The BoJ has obtained a larger than usual move in the JPY in response to last week’s new easing policy (see my summary for details). Sceptics, however, might argue that this is nothing new — the BoJ has been doing QE on and off for a decade.

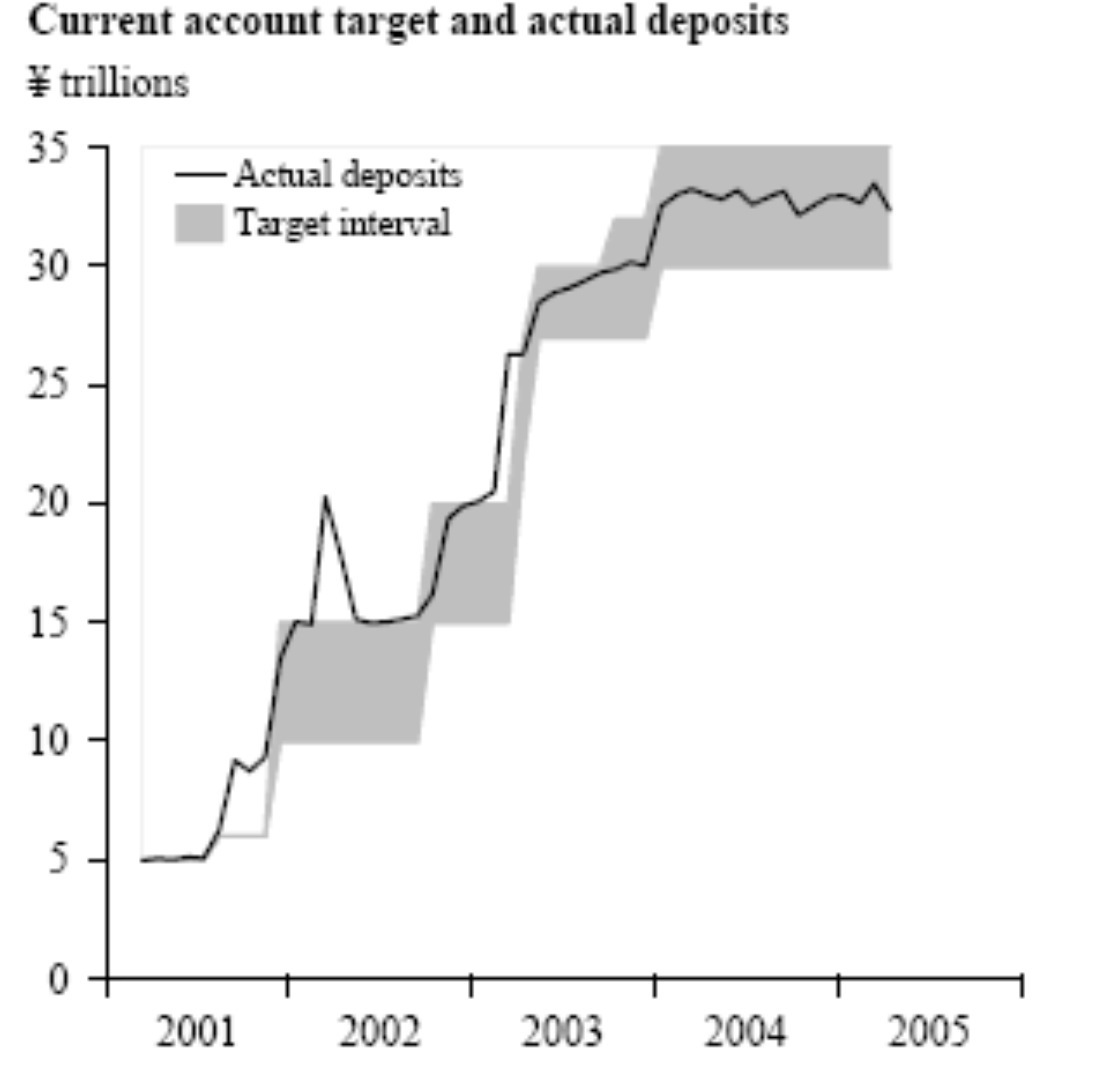

Indeed, this is true. The initial experiment started in 2001 and ended in March 2006: by the end the excess reserves target reached Y35tn. Then the policy was unwound.

The difference, as can be seen in the below chart, is that the current policy starts where the old BoJ finished. Between 2001 and 2006, when the BoJ targeted current account balances at the BoJ, the peak value of excess reserves was around the current level.

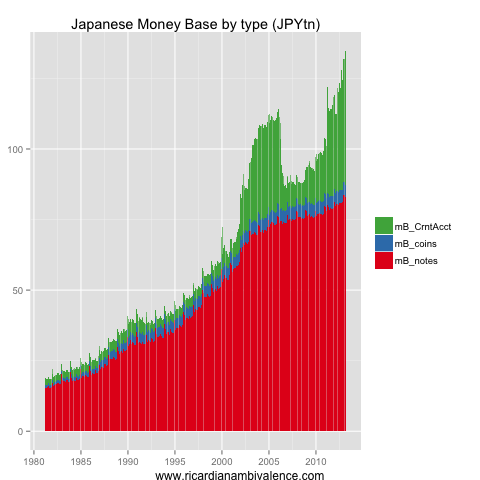

The new policy aims to boost base money to Y200tn in one year, and Y270tn in two years. Most of this will go current account balances, meaning that excess reserve balances will reach around five times the prior peak level.

I do not think that the level of balances means all that much (see here for more on this), but I do think it is a reasonable guide to how much more serious they are this time.

What is different is that the BoJ is now signaling that these injections are permanent or until inflation reaches their target

Yep, that is different too.