The March non-farm payrolls report was about half expected, printing at +88k (mkt +193k: range +170k to +230k). There was some support from revisions, which added 61k to the prior estimates: +29k to January (now 148k) and +32k to the February estimate (now +268k).

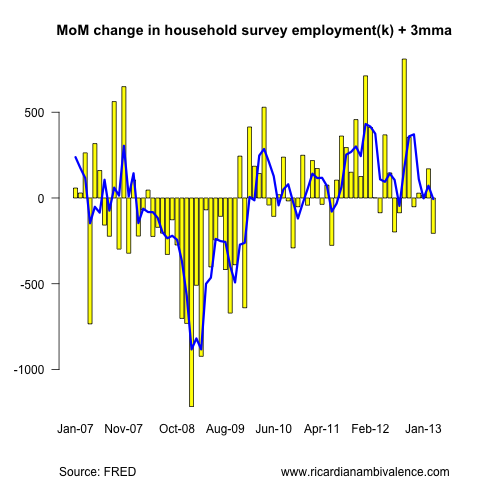

The household survey was worse, showing an employment decline of 206k in March.

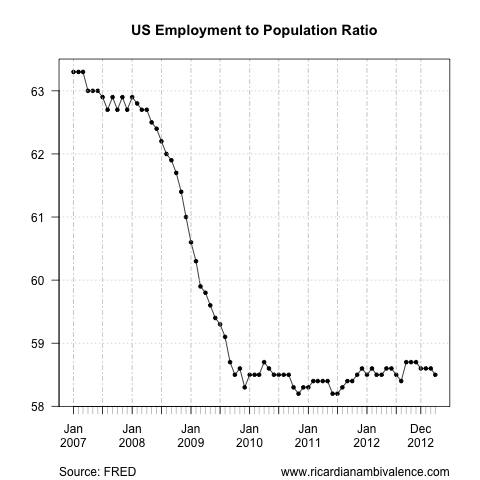

The number of the unemployed declined further (-290k) which resulted in a decline in the participation rate of 20bps, to 63.3% — which lowered the employment to population ratio to 58.5%. At least on this metric, it’s hard to see any recovery from the crisis.

It’s almost like something happened to part of the population — one day 4% of Americans woke and couldn’t go to work … economics doesn’t have any satisfying explanations for such waste.

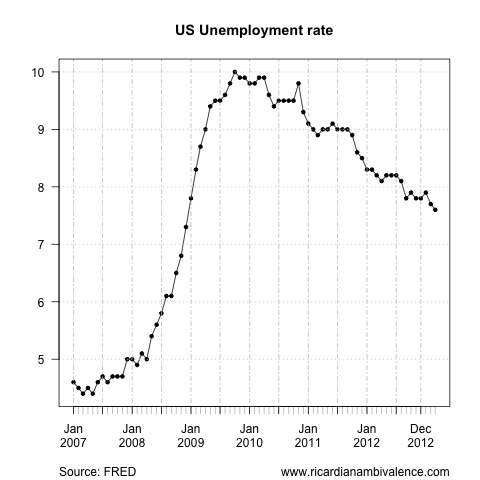

Reflecting this, the unemployment rate declined — for BAD reasons — by 10bps to 7.6%.

The main interest in the labour market report is due to the FOMC labour market focus — the market wants to know and how long they’ll retain their present ‘open ended QE’ policy. This report suggests to me that their is no end to their purchases of 85bn / month in sight.

