The market traded like it was short following the better than expected jobs data.

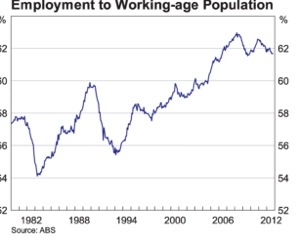

At least that is one view of things. The other is that despite a drop in the unemployment rate to 5.2% the report was weak. I am not so sure about that – while the employment to population ratio was constant at 61.7% for the fourth month, and the gain was all part time jobs, i do think that there is something in the unemployment rate.

Leaving participation rate stuff aside, there has been a sideways move in trend hours worked for some time, and if we cut the employment estimate and boosted the ranks of the unemployed by pushing average hours worked to 2007 levels, the unemployment rate can be pushed to ~7.5%.

This has been the case for some time, and until very recently the behaviour of wages suggests we should have worried about the low unemployment rate. Recently, wages have eased, and productivity has picked up, which should allow core inflation to track lower. it remains to be seen if wages remain low. I suspect they will, but it seems fairly uncertain.

Certainly, lower wages growth is required for the economy to regain competitiveness in the non-mining private sector. That is one way out if the currency does not fall.

I think the fiscal policy consequences of this development are clearer than the monetary policy implications. If the decline in participation and hours worked are due to supply side changes, then most of the budget deficit is structural. Deputy Gov Lowe pointed to the unusual increase in employment as a share of the working age population in his ‘normal’ speech this week – it may be that part of the new normal sees that track back down toward more ‘average’ levels.

If the terms of trade decline further, we are likely to find that the budget deficit very difficult to erase. This is not a massive economic problem, but it is likely to be a rather large political issue.

It may turn out that those surpluses were the fruits of a double boom – a demographic and mining boom. Now both ended.

Didn’t you say a month or two ago that the unemployment rate was the best measure?

Historically it has been the best predictor of future inflation. If there is something happening on the labour supply side, the unemployment rate tends to wash that out. The employment to population ratio misses that bit out.

All part time dude.

Yep, thought i’d saved that one in drafts … It was a little half baked! Fixed now. Thanks

not over the year and certainly not Males.

As I mentioned to you before the survey, I think something odd is happening with the job ads series. Right now, I do not believe the numbers. One candidate explanation is the fragmentation of digital advertising. It is also striking how after every circa 5.2% unemployment print there are a chorus of cries claiming the report is far weaker than it looks, and that the jobless rate is about to turn much higher. Finally, I note that the facts appear to have proven Glenn Stevens wrong within a few days: “Looking further ahead, with the labour market softening somewhat and ***unemployment edging higher***conditions are working to contain pressure on labour costs.”

Sure, that’s the big risk in this report — that the balance of supply and demand in the labour market is more inflationary than many judge to be the case, because the weakness we identify is due to changes on the supply side. Too soon to tell, but it is a rising risk.

a quick comment on the budget.

If tax revenues are very weak then ipso facto the improvement in the budget has come from spending and therefore a cut in the structural deficit. We can add the effect on GDP growth as supporting this.

this is obviously in contradiction to your theory which appears to be a cyclical effect has become a structural effect but has not had the expected effect on GDP growth.

This is what the blogosphere SHOULD be all about.

Keep it up!!

Thanks. I think i am am still formulating my new theory.

I had thought that the story for Australia was all about weak nominal gdp growth as the mining boom crests and falls away — but i am beginning to wonder if in addition to the end of the mining boom, we might not be also seeing the end of a demographic boom (at least in terms of the employment to population ratio).

Of course we had both lower rates of inflation and unemployment coexisting in the past, and it may be the case that they do so again in the future.

That may be the case. But there was an article on page 10 of the Fin today saying that the fall in participation and UnN was entirely due to a massive fall in participation amongst teenage girls. Schoolies week/month effects perhaps?

Looks to be true – part rate for women 15-19 was -1.8pts to 55.1%, none of this can be structural change — the unadjusted number was -2ppts, so it is not likely to be a lack of retail jobs over christmas, and the seasonal factors driving it down.

Anecdotal… just heard of a friend made redundant last week… she’s not going to go from employed to unemployed, but rather from employed to out of the workforce for a while… unless she can find a job very easily. This possibility was discussed here a few weeks ago.

Didn’t we have GDP running at 4% for most of this year and just recently slowing to 2%? Again, the unemployment numbers lag. Job advertising is more coincident and has turn south already for a quarter or so. Considering we will also see temp hires for the holidays, I think the next key UE numbers will be released in March/April.

you can see this type of thing in the gross flows data. exits to not in the labour force are unusually frequent just now.

