In my recent post regarding central bank balance sheet operations and bond market term premium (see how QE works), there’s a rather large unexplained divergence between model and reality in the most recent period.

A reason for this may be the ‘regulatory bond-bid’ – by which I mean that changed banking regulations have increased the private sector’s demand for high quality liquid assets, and an increase in demand ought to raise the price.

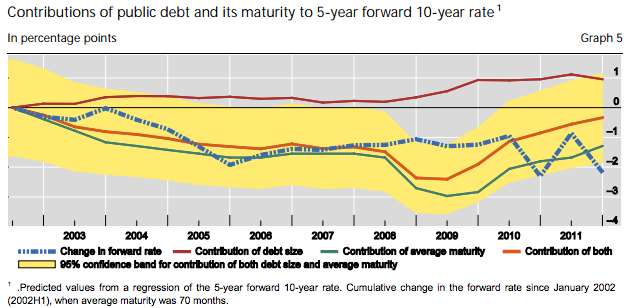

This subject (among other things) is covered in over 50 pages of detail in a recent BIS CGFS paper (No 49).

For example, I was surprised to learn that:

Current estimates suggest that the combined impact of liquidity regulation and OTC derivatives reforms could generate additional collateral demand to the tune of $4 trillion. At the same time, the supply of collateral assets is known to have risen significantly since end-2007.

While the CGFS pitch this as a wash, in the context of the long term bond-yield model in the QE working paper, it probably means that the part of the model that relates to the increase in debt supply over the prior five years ought to be ignored. If this is the case, we can lower the model bond yield forecast by ~100bps.

This explains about half of the divergence between the historical bond model, and recent market pricing. On this basis, one would have to think that ~4% for 5yr fwd 10yr yields would be plenty high enough. As it turns out, 5y10y IRS (which is only a bit higher than bond forward, and but easier to price) peaked at 3.97% on 11 June.

Given this, it seems like the market had indeed sold off ‘enough’ by the time the Hilsenrath article taper-off blog post was published …

Also in the CGFS note is a neat cross-country chart on the changed composition of bank funding over time. This shows the massive progress Australian banks have made in rotating their funding base away from short term money markets, and toward retail deposits (note also the odd decline in term borrowing by European banks — that is the sign of true de-leveraging in Europe … they don’t need to borrow as asset books are being wound down).

Look your output is fantastsic and the quality is always there ( except when you cochrane!!) but seriously do you do anything on the weekend but work?

i do take holidays …