Ben Bernanke made a splash in the late 1990s criticising the Bank of Japan. He argued that the Japanese situation (at that stage a decade of stagnation) was one of ‘self induced paralysis’, and that there were options available to the BoJ that would end deflation and support growth.

Since making those comments, Bernanke has found that actually taking his former self’s advice is more difficult — notwithstanding, there is a strong sense in which the arguments he made at that time have been a good guide to the actions he has subsequently taken (the WSJ’s Hilsenrath was writing about Bernanke ’99 in 2010, prior to QE2).

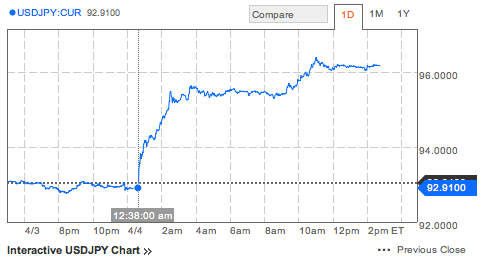

Yesterday, the BoJ’s new Governor Kuroda followed Bernanke’s lead, and surprised markets with open-ended QE. This caused an immediate drop in the foreign exchange value of the JPY and caused the 10yr JGB yield to decline by the largest amount in nearly a decade, hitting an all-time low of 0.425%

My sense is that Bernanke’s demonstration that a central bank retains powerful tools once the zero-lower-bound is hit has motivated the BoJ. Once it was clear that ‘good’ options were available, it became inevitable that politicians would push central banks toward them.

So what did the BoJ actually do (their statement is here)?

1/ The BoJ set a goal of ‘about 2yrs’ for achieving 2%y/y inflation. The 2% target is not new (though it is recent), but this is the most committed they have been to a date.

2/ The BoJ announced a ‘new phase’ of monetary easing — both in terms of ‘quantity and quality’. As part of this, the operational target has been moved from the overnight call rate to the monetary base. The target is now a Y60-Y70tn increase in the money base each year.

For those that are rusty on Money and Banking jargon:

Monetary base = Banknotes in Circulation + Coins in Circulation + Current Account Balances

In Japan, the largest part of the monetary base is currently notes (~62%), with current account balances that Japanese Banks hold at the Bank of Japan the next largest part (~35%). A policy of Y60tn to Y70tn annual increase in base money will mean a substantial increase in the present ~Y47tn of current account balances held at the BoJ (the BoJ’s base reports are here) … likely of about Y60tn to Y70tn per annum.

At over Y47tn already, it seems implausible that Japanese banks are currently reserve constrained in their lending — more likely, they suffer from a lack of good (risk adjusted) lending opportunities. Thus, targeting an increase in base money is unlikely to have much direct impact on the economy. Fortunately, the policy that’s been announced is sufficiently large that we can be reasonably sure that it will move prices in many markets, and these consequences (or ‘distortions’) ought to have medium run impacts on broad macro variables (you can see it in JGBs, the JPY and equities yesterday).

I do, however, think it is a mistake to focus too much on the money base (or Japanese Bank reserve balances). These are a necessary consequence of the BoJ’s open market operations (balance sheets must balance: see my prior note) — not the means by which they will impact the economy. Buying Y60tn per year of assets must make these balances rise — it doesn’t tell us if the policy is (or isn’t) working.

3/ What will they buy and how much? JGBs, ETFs and J-REITS with no upper limit. The targets are now all flow based (Yen per year).

A/ Y50tn per year of JGBs. In addition, they will start buying across the curve (all the way out to 40yrs) and will lengthen their portfolio from ~3yrs to ~7yrs.

B/ Y1tn per year of ETFs and Y30bn per year of J-REITS. The CP and corporate bonds programmes will continue until they reach their targets of 2.2 trillion yen and 3.2 trillion yen — but will not be extended.

My view is that these policies work better the more risk the central bank takes. The more risk, the better the payoff per Yen. The most effective policy would be to buy equities — however it’s hard to avoid deleterious corruption once one starts directly allocating financing in that way.

As an early step, buying long-term JGBs, equity ETFs and J-REITs seems promising.

The next step is convincing Japanese investors (who have thus far been selling foreign assets and buying JPY, to lock in their FX gain) that the BoJ is serious about sticking to these policies. If this is achieved, we may see capital flow out of Japan, which would encourage a further leg down in the nominal value of the JPY.

Aussie Governments at ~3.5% must seem pretty attractive to Japanese investors who are contemplating 40bps for 10yr JGBs.

This piece has made IT!

in three categories as well.

Wow, that’s super flattering. Thanks for your support.

Great news for the Japanese and for us. But I wouldn’t want to be holding JGBs at anything like 0.45%!

I don’t think these sorts of policies work according to what the central bank buys; I think the willingness to buy increases expectations of future nominal growth, which increases V and pushes down the currency, making the expectations self-fulfilling. So even buying less-risky assets should increase equity prices, as it has done already.

I think of the central bank purchases as showing their commitment. If you are timid, you buy 1m bills, if you are aggressive you buy equities and 30yr JGBs. As you point out, expectations are key. In this case, it is expectations about commitment to reflationary policy.