Nominal GDP growth has been below trend for sometime now as has Real GDP being above trend.

The difference being disinflation.

This surely not continue

It could do, so long as the terms of trade keep falling. In that context, the trade deficit is worrying. If the AUD does not decline the work out is higher net exports, which will be difficult to achieve without a long period of very low wages growth.

This must be why sovereign wealth funds are buying up our bonds.

They are assuming a fair period of rather tepid growth with quite low inflation.

Thus a loosening in fiscal policy would deliver a lower $A and expansion on two fronts would it not?

Hmm, it might do. It depends on the relative fiscal position, i think. If we held relative fiscal constant and issued more bonds i suspect the currency would strengthen, as capital flowed in.

If were became weaker next to our peers, i think the AUD would have to weaken to attract the buyers.

Losing the AAA rating would definitely bring down the AUD. Otherwise a recession. If no recession, then it means the economy is adapting OK to high AUD, so a lower AUD is not warranted. Aussie economy still significantly better than most. And in a free market, a high exchange rate is one of the mechanisms through which the weak conditions in most of the advanced economies are transmitted to the rest of the world.

PS for me the most likely path in the next couple of years is a marginally lower AUD, to around parity with USD, but not much lower than that. Only in the event of a recession we may see 0.90 again. On the other side, I do not think our economy can deal with a much higher AUD from here, unless China takes off again.

What if the US went to AA-flat? Then AA+ Aussie bonds would be pretty attractive. You have to keep relativities in mind when thinking about capital flows.

Yes, but being one of the few left AAA (the best of the best) does include a premium.

Holding relative fiscal constant is surely not the same as loosening fiscal policy.

However once the expansion is sound then you would get the same problem again as fiscal policy is tightened given the European situation.

Where in the world can you get a triple-A 10 year bond at 3% , with bond prices forecasted to go higher and the currency to stay strong? Markets are trusting the RBA cutting rates will be enough to sustain the economy.

Who has the solution to lower bond prices which lowers the $A, boost nominal GDP and therefore also the budget bottom line?

We have inadvertently picked up the European disease of stronger fiscal policy ( and $A) leading to weaker growth!!

“European disease of stronger fiscal policy ( and $A) leading to weaker growth!!”

So, you really think the solution for Europe is more wasted govt spending?

Re Australia. People have decided to start saving after having accumulated debt for years. Why would the govt go against that decision? Can’t we afford to save money, not even during the biggest mining boom ever. Then when?

Lars Christensen has a good post about how countries like Australia can avoid problems arising from the zero lower bound – follow Bennett McCallum’s rule of committing to operate monetary policy through an exchange rate target (like Singapore) if the cash rate falls below 1%. The right time to banish any “out of ammo” talk is now, while the cash rate is still at 3% and before it looks like panic.

IMO economists that propose NGDP targeting in monetary policy do not understand that the inflation target is a *very important* contract between the government (who controls the currency) and the people. And that goes far beyond “economic growth”. Take that away, and money becomes worthless paper (some people already think that, because they do not trust govt to keep its promise) and monetary policy useless.

Do you think? Why are people so miserable then with inflation at 2%, RGDP at 3% and UnN at 5.2%? Sumner’s favourite response to your point is that CPI-measured ‘inflation’ often doesn’t mean very much to people. He frequently highlights that the housing component of CPI in the US rose 7.7% over the 5 years 2006-2011 whereas Case-Schiller has them down 32% over the same period.

You are miserable with inflation at 2%, RGDP at 3% and UnN at 5.2% only if you are drawing in debt that must be repaid, and asset prices are no longer growing like they used to. High asset inflation is your drug. Ask the Swiss if they are miserable. I do not think so.

” CPI-measured ‘inflation’ often doesn’t mean very much to people ” Often? Very much? Sorry, but pretty vague. When real asset prices go out of control, that’s exactly when people think money is worthless and keep buying more and more. Central banks were wrong in not considering also asset prices key to monetary policy and limiting themselves to “official” CPI

I agree with this. I think nGDP targets could prove costly – however i do think nGDP is a useful variable in thinking about the likely evolution of the economy, especially w.r.t inflation and unemployment.

Interesting set of papers from the RBA just released on the topic of property markets. Stevens’ intro provides some support to ‘leaning against the wind’ whereas the Ellis paper seems more circumspect.

I really appreciate Stevens fatalism and modesty. We are doing as best as we can in an imperfect (and unknown) world he seems to be saying. Which is exactly right.

