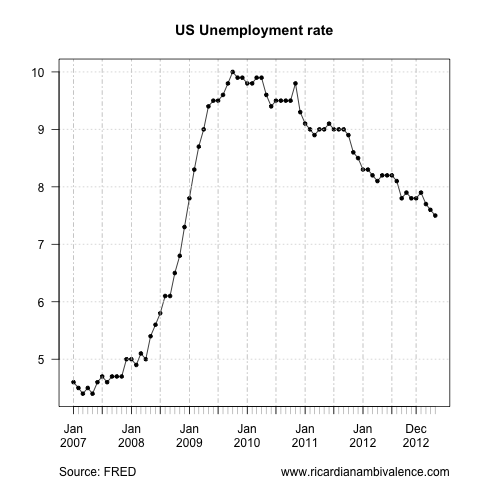

The April non-farm payrolls report surprised on the high side, with 165k jobs added (the bloomberg median forecast was +153k) and the unemployment rate falling 10bps to 7.5% (mkt was unch at 7.6%).

The revisions were extremely positive, with March revised up 50k to 138k, and February revised up 64k to a whopping 332k.

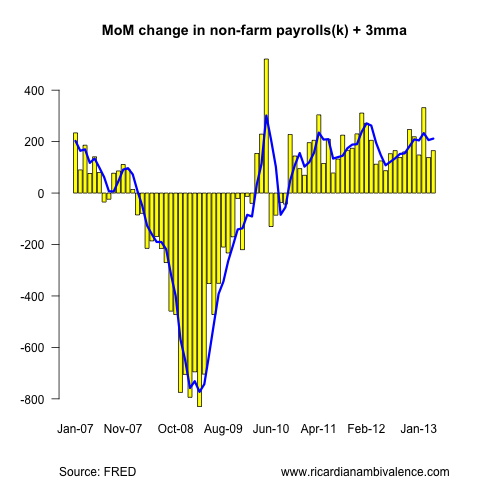

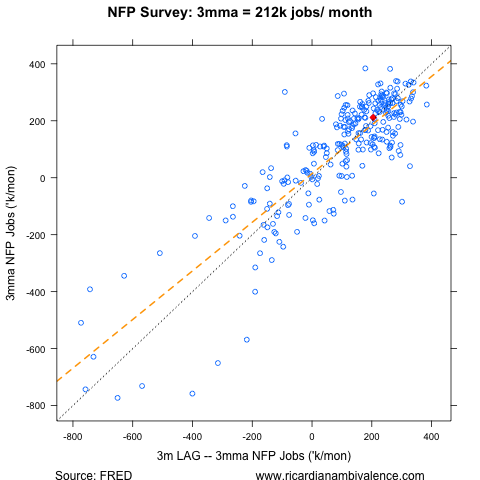

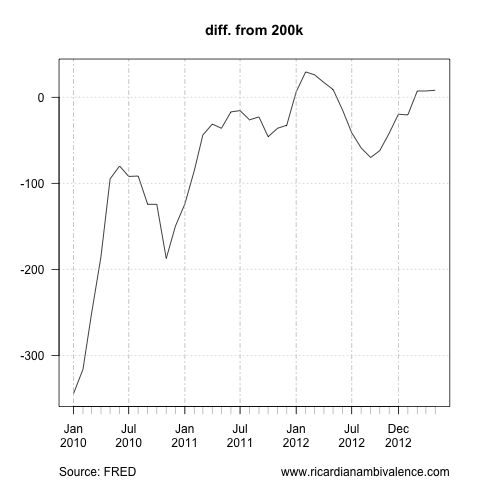

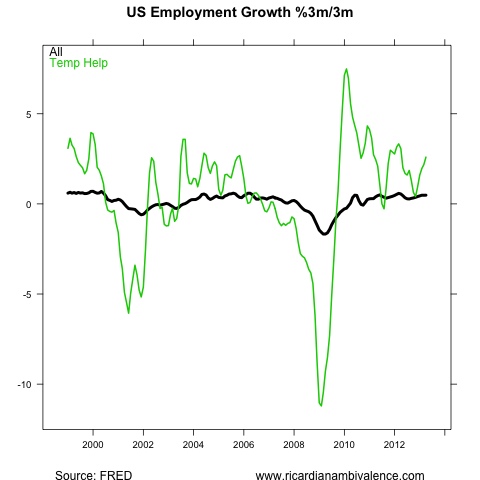

This is around the +173k jobs per months average of the last year, and it has taken the three month average to 212k (the fifth month in a row that the 3m average has been above 200k).

This is a result that’s fairly consistent with recent trends in the labour market, though further gains of this kind are required to get the FOMC to consider reducing the pace of their balance sheet expansion.

A 6m average that’s sustained above 200k per month for about a year is probably required to persuade the FOMC to change their policy, and after the revisions we can say for sure that we’re moving toward that target.