However, in some shorter term (or maybe a medium term), mandates are sticky so the portfolio balance argument (which makes what you buy important) makes sense to me.

Haven’t all asset prices responded pretty rapidly in the past when central banks have indicated they wanted to inflate? We’ve seen the Nikkei outperform Spoos since mid-October.

Do I understand correctly…. Y1tn per year of ETFs??? So the central bank is now explicitly giving free money to ALL Japanese companies that are publicly listed? And that’s just to achieve a miser 2% y/y (then what happens as soon as that support is removed, back to 0%?)

– This really looks like govt subsidies. It’s definitely not promoting open market and cross-national free trading and competition, is it? I wonder when Europe will wake up. We have US, Japan, China breaking all free market rules, and Europe seems the one paying up for it. I think it’s time for Europe and Australia and others to instate import fees for Japanese products, cars and electronics.

– What will separate good from bad investments in Japan and what happens to bad investment when support is removed.

– And we think Aussie cash rates will ever go higher again, while everyone else is printing as much as possible and devaluing their currency?

Ricardo, please explain… WHY do they want to FORCE inflation into the economy? Japan is a very rich country that does not seem do be doing too bad, is it? Unemployment is low, standard of living pretty good, so why? The population is aging and they have a propensity to save, 2% inflation will change all that magically and they will all start to splash out?

They need more growth else they will never close their budget gap and repay their debts — or even stabilise them as a share of gdp.

They print their own money (as they are showing with this framework), paying back debt is not the issue here. Obviously this has also nothing to do with achieving 2% inflation, that’s just an excuse. This is simply the cover for currency depreciation. Internal demand in Japan is not going nowhere, the objective is currency depreciation to support exporters and external demand with the excuse of internal inflation targeting. It’s the “perfect” way to manipulate your currency lower, still within G20 framework. Bernanke docet.

You tell me how the EURO can be still trading at 1.29 (higher than 10 years ago) when they have unemployment above 10%. Europe has to wake up or the dream of a common currency will become a nightmare. It’s getting more serious by the day.

The fact they issue their own fiat unit is related to the necessity of making the JPY collapse. Printing money doesn’t create real resources. To repay their debt someone has to take a real loss. Making the JPY collapse is a means of making that real transfer.

On the euro — it’s been a range trade for almost a decade. They have a solid current account and while they are less coordinated w.r.t. policy they are not much less ‘troubled’ than the US in term of fundamentals.

The EU zone is in much worse shape compared to US or Japan, but unable to join the currency depreciation race (they should), due to Germany’s veto.

Japan unemployment is below 5%, US < 8% while unemployment across the 17 eurozone countries is at 12% for the first time since the single currency was launched in 1999. Germany, however, has an unemployment rate of just 5.4% and trending down, while France, Italy and Spain are all above 10%. With a EURO at 1.10 vs USD (which is pegged to Chinese) EU exporters would help the economy.

Truth is that without the EURO, France, Italy and Spain would be in a much better shape right now, local currencies would have depreciated significantly and helped repaying debt without the need of absurd austerity. Austerity does nothing but worsen the situation and repaying existing debt remains impossible.

The EU should introduce import fees for Japanese products, cars and electronics, when the yen falls below a certain value, so that EU citizens can buy Renault, Fiat and Seat instead of Toyota.

Tax itself rich? If the japanese want to vote themselves wage cuts by devaluing their currency and selling us stuff for less, why should we tax ourselves to un-do their kind deeds?

BTW: “To repay their debt someone has to take a real loss. Making the JPY collapse is a means of making that real transfer”. Yes, the loss will be paid for by those countries Japan exports its products to. Last year’s Japanese trade deficit was only the third since 1980. Hence the need to now engineer a JPY collapse. Nothing to do with inflation targets.

All these things are related. You say that they cannot default as they can print — i point out that what is going on is what you’d expect if they were exploiting their fiat-money privilege.

it does not work that way really. when you lower your currency you become more competitive, your cheaper labour helps employment, but you do not lose / gain your purchasing power as products are sold in your country on the base of you can afford to pay not their intrinsic value. for instance a business class ticket from rome to sydney and back is way cheaper than sydney to rome because australians can afford to pay more. Same thing for most pruducts just compare prices of identical things in the us with australia. So we have global ‘free’ markets where goods are traded freely but this all currency thing is a black box and why would europe accept a weaker yen when they have much worse employment ?

That may have been true before, but i think the internet has made pricing much more global. That is part of the reason online shopping is growing so strongly in Australia — because as the AUD rises, the price of online goods declines.

if you import , yes, it gets cheaper, but there is a lot that you can’t import directly (because foreign producers does not allow it, you gotta buy locally) or it is not phisically easy/practical to import yourself. that stuff is still a big chunk of what we consume and it is priced based on what we can afford to pay, and currency movements do not make it more affordable. Otherwise we would have deflation in Australia now after a massive 20% increase in the currency but we are far from it.

also according to your theory we should see massive inflation in japan now after the currency has collapsed but we won’t becasue exporters into japan will have no pricing power refardless what the yen is doing and local producers will undercut them.