Krugman famously said that in a liquidity trap, a central bank must make a ‘credible promise to be irresponsible’. In Japan’s case, that’s going to show up as a weak JPY — which will lift their economy via an increase in net exports.

The MoF’s latest weekly capital flows data suggests that Kuroda has more work to do on this front with the home audience.

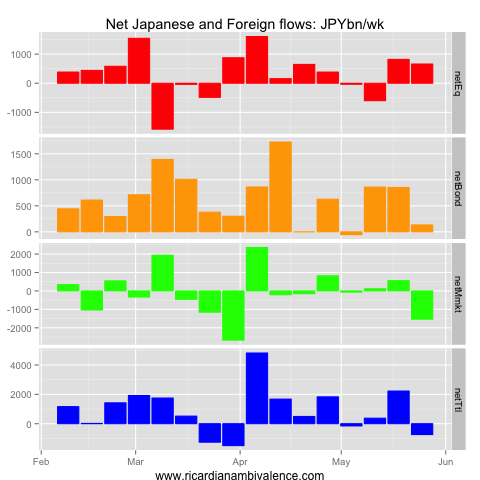

The current and capital accounts must always balance, so a larger current account balance (higher exports and fewer imports) ought to show up as an increase in capital outflows from Japan. It follows that we ought to be able to see that the BoJ has traction from the securities flows data — when the BoJ has convinced Japanese investors that inflation will erode real returns, we ought to see capital flow out from Japan.

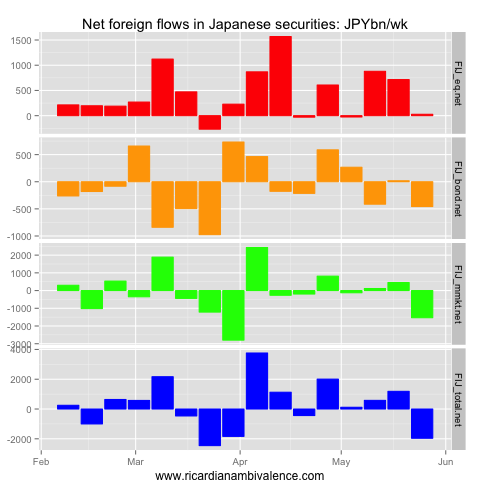

Netting Japanese flows in foreign securities and foreign flows in Japanese securities, we are left with a small net outflows from JPY — due to a large outflow from short-term Japanese paper (Y5tn of sales v. Y3.5tn of purchases).

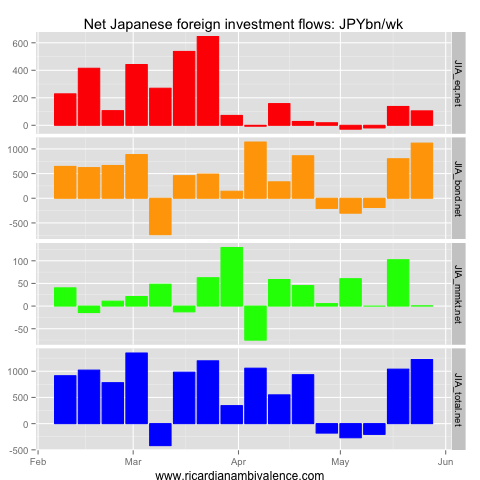

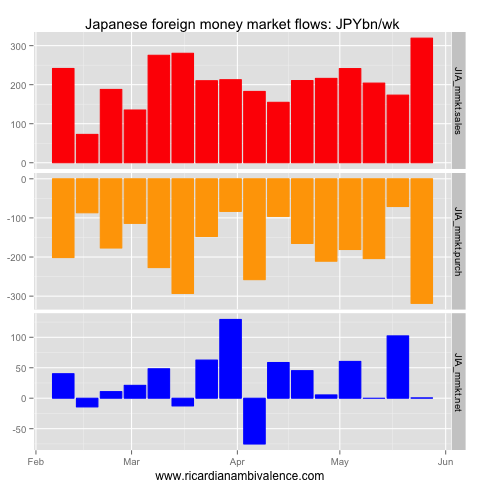

The basic story on this side is that net selling of foreign assets appears to have slowed merely due to Japanese holidays.

When the Japanese came back to work, they re-started selling foreign assets — I suspect they are taking profit on JPY shorts.

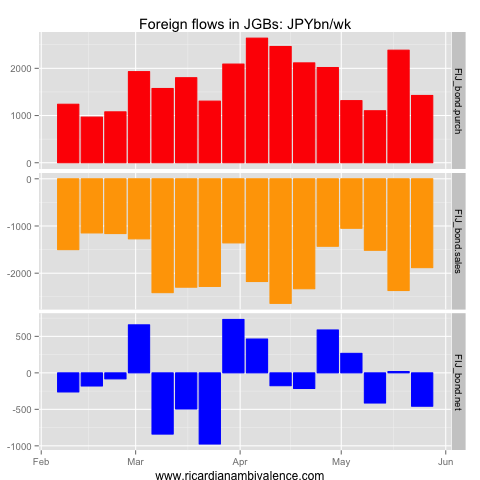

In the past two weeks, Japan has stepped up their selling of foreign bonds — and this has outpaced the increase in sales, resulting in a large-ish net-bond outflow. Japan inc sold ~Y1.1tn of bonds in the week ending 25 May.

