Boston Fed president, Eric Rosengren has been dovish (and right) for the past few years. Reading the FOMC minutes, my guess has been that he is the one that wants more stimulus now due to low inflation.

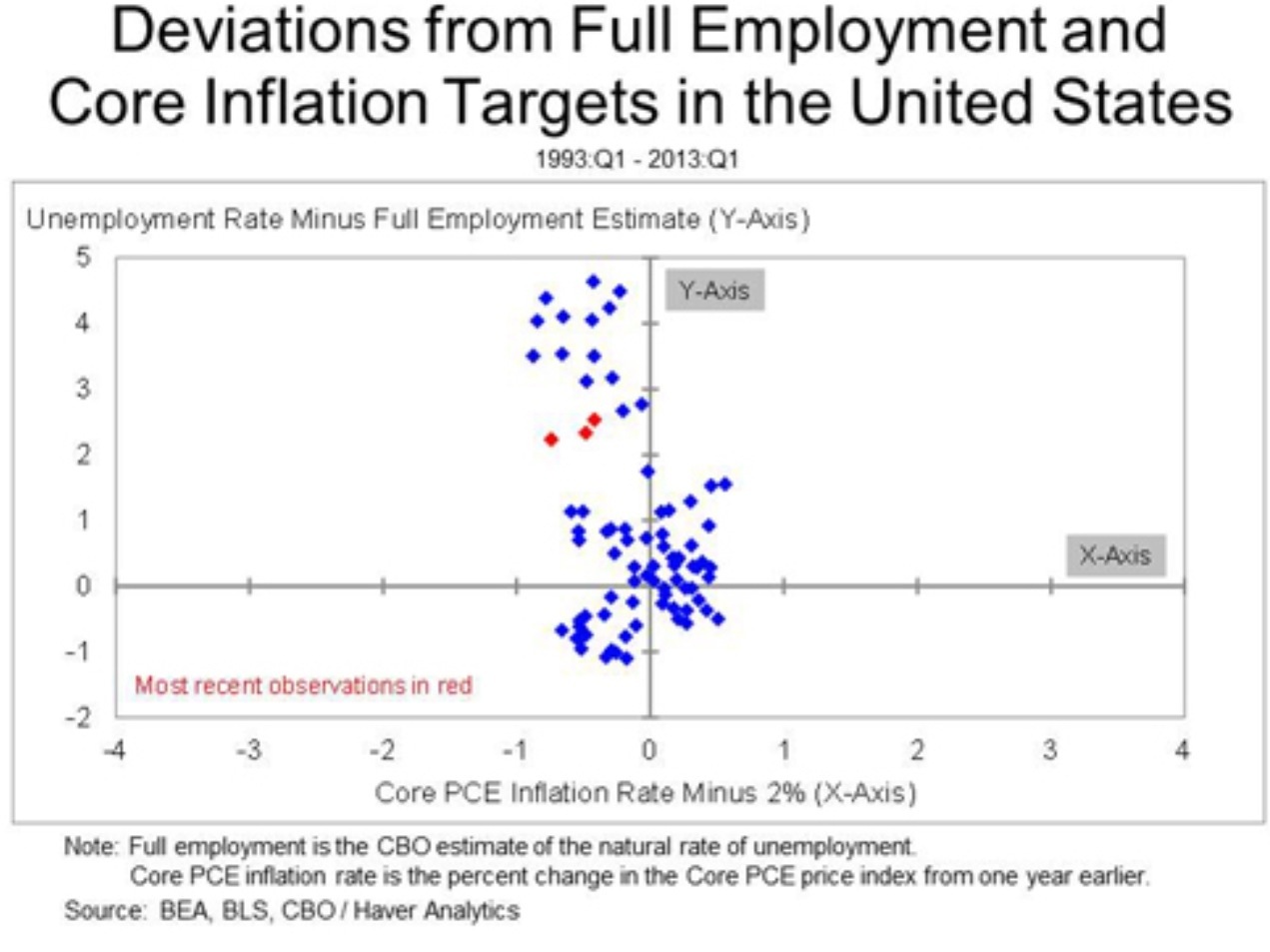

The fact that he was packing the following chart tends to support this hunch … But

His speech overnight suggests he has changed his mind (or that i was wrong, in which case arch dove is likely to be Kocherlakota).