I like it most because it exposes the overconfidence of many ‘experts’ as nothing but bluster.

I think the RBA is already thinking along these lines. At least that was the impression i obtained from Lowe at last week’s ABE function.

We should finally put to bed the argument that cutting rates lowers the AUD. There’s just too much rate differential, for the time being.

AUD is now just a function of commodity prices (iron ore).

There’s the argument that govt should borrow cheap money and invest in infrastructure. Just would like to remind that even if rates are low, the principal still needs to be repaid. So govt better make a return out of that investment. Rates were low in Southern European countries too when spending went up in the last 20 years. But the majority of the deficit was pretty much wasted money. And it simply delayed the reality of China’s uprising and low competitiveness.

There is a subtle question here about the appropriate IRR to assume when assessing public works, that i think is missed. If we assume that the economy balances out in some reasonable term, the IRR should be an appropriate risk weighted rate, but if we think there are material frictions a lower rate is appropriate. I am ambivalent — as expected :)

In normal times I agree with you on infrastructure spending but faced with an emergency and with no plans ( disgracefully on the table) the government had to do something.

As it was the stimulus was highly successful and when examined correctly with surprisingly little waste.

That is not to say there were no problems,

http://www.smh.com.au/nsw/awful-waste-school-building-audit-finds-664m-reduction-in-value-20121211-2b7c3.html

That’s what happens when people are not spending their own money … (it was actually our money, the tax payers)… efficiency is gone, things are done “more or less”, “about right”. And that’s what has happened for 20 years in those Southern Europe countries that are now struggling repaying their debts. But still there are some people in those countries calling for larger government and more public spending! Wanna end up like the USSR? Now is the right time for Australia to be virtuous, when it looks like you do not need to. Will benefit us later on.

It’s an interesting post hoc valuation. I wonder if they’ll repeat the exercise for all infrastructure? Valuing public assets with no market value is a highly theoretical task.

I do not think it’s a market valuation. They valued the cost to replace now what was built under the federal government’s Building the Education Revolution program and found it all could be built now for about 30% cheaper.

What do you think about this ?

RBA told intervention necessary to dampen $A

http://www.businessspectator.com.au/bs.nsf/Article/RBA-told-intervention-necessary-to-dampen-A-pd20121212-2WQ48

“The Reserve Bank of Australia (RBA) is being told by central bankers elsewhere that if the RBA truly wants to dampen the value of the Australian dollar then it should consider heavy intervention measures…..”

I think it would be a better plan instead of further budget spending or ZIRP. *IF* the problem is the high AUD, then let’s go to the root of the matter.

I think if you read the BER task force’s final report then I am sure you wil change you mind.

I always rely on primary source ans secondary sources sometimes get it wrong, badly wrong!

Who do you trust, who do you trust? It does not matter, as there’s no accountability and it’s not their money. Tax money keeps coming in, it is not earned. Definitely I do not trust govt reviewing their own spending. An independent investigation would be better (but can you have something “independent”?)

No you only trust something that backs up your prejudices.

Unless you can show how the BER taskforce ‘doctored’ the figures or miscalculated you are simply wrong with a capital W

The NSW Auditor-General found the NSW Department of Education’s revaluation figures showed the replacement cost of some buildings after revaluation was up to 84 per cent lower than actual costs for the BER buildings.

Auditor-General Peter Achterstraat said the significant decrease in replacement cost in the department’s revaluation of BER buildings – from $1.89 billion originally to $1.23 billion now – may be due to the actual costs paid for them being too high.

You are not trusting the NSW Auditor-General but trust DEEWR? OK

He who trusts not is not deceived.

If you look at the BER report (on page 24 on) you’ll see criticism of the NSW Department of Education. He who trusts not is not actually reading anything.

On page 26, it reports that 40 out of 137 projects checked were a fail, with a further 31 passing the test only partially. Focusing on the 40 out of 135, that 30% wasted money.

If you then go to Appendix 8 (starting on page 154), you’ll see how many of the projects failed on cost. Far too many 0 out of 10 IMO.

By the way, I am not arguing against public spending in general, it’s great to have new school for kids, etc. But it’s better not to rush into major, rush-through infrastructure projects with the goal of supporting the economy in the short term. We better take the time needed and do these project as best as we can, on a merit basis, following the proper processes.

Like the Anzac bridge? A wonderful piece of infrastructure built years after the recession ended. How useful. If you accept stimulus is needed to avert a crisis, surely it has to be timely?

Any thoughts on the BER in other states, or even in NSW private scoold where there seems to be a lot less criticism.