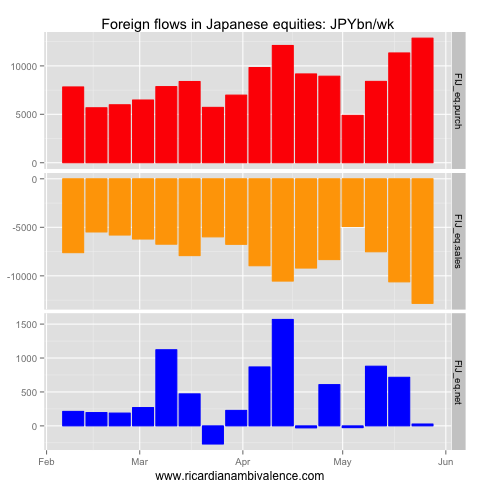

Similarly, foreign equity sales have picked up a little – taking the net flow to -Y105bn in the week ending 25 May.

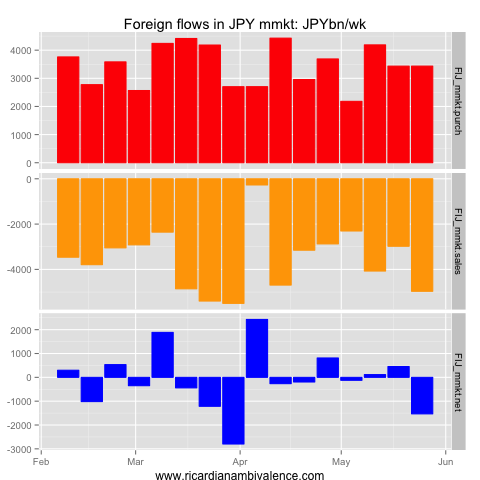

Money market flows picked up in both directions — but the net impact was zero for japanese holdings of foreign short-term paper.

On the other side of the ledger (foreign flows in Japanese securities), the BoJ appears to have more credibility — with foreign flows out of bonds and money market instruments.

For the week ending 25 May, foreign accounts net sold Y2tn of Japanese assets, with around -Y1.5tn of these japanese money market instruments, and ~Y500bn of bonds and notes.

For the week ending 25 May, foreign accounts net sold Y2tn of Japanese assets, with around -Y1.5tn of these japanese money market instruments, and ~Y500bn of bonds and notes.

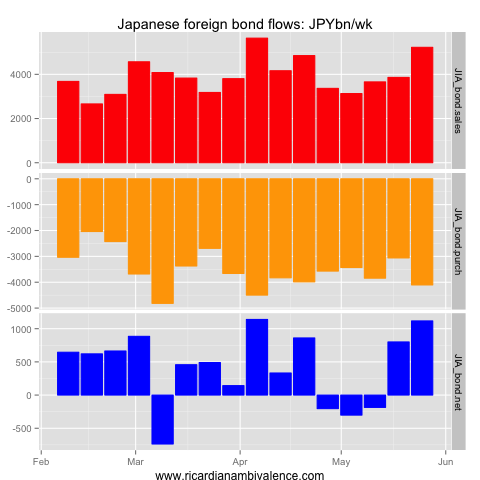

The volatility in JGB yields is doubtless chasing funds out of Japan. The foreign sector has really pared back their purchases in recent weeks, and sell flows remain elevated, so net outflows continue (Y500bn last week).

The real foreign investment (into Japan) bubble is in equities — but we’re not yet seeing the capitulation trade. Who knows how many people were long on some Macro-story they do not understand?

The real foreign investment (into Japan) bubble is in equities — but we’re not yet seeing the capitulation trade. Who knows how many people were long on some Macro-story they do not understand?

My guess is that foreign net selling of Japanese equities will have spiked higher in next week’s data.

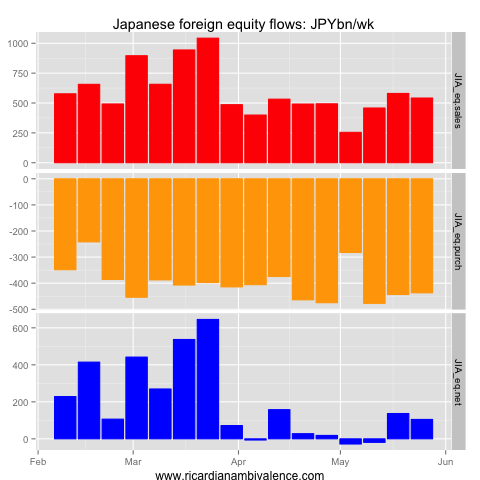

Finally, we have a Y2tn increase in money market sales, without a change in purchases, leading to a net Y1.5tn outflow in the week ending 25 May.

Finally, we have a Y2tn increase in money market sales, without a change in purchases, leading to a net Y1.5tn outflow in the week ending 25 May.