In terms of monetary policy, it would in my view be premature to stop the Fed’s large-scale asset purchase program at this time. I believe the Fed should continue the purchase program until we see more sustained improvement in labor markets and have greater confidence that the economic recovery is sufficiently self-sustaining to yield continued progress in reducing the still very high unemployment rate.

However, I would also say that it may be undesirable to abruptly stop purchases, so it may make sense to consider a modest reduction in the pace of asset purchases if we see a few months more of gradual improvement in labor markets and improvement in the overall growth rate in the economy – consistent, by the way, with my forecast, which is somewhat more optimistic than that of many private forecasters.

What’s going on here? The FOMC are missing badly on employment and inflation, but might taper soon? I think it is the old stock-flow debate. The FOMC thinks it is the stock that does the work – so they will not have tightened until their balance sheet shrinks. The market, however, thinks it is the flow!

I would reiterate that with an open-ended asset purchase program, changing the flow of purchases does not necessarily yield, in the end, a smaller central bank balance sheet. That would depend on having a fixed point for cessation of purchases, combined with a lower flow of purchases. So, even if we were to adjust the rate of monthly purchases, the ultimate size of the Fed’s balance sheet would depend on the point of cessation. If economic growth proves sufficient and the purchase program was not extended over a longer time period, the size of the balance sheet could be smaller than otherwise.

We will see if the Fed holds their nerve when they actually taper … The exits from QE1 and QE2 suggest the equity market won’t like it, and that may undo the economic argument for monetary tightening from higher inflation, and ultimately cause the FOMC to reverse track.

In any case, with Rosengren talking tapering it seems like the FOMC is headed toward the exit, probably at their September or December meetings (which are followed by press conferences).

Yes, of course it’s the flow, or more specifically, the flow relative to expectations. If the FOMC members don’t understand that, they don’t understand their own policy.

Central bankers around the world seem profoundly uncomfortable with increasing the money supply when nominal rates are low.

Flow or not flow, it can’t go on forever. There will be a point where it stops and markets will have to deal with it. The longer they wait the more disconnected with reality financial markets may become and the risk of a disorderly exit gets bigger. So I think it’s good to start talking about this now, it prepares expectations now.

I’m sure that’s the view of many FOMC members and market economists. The problem is that the policy doesn’t fully work if the markets think the Fed believes it can’t go on forever. The policy works through backward induction and the more credible the Fed’s determination to inflate ‘whatever it takes’, the faster the policy will work and the less they will have to buy.

Well, it would go on “forever” if the economy never picks up (hopefully that is not the case). But I see nothing wrong with saying that the Fed are “considering a modest reduction in the pace of asset purchases if we see a few months more of gradual improvement in labor markets and improvement in the overall growth rate in the economy”.

Another quality article which almost becomes a tautology in your case

Thanks. Very kind :)

Can I just say with no hyperbole at all I have the greatest musical taste in the world!

I just hope they can avoid the same crazy stuff that’s going on in Japan right now. More than investing is becoming a gamble there. Volatility is just crazy. That can’t be good for the economy.

what’s your take on capex? have we passed the mining investment peak or not? are other sectors ready to take over?

doesn’t look great to me, but more like a slow grind lower than a plunge just now. On the principle that the first thought is not the best i am working on a few things before i post.

Our mate has three entries this week. He is top of the list examining the US!! and what a list of stars it is

Wow, thanks very much. I don’t think i am quite that worthy!

Homer, just realised it’s you – I assume it isn’t a secret, as it’s on your blog. I remember you from Catallaxy (won’t disclose my pseudonym there). I’ve stopped commenting there, as its gone a bit too feral even for my political leanings. Kates is a bit mad and Samuel J seems to be a good contrary indicator for just about everything… Thanks for the links. I got value out of Matt Cowgill’s posts. I was aware of him through his tweets, but Twitter always seems to bring out the worst or least worthy in people (eg The Kouk). Not impressed with Andrew Elder’s conspiracy-laden post though. Cheers.

Probably at the peak around now but we will not be falling.

competition.

Who is the biggest star on My US list? Is it RA?

Rajat,

I do not agree with every link but they are all interesting. I made a point of that this week.

It is great weekend reading from a variety of sources not the least Our mate here.