First of all, I need to acknowledge my bad forecast for headline real GDP — I had guessed at +0.25%q/q and the number ended up printing at +0.5%q/q.

Notwithstanding the strength in real growth, i still judge that the overall economy is weaker than the headline Real GDP number suggests.

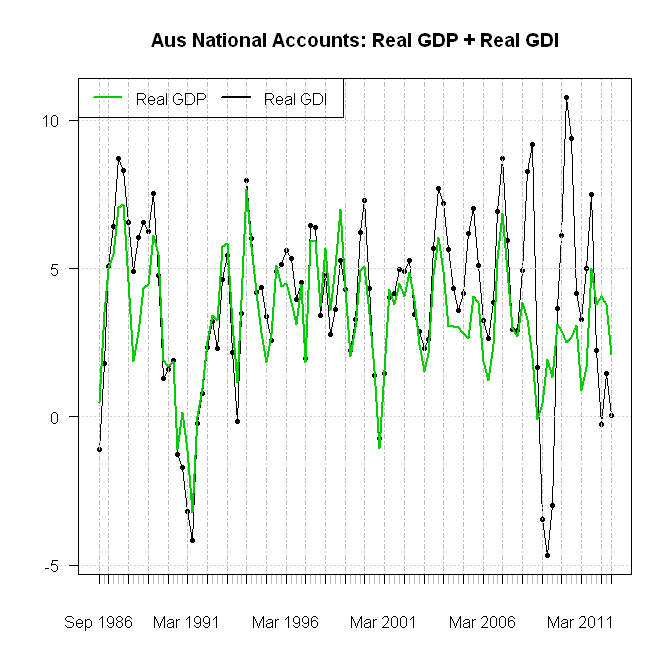

Having had a look at the GDP data, you can see where my judgement and the real data part.

Much monthly data seems to more closely track real GDI — this is a terms of trade adjusted measure of real incomes. This measure is weak, due to the falling terms of trade. The consequence of which is the real profits and real wages are falling (as they purchase less). In consequence, folks ought to spend less, and invest less.

I think that over the past decade this has been the better measure of what’s going on in Australia — it is more closely related to employment and inflation outcomes, and more closely related to real profits for the listed sector.

Real GDI was -0.4%q/q, and -0.1%y/y … that’s why firms are bleating like we are on the edge of recession. Above, i have shown the 2q MA AR, which i think best balances the need to smooth this data with the need for a timely measure of momentum. The 2q MA AR of Real GDP is +2.1%y/y, and the same measure for Real GDI is +0.05%y/y

A favourite measure of some, and a related measure, is nominal GDP. That grew at 0.16%q/q, taking the YoY pace down to 1.9%. The 2q MA AR pace is 2.3%. It only gets weaker in a recession. Looks like that surplus is going to be a LARGE deficit.

The other worrying factor (and reason i got my forecast wrong) is that the growth is ALL mining. We don’t have much monthly data on mining. According to the GVA Accounts, mining was +0.44% of the +0.47%q/q growth (it’s a bit of bogus point, but the statistical error was +0.1ppt, so if i hadn’t counted that, mining would have been everything).

So, while headline growth look okay(ish), nGDP (the thing the government taxes) looks weak, and inflation adjusted purchasing power is falling.

You cannot trust a single quarter of data, but it’s at least a little worrying that, outside of the mining sector, the economy appears to have stopped.

Looks like we need more cuts, and that we’re going to get a deficit. I’m taking a wild swing at -25bn.

I can’t help but feel that many listed companies wasted the boom by assuming the surge in the terms of trade would last forever. Check out performance of the resources sector….certainly doesn’t match what should’ve been delivered.

There’s little doubt Swanny is going to come up well short…at what point does he go from austerity to stimulus? What about if the Libs get into power…does that make you even more bearish given some of their rhetoric on the budget?

On an unrelated matter, do you know of a concise how-to guide to using R?

i will think on it and post something over the next few days. i have used a lot of different resources.

Another lovely post. Can I say that? Look, from an i/o perspective it’s still pretty intense. BK above say ‘doesn’t match what should have been delivered’.. How? Miners respond to demand. you can only sell to the market. So far,it has not retreated has much as bears would have, and as The Telegraph’s Ambrose Evans-Pritchard says we are “a country that lives off iron ore and coal sales to China”

as in, bring it on!!

i myself think that at least part of the weakness in overall productivity is due to the lags between investment and production in these massive mining projects. so i don’t think the mining sector has wasted the boom. the other sectors, including government (especially) have wasted the boom. the time for difficult reform is when capacity is stretched — but as always, it’s also when government is lax as revenue growth is strong.