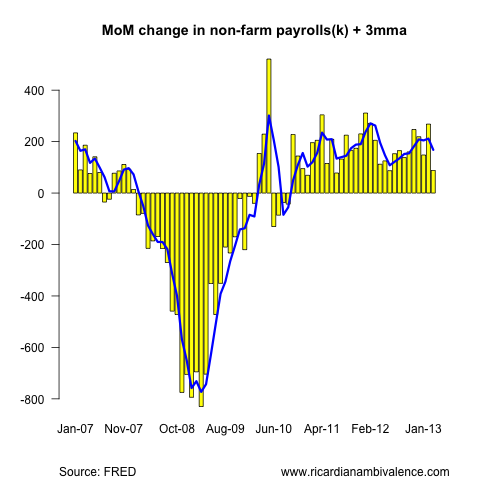

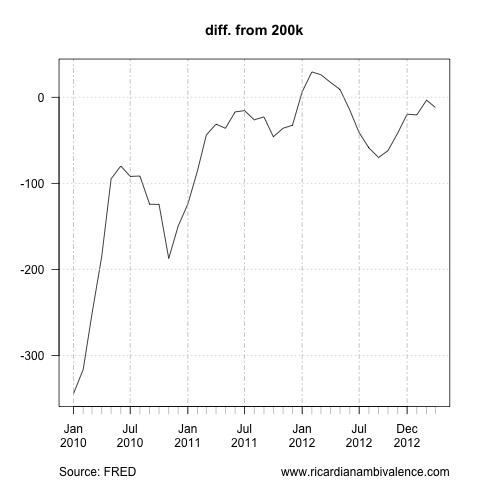

One test that’s been set out is sustained employment growth (in the establishment survey) of ~200k per month. To summarise this test, I show the difference 6mma of employment and 200k in the below chart.

As you can see in the above chart, the six month average of employment growth got close to a +200k average in recent months — however the recent weakness has kept the average just below the level. At 188k in March (down from 197k in Feb) we are close, but not quite there. To get the FOMC to change tack, i think we’d need to see the 6mma of employment above this level for around six months.

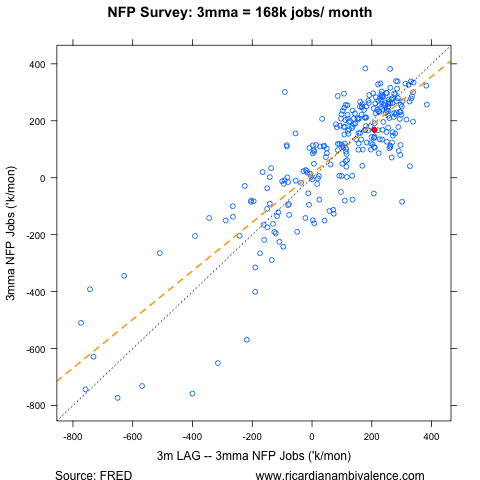

Monthly surveys are very noisy and subject to heavy revision, so I think it’s best to look at moving averages. Things still look okay in 3mma terms.

The above chart shows the 3mma of establishment employment growth lagged by three months against the most recent 3mma (the highlighted point is the most recent pair: the x-coord is the 3mma of employment growth to Dec’12 & the y-coord is the 3mma of employment growth to Mar’13; the orange line is the regression slope [1990 -> present] and the black line is the 45′ line). This shows that recent employment trends are consistent with prior trends — which means we probably have a stable US labour market.

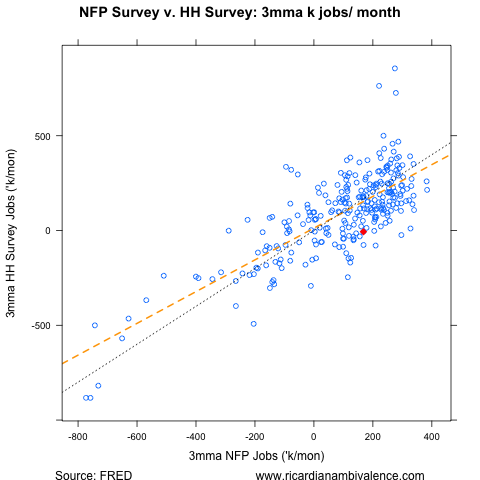

I doubt that the weakness in the household survey’s measure of employment is telling us about anything more than sampling error. Compared with the Establishment survey, the (3mma) of the household survey looks a bit low just now. It’s probably noise — and therefore nothing to worry about.