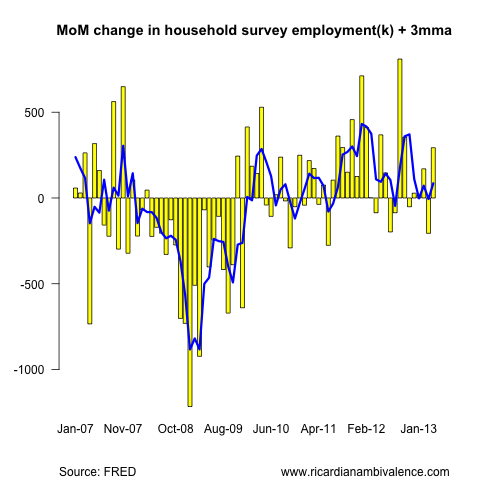

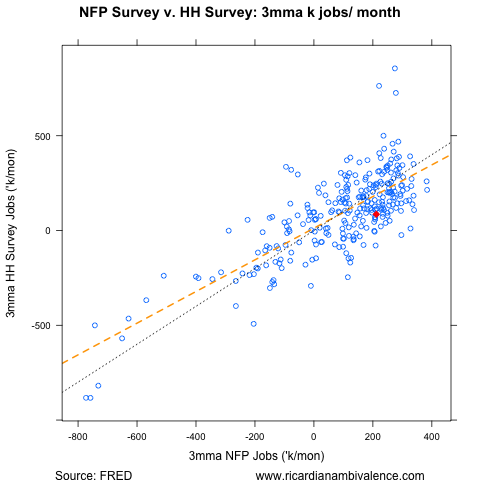

The household survey showed a similar increase in employment (+293k), however this survey is not as positive in trend terms (the 12m average is 137k).

The household survey remains weaker than you’d expect given the strength of the establishment survey. It should balance out in due course (when all the revisions come in) — if you’re looking for the weakness in this data, it’s in the household survey that you’ll find it.

The unemployment rate continues to trend lower (it has been a remarkably smooth decline, if a fairly gradual one), and this time it fell for a good reason — more people in work.

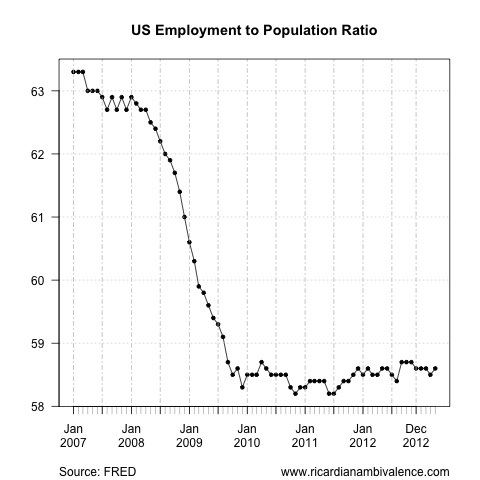

The long term non-recovery of the employment to population ratio is a little frightening; but the news in April was good. The employment to population ratio rose 10bps to 58.6 (though it’s only up 40bps from the post crash low of 58.2%).

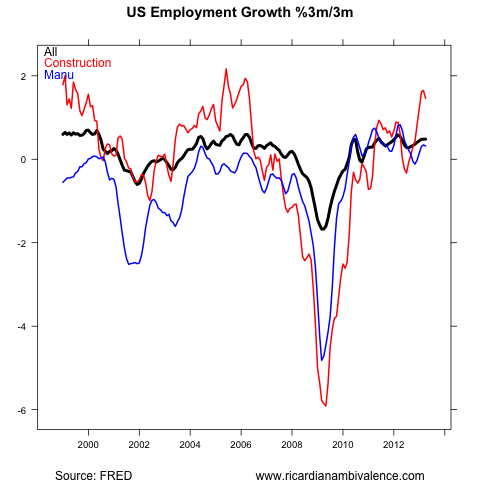

The cyclical sectors look okay, particularly construction — doubtless reflecting the improvement in US housing.

However, the signs are good outside that sector also, with ‘temporary help’ jobs also growing strongly.

All up, this is a good payrolls report. Combined with the decline in initial claims, it seems possible that we’ve navigated the worst of the Q2 data slump.

What? Jobs are being created even with inflation falling?

Just imagine what might be achieved with a little more inflation!

I feel more confident if projects are started based on their intrinsic value rather than because “prices always go up”. I reckon it’s better to have low rates and inflation and solid economic growth, rather than higher inflation and people “investing” just because they do not want to miss the boat. Obviously when unemployment was at 5%, lots of people were working on the wrong projects. We found that out too late. Thinks how nice it would be to keep low inflation (including house prices) and a jobless rate of 5%! Much better and more solid than high inflation and a jobless rate of 5%!

shaves RBA probabilities on tuesday–but they could still go; very much line-ball call. anyone who says otherwise projecting their naivete

yeah, i think it does shave the probability. in my mind, it’s a demand test — and if global growth is holding up, i don’t see how they can downgrade demand.

But jobs are actually lagging the economy; data in April was pretty much very weak world-wide, including trade data in almost every country. Even on Friday we got weak data in the US outside the jobs number, but pretty much ignored by markets. Huge revisions too, what if they revise negative next month.

I now reckon it’s going to be a cut from the RBA or most likely a statement that is preparing for a June cut …. -5% building approval last week and only 3.9 % y/y does not point to strong housing activity. State by state, only WA and NSW improving:

http://www.abs.gov.au/ausstats/abs@.nsf/Latestproducts/8731.0Main%20Features3March%202013?opendocument&tabname=Summary&prodno=8731.0&issue=March%202013

Then a lot will depend on the job numbers next week and capex numbers.

if only the public sector grew as much they did under Reagan the Fed would be raising rates.

This of course is a very late addition to ATT!

Thanks.

I think you fit in very well with the Mark Thoma’s, Brad De Longs, Peter Dormans, Barkley Rossers , Jim Hamiltons, Menzies Chins and gasp the sainted Paul Krugman

Heady company indeed.