From my perspective, and I agree a lag can arise, it is ‘still’ full-on. I guess miners have done what they do. And yes, these very good years have been if not wasted, expended – but I freely admit this an area of economic activity I possess no great knowledge. And yes, really problematic. Jeesh, as I’ve said elsewhere we need China! I can’t see an alternative. – if one exists – what is it?

ps – absolutely correct – the scale of these projects almost defies imagination!

2013, the year of the Aussie Dutch Disease.

OT, but now McKibbin is saying that we need fiscal stimulus. This comes after his call for the cash rate to be raised 75 bp. In between he argued for the RBA to sell dollars and just recently he reiterated his support for NGDP targeting. Apparently the rationale for his latest call is:

I think this is a very limited view of the monetary policy transmission mechanism. It’s pretty clear that if the RBA had cut by 100 bp, it would have got things moving very quickly and all this hand-wringing would have disappeared.

Then I heard Satyajit Das on Radio National last night, who said that lowering rates would do nothing because it would cut the spending power of lenders as much as it raised it for borrowers. My god, this man gets paid for this opinion. Why can’t they get Gittins, who is pretty sound and a good explainer when he’s actually talking about the economy.

Nominal GDP lower than real GDP because of deflation!!!

If that continues then no budget black line.

Oh how Wayne must yearn for Costello revenue figures.

Unit labour costs and productivity are heading in the right direction as well.

The public sector detracting 0.5 percentage points from GDP. We have austerity but those addicts do not want to recognise it.

I am thinking the only way the $A will fall is fr Europe to perk up. But since they are using Austerity but at the wrong time, As Keynes said, their debt and deficit ratios are rising.

what if Europe got better but China does as well so the $A stays where it is?

Lastly McKibbin is all over the place like Joye perhaps they share coffee

Lol, chris is going to really be annoyed by that comment!

No doubt he will be crowing about the latest jobs numbers. But how would they have looked if the cash rate was at least 1% higher, as he has been arguing for?

No surprise really. Unemployment is a lagging indicator.

This is all part of the disease … participation rate falling …. costs remaining high …. currency high … stubborn inflation … until ….

It is very well possible now, with the RBA out of the picture for 2 months, that the AUD will go even higher towards 1.06-1.07, especially during low volume holidays and especially in case of a fiscal cliff resolution (which I think it will be a last minute deal during low-volume holidays).

Yesterday Phil Lowe speech ( http://www.rba.gov.au/speeches/2012/sp-dg-051212.html ) contained a very good point I think:

” As I talked about in another speech recently, many of the countries that avoided the financial crisis are experiencing uncomfortably high exchange rates and low interest rates.[5] Australia is one of these. With the major economies of the world quite weak, most other countries would see themselves as benefiting from a lower exchange rate to boost their exports. But, of course, given that exchange rates are relative prices, not every country can simultaneously have a lower exchange rate. It should not really come as a surprise that countries that are in relatively good shape and have not seen large-scale expansion of the central bank balance sheet are experiencing stronger currencies than those that are in relatively poor shape. This is one of the mechanisms through which the weak conditions in most of the advanced economies are transmitted to the rest of the world. And in response to this, interest rates are lower than they otherwise would be to offset some of the effects of an uncomfortably high exchange rate.”

… The uncomfortably high exchange rate is one of the mechanisms through which the weak conditions in most of the advanced economies are transmitted to the rest of the world….

The uncomfortably high exchange rate is recurring more and more now in RBA communications. They know. They know. :)

CBA economic research make a valid point. if you examine personal income tax and payroll tax collections they are much stronger than the labour market shows.

Why?

My take:

– PAYG includes more than just salaries (includes all incomes) and you pay it based on your previous year declaration. At least I do.

– Payroll tax is calculated on the amount of wages you pay per month (and we all know these are going up, especially in mining, see: http://www.businessspectator.com.au/bs.nsf/Article/Chevron-lifts-Gorgon-cost-estimate-to-52bn-pd20121206-2PTZY ) From the CBA graph it looks like it is now just starting to come down. Excluding mining it must be coming down significantly already.

Bracket creep, tax changes? That series seem only weakly related to jobs growth.