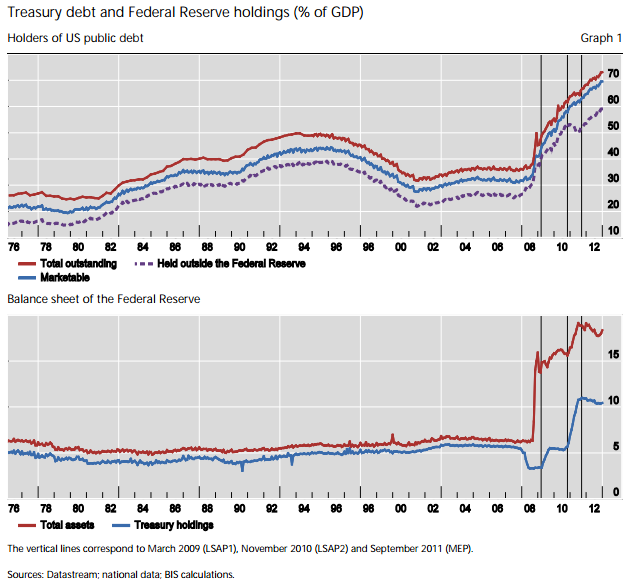

The BIS has just published a paper which traces the main path through which QE works to stimulate the economy. It shows how the size and average maturity of government debt in private hands influences long-term yields, and how the FOMC is working to lower those yields via QE (their LSAPs or large-scale asset purchase program).

So how does it work? By crushing the term premium (it’s a preferred habitat thing).

Over the last few years, as the Fed’s balance sheet ballooned, it massively increased (among other things) holdings of term US Treasury debt.

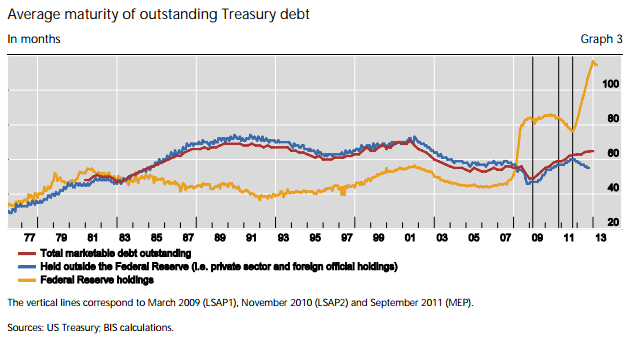

The theory is that the greater the term of the debt the Fed purchases, the greater the boost to the economy (the more duration risk they take out of private sector hands, the more risk the private sector has to seek elsewhere). So when the Fed wanted to boost the economy but was unable to cut rates further, they purchased a greater share of longer term bonds — you can see the particular impact of twist on the portfolio in 2011.

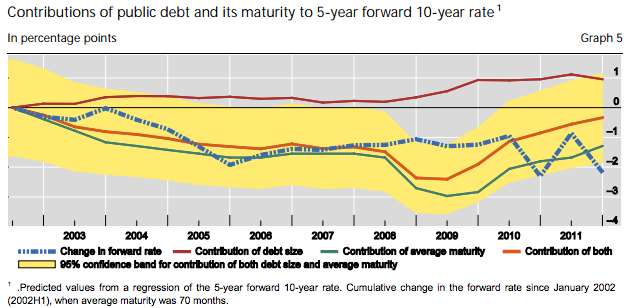

The result has been a decline in modelled term bond yields (and a larger decline in actual yields).

Splitting the contributing factors up by type, the increase in the stock of debt on issue has worked to increase long-term UST yields, while the decline of the average maturity of debt held in private hands has worked to decrease bond yields (again, note that the actual decline is a little larger than can be explained by these two effects).

The reasons term debt yields may be ‘too low’ (relative to model) are many: some that come to mind (apart from model mis-specification) are subdued economic conditions, and the depressing effect of ‘forward guidance’ (both in terms of improving the carry, and perhaps shading private sector expectations about the future).

In my view, the term-premium impact of LSAPs is the second channel of monetary policy at the lower bound. The first is expectations (or forward guidance) — but when promising low rates for a long time isn’t enough, a central bank can boost activity by lowering the term premium (of course, it follows that a Treasury can un-do this by issuing more term debt).

Excellent but please do get a life

The question we should be asking is HOW LONG can Q.E work, how many more years, decades.

It inflates asset values higher than they would otherwise be (bernanke even states this) increasing confidence/spending/hiring. So assuming that it needs to be restarted shortly after it is stop’d. (Or hopefully it is before the asset collapse sets in motion> banks below cap req> bank bailouts on over indebted gov’t credit cards> bond market “instability” restructuring of global monetary system.) assuming those dominos dont fall and under assumption elevated asset values (like we have) are continued or quickly restarted (if silly notion of ending QE is attempted) how long , decades? Can QE continue successfully keeping economy afloat. I think this is a huge question

I think they can buy assets without limit – the risk is that a sort of ricardian equivalence takes hold and prevents it from being stimulatory – after all the taxpayer owns the central bank.