The so-called ‘leading details’ of the report look okay to me.

The construction sector in particular is showing healthy employment growth (+24k, +49k and +18k the last three months) — which doubtless reflects the recovery that’s underway in the US housing market.

Manufacturing employment growth remains modest (+14k, +19k and -3k the last three months), however it is at least improving somewhat.

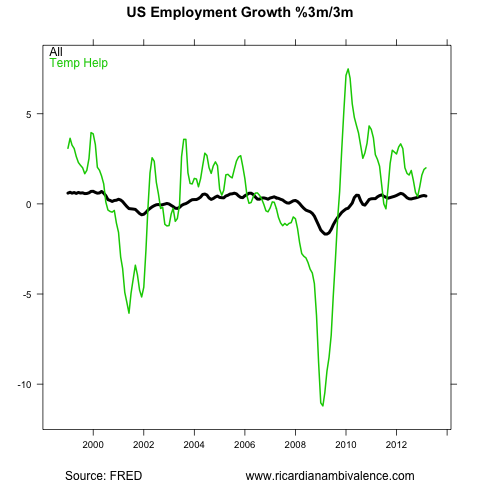

Finally, growth of temporary hiring — which is often a leading indicator of general hiring — is holding up well (+12k, +23k and +20k the last three months).

Thus, while the weak headline number (88k v. mkt 193k) was fodder for Bond Bulls — and was not liked by the equity market — I doubt the overall report represents a particularly sinister change in the broader US labour market. It marginally reduces the probability that the FOMC will slow their bond buying — but then I always expected that the policy would remain in place for the duration of 2013.

On balance, therefore, it’s should have been good risk assets and bad for the USD (okay data plus delayed monetary tightening ==> good for risk).

Thanks. You’ve been busy – no lazy Saturday morning breakfast for you! ECRI just posted saying y/y NFP growth is at a 19 month low. Not sure what that’s meant to mean.

The falling participation rate has been happening here too, although to a lesser extent. Baby boomers giving up? I think the data here suggest its been younger job-seekers dropping out, perhaps not helped by labour market re-regulation.

I think both the Fed and the BoJ need to incorporate a positive rate of change in their monthly bond-buying, to show that they want to reach their targets quickly. Say, 10% extra for every month they miss their target.

The participation rate issue is puzzling. The fact demand is depressed globally suggests low demand has played a part — but equally, the lower returns to both job search and employment suggest there is a supply side part to the explanation.

It sure is an odd global development.

You are on fire but you do need a life

Did you see that delong linkedto us? Just a tiny link in his noted, but still nice.

Congrats. You are entering the big time! Interesting to see if you get a spike in views.

That’s how i noticed it. It has only been modest so far, but notable.

ooops. yes QE = higher share prices.

But the real economy that’s a different thing. Do you really believe that printing money = jobs = prosperity? That would be a bit too easy wouldn’t it? if the real economy will recover in the US, it will have nothing to do with QE. yes money is cheap to borrow, but you need to put that money to work in something useful. It was the housing bubble that got employment to 5% in the us, now we are searching for the next bubble! until found there’s nothing QE will be able to achieve. Current conditions in the US are normal, not the last decade. it’s an epochal change and there are people still talking abut ‘cycles’ (especially here in Australia)

I believe that in a rigid labour market that a little final price inflation can improve general employment prospects by lowering the user cost of labour. I think that QE helps achieve that in a roundabout way via boosting asset prices

yes, QE got shares back up where they were, for those who are lucky enough to actually own shares. Housing recovery is hardly keeping up with inflation after a big decline and employment to population is going nowhere after 5 years of money printing. All of which would have happened anyway. QE has put lots of fuel in the tank but the driver is reluctant to go anywhere after the big crash.