[is this thing still on?]

It’s been a long time since I blogged, but today’s RBA statement has lit a modest fire …

Before I riff on what’s wrong with the Bank, let me put down some context. The Bank’s main job is to keep inflation at 2.5%, with a control range of 2% to 3%.

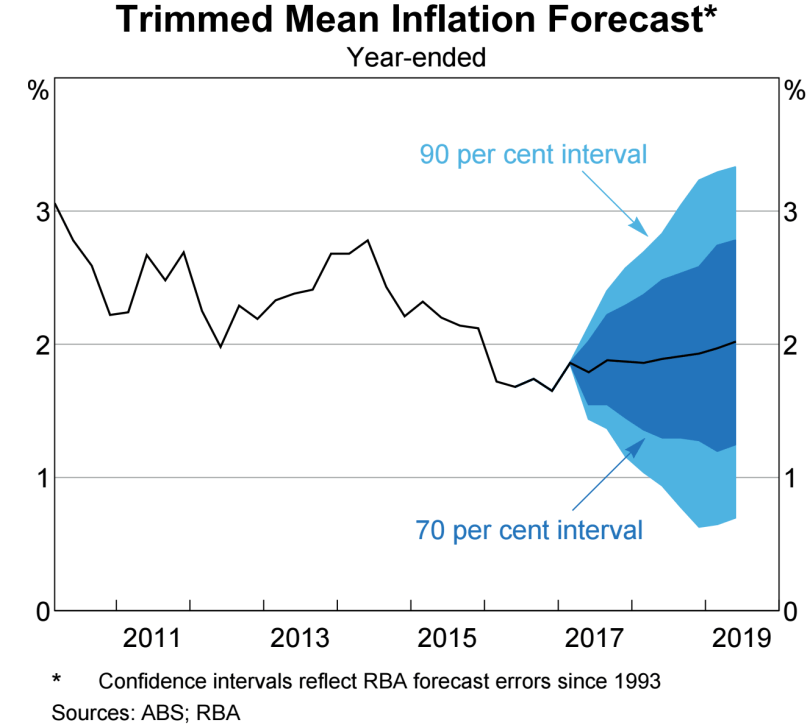

At present, inflation is both below the 2.5% target and below the 2% to 3% control range; and it is not expected to get back inside the control range until some time in late 2019. The chart below is from the RBA’s Q2 SOMP, and it captures their failure … sorry boss, i’m missing my target and i don’t know when i’m going to hit it. Given the gentle up-slope of their CPI forecast, i would say the central case is a return to 2.5% inflation around 2025 …

Given that the NAIRU is probably 5% and that we’re around 5.75% just now, monetary policy should be easy: it’s either on hold with an easing bias, or cutting, right?

Well that’s so pre-GFC. RBA Gov Dr Lowe was an early contributor to the financial stability literature, writing papers in his time at the BIS (with Borio) which encouraged central bankers to take a different view:

central banks should consider paying greater attention to credit in their monetary policy strategies than is generally the case at present. Specifically, simply setting monetary policy so that a two-year inflation forecast is at the central bank’s target may, on occasions, be less than optimal.

Gov Lowe and Assistant Gov Kent even wrote a paper together in 1998.

So rate cuts are not on, given the highly-leveraged Aussie household balance sheet and the recently rapid appreciation of house prices. That’s a bit inconvenient given the yawning gap to the inflation target and the troubling state of the labour market (at best mixed, probably trend loosening) and the still-bleak capex outlook.

So what to do? Cheer-lead.

GDP downgrade? No problem, it’s still going back to 3.25% … 3.25% is like the horizon, always the same distance away …

Remember how they dropped 100bps of GDP when Q3 GDP unexpectedly contracted due to ‘temporary factors’?

And today they downgraded Q1 GDP in their words.

But it’s all no problem, because it’s going back to 3.25% in a few years time, right?

What’s the point of being downbeat? They have already decided that they cannot cut, so they might as well tell business that the medium term outlook is okay. Perhaps it’ll boost business investment and help to solve their problems?

It’s not working so far. The ABS Q1 Capex report was bleak. After making all the nerdy adjustments it suggests that investment is going to crash by 10% in 2017/18 — this means that the RBA’s growth forecasts are about 100bps too strong.

What does the RBA say?

the transition to lower levels of mining investment following the mining investment boom is almost complete. Business conditions have improved and capacity utilisation has increased. Business investment has picked up in those parts of the country not directly affected by the decline in mining investment.

Well maybe … except that firms told the ABS that they plan to spend less in 2017/18 than they did in 2016/17.

I suppose that there’s no point talking about it unless you are going to do something about it … might as well get out the pop-poms and cheer-lead.

Maaate,

It has been far too long. I hope we can have some more semi-regular basis at worst.

I have given your article publicity on my humble blog

i promise i will be more frequent — easy bar! also, please add a link to your blog. thanks for your support

I really should comment. No The RBA should not cut. It won’t do anything but fire up housing. If you think the economy needs a push then Infrastructure spending via the budget!!

What i am sure of is that they believe they should not cut. This means a longer period at 1.5% and lots of cheer leading. Who knows what the right price of housing is? we ought to also be critical of housing policies. we might have lower rates and cheaper housing in an alternate scenario.

hmm sounds like a subject for a future article ( hint hint).

It is fantastic you are back as well.

Welcome back Ricardo! I fully agree with your post and great to see you calling out the RBA’s BIS-style BS. I had no idea Kent was a co-author with Lowe on the bubbles-monetary policy theme, so it doesn’t seem likely we’ll get any injection of sense from him.

The longer they carry on like this, the more the inflation target loses credibility and expectations become unanchored, which means they will eventually have to cut by more to get back on track.

You’ve referred to the inflation fan chart from the SoMP, but the underlying inflation forecast in Table 6.1 says 1.5-2.5% for year-ended in Dec 2018, but 2-3% in Jun 2019, which doesn’t seem to square. Any thoughts?