nothing else, this is an interesting experiment!

Dumb question mate. What does it mean for banks not being reserve constrained in their lending. Heres what i think happens

– They can’t turn reserves into mortgages or commercial loans.

– They can only use it to settle interbank transactions.

– some banks may have lending opportunities other banks can’t. So reserves act as a means of settlement by which bank a for example pays bank b for their term debt in exchange for reserves (ps – this seems odd to me)

– the central bank determines the quantity of system reserves (almost entirely)

To what extent can reserves quantities constrain lending? Is it because their isn’t enough for bank a to lend to bank b, the latter of which would like to lend to firm x or household y?

Thanks for monetary economics 101.

It’s all about your last point — the CB picks the system reserve position.

in a ‘normal’ regime, the scarcity of reserves sets their price in the overnight market, and that’s how you get a positive overnight rate. If banks in aggregate wish to lend more, which will create more deposits, the system requires more reserves — in a ‘normal’ system, this bids up the price of reserves in the overnight market. In a QE system, reserves are no longer scarce, and banks (both individually and in aggregate) typically hold reserves that are well in excess of their requirements. To say that such banks / systems are not reserve constrained in the lending means that the CB would not have to add reserves to keep the price of overnight cash stable should the system create more credit (= deposits).

As you point out, there are still going to be banks with better opportunities to lend in any system — and to the extent that bank A has the potential to lend, but not the reserves to back the deposit creation, they obtain the reserves to do so from bank B via the interbank market. That may be hard from time to time, so there may be constraints even in a cashed up system, but for the most part the quantity of reserves is not a constraint on credit creation.

… perhaps this is a good subject for a post?

Indeed a good topic for a post. What of regimes without a reserve requirement (eg Australia?)

Do you move to a desired reserve setting?

Yeah, it is a bit passé these days in Aus but if you have deposits you do need some reserves. If the CB sees excess demand for reserves in OMOs or daylight operations, they may move their rate. You still need some reserves, and esp access to them to grow credit.

Ps that was a great explanation

I agree the central issue is the BoJ’s credibility rather than its short-term success in buying bonds at a particular auction; the question is whether their credibility will be affected by that short-term failure. It won’t so long as the BoJ can credibly say they will make up shortfalls in future. But let’s take it to the extreme and assume that no auction looks like achieving the required number of purchases. Then I would say the credibility of the policy would be affected.

I don’t think the short-term effect on yields tells you much about whether the policy is working. But I agree the effect on the Yen does.

I guess my point is that there is nothing that cannot be done, economically or financially, due to a present shortage of base money. If a buyback fails due to excess demand, and yields decline, that’s a good thing.

I agree with your first sentence – clearly it’s true, as the Australian RBA has a much smaller balance sheet than the BoJ, Fed, ECB or the BoE and we’re doing much better than all of them. Velocity is too low in those countries; that’s the problem, and the solution is to lift it back towards more normal levels.

I’m not sure about the second sentence, though, and I’m not sure it follows from the first. Lower yields could be consistent with a failed buyback fanning expectations of lower inflation/ more deflation due to a loss in central bank credibility for achieving its target.

i think it’s true that low yields may signal deflationary expectations, however my point is a narrow one — that is that there is nothing for the reserves to do. the buying operations are the thing, and they are the thing because the move important prices in the economy. If a buyback fails due to excess demand for JGBs (assuming it’s not due to a deflationary turn in expectations) then it’s a good thing.

my point is that it’s the asset prices and not base money they do the work — and that if we get less base money and more ‘helpful’ changes in asset prices, well that’s OK.

Part of the effort of re-inflating the Japanese economy?

http://www.adelaidenow.com.au/news/south-australia/holden-set-to-make-major-announcement-regarding-jobs-at-south-australian-and-victorian-plants/story-e6frea83-1226614971545

But who cares we have mining! :)

Holden chairman and managing director Mike Devereux says the carmaker was priced out of export markets by the high Australian dollar and it was “crucial to align production with local demand”.

**** priced out of export markets ****

and you still believe BoJ are fighting deflation here?

They could not care less about inflation, that is just an orthodox cover-up. Reality is that #1, #2 and #3 economies in the world can do whatever they like and all the rest must just accept. Until it will become no longer acceptable.

Cheaper cars for most of us. Australia has no business making cars. It is stupid for Australia to do so. We can buy them cheaper from elsewhere.

“Australia has no business making cars … ” and Japan / Germany / US do? Why? High-costs economy has definitely killed any chances we had to compete anyway.

“We can buy them cheaper from elsewhere.” That is very true. And not only cars. Software, education, tourism, we are just to expensive now for everything. The sooner the mining boom ends the better.

Cars are a scale game.

Germany has 5 large car companies and a population of 80 millions.

Disagree — they have a market that is 300m in europe, plus a global franchise that sells to 2bn. Anyhow, they make great cars — everyone wants one. Australian cars are not so well regarded. If we made great cars, they would not need protection and subsidies.

I am old enough to remember when they would advertise foreign cars for sale in Australia as ‘fully imported’ — meaning not local garbage. We had 70% tariffs on imported cars at that time.

The German car industry can only survive because they export most of their cars, as Germany is a relatively small country and have 5 major car companies. What I am saying is that the size of Australia per se would allow us to have at least one successful company. I do agree that car makers is Australia have not been competitive, but what I am saying is that the high dollar has now destroyed any hope that was left. And then I am wondering if it is a good choice to sacrifice all of these industries in the name of mining. Plus what happens if commodities prices come down and the dollar does not.

I am not very familiar with the history of car makers in Germany but I am quite sure they are where they are now thanks to a lot of govt help and subsidies.

The next one to go is Qantas in the next 5 years.

That’s true, almost all car companies receive protection and subsidies from governments in various jurisdictions. I have no interest in subsidising folks — let foreign taxpayers subsidise my car consumption!

Australian car companies are professional rent seekers and serial losers — their products are terrible.

Are you seriously suggesting that we in Australia would somehow be better off if the US, Japan and Europe each tightened monetary policy? We would have a lower dollar, but the world would go into recession. We gain, in net terms (as does any small open economy), when larger economies are growing, even if it means a higher local currency.

We would be better off with a 15% lower AUD regardless of monetary policy in other countries.

That’s almost certainly wrong. It is not going to be much help having the AUD 15% lower if demand substantially weaker in our export markets.

You might argue that monetary policy does not work — in which case it impacts neither the JPY nor activity — but then it follows that policy isn’t moving the AUD either.

We go back to what we’ve discussed before here. Currency pegging or similar policies. They can devalue their currencies, follow whatever monetary policy they think is good for them. But we do not necessarily need to accept a “free market” currency value. How is Switzerland doing?

Anyway, my initial thoughts were more towards southern Europe, not Australia right now. They need a much lower EURO much more than Japan or the US, but they are not achieving that partly because of Germany.

Don’t think only about exports towards them. Think about competition from them (cheaper imports into Australia or competition for existing demand, e.g. airlines, car companies etc) and investment in Australia by multinational companies (where will we open the next high-tech center in Asia?). The currency impact for a small economy like Australia is huge.