I do not know about other states… surely there was a review done for other states?

Were there 30 project managers failed / demoted for the schools that failed the projects?

“If you accept stimulus is needed to avert a crisis, surely it has to be timely?” What about just cutting taxes to stimulate then. Rushing infrastructure projects comes with too much waste.

Weren’t tax cuts already coming from the permanent Howard tax cuts that rudd promised to also deliver? If tax cuts worked there wouldn’t have been a recession. Oh and the 900 cash handout.

It also bought lots of plasma screens and increased savings. Is that really better than new school halls and decreased energy usage?

Nanny State? We should have a 80% tax rate and let the govt decide how it’s best to spend your money.

Isn’t this where we give some space to public service maxim that you ought never have an enquiry if you do not know the answer?

yes but there were good reasons for that in NSW if you read it through.

more smaller classrooms which cost more and no project management in NSW so it had to be outsourced.

DEWWR had nothing to do with it.

The only reason I see for the waste is that these projects had to be done in a rush or schools lost their funding. That allowed some contractors to over-quote and under-deliver. Do you know of a post-mortem analysis done for other states too? Surely there must be one done. Hopefully was only a NSW issue.

Your’re determined not to read the BER report aren’t you?

I think that is why private schools got better value for money. That and they also (typically) did a parent capital raising, so they were spending ‘their own’ money, which means folks tend to seek better value.

I did… I must be tired… probably missed a key point. Can you point it out to me. thanks

Lol

of course it had to be done in a hurry. there was a GFC at our door and there were NO I repeat NO infrastructure projects ready to go. (Think about a dual carriage way from Melbourne to Brisbane for example. why wasn’t this ready?)

Something had to be thought up and done in very quick time.

Given that I am astounded we didn’t see a lot more problems.

That is why we didn’t have a recession.

If we didn’t have a stimulus then we would have ended up like NZ or Canada in being too slow and to little or like Estonia and make a depression out of a recession.

now that is waste.

The infrastructure components of the stimulus are a sad joke. Leaving aside the massive over-payments and the inappropriate types of buildings, even the timing was too late. The government’s own documents show that only $3bn (out of $27bn) had been paid by June 2009 and only $12bn (out of $30bn) had been paid by the end of 2009. Interest rates started rising in October 2009, so it cannot reasonably be said that fiscal stimulus was needed beyond that point, yet more than 60% was yet to be paid, driving up interest rates unnecessarily and crowding out productive private investment. Just because the RBA is too stubborn to loosen monetary policy enough now does not mean that more wasteful government spending is the answer.

$664 million wasted only in NSW….. Minister for Education Adrian Piccoli said $664 million could buy 20 new primary schools and 9 new high schools. But who cares? It’s just tax payers money, Every time there’s a risk of recession in Australia, let’s just waste some more tax payers money and we will never have a recession – guaranteed! Builders were happy – I am sure. We will be wealthy forever! Because it is know fact that waste = wealth. We can always print more money. A LOT OF IT!

Rajat I am afraid you show a lack of understanding of basic fiscal policy.

One has to be very wary of consolidating too quickly because you can go the Japan way.

So you reckon house prices are down about 5 to 10% from peak? You really can’t invest in ALL residential Australian houses…. but here is a two real life examples in SA. This is a new build 2009:

67/155 Brebner Drive, WEST LAKES SA 5021

It was paid $3,250,000 on 05/08/2009

Just sold last month for $2,300,000

The penthouse next to it, it is 63/155 Brebner Drive West Lakes SA 5021

It was paid $2,800,000 on 05/08/2009

Listed for sale now at $1,750,000

http://www.realestate.com.au/property-apartment-sa-west+lakes-112204011

The vast majority of new houses bought after the GFC would be now selling at a significant loss if on the market. That is why new home sales are now at very low levels. We have allowed domestic non-tradabale inflation to be too high, and especially in construction, and we think now new residential construction should replace mining???? New houses are completely unaffordable and at current prices are a certain loss/ That’s what happens with unneeded stimulus plans. But you all know, just try to get quotes from trades nowadays.

Ouch.

The studies i have read are US, but they come to the same conclusion — when prices are down, folks sit on their homes rather than sell them. And why not, mortgages are never margined.

I have a friend who said a friend made a killing on a house nearby, so that clearly shows property isn’t that weak. Or at least not as weak as citing two house sales as proof of an argument, which fails to explain a rise in sydney values

Friends always make a killing :)

Was that “killing” on new residential built after 2007? Address?

Regarding house price indexes consider that:

1) The ABS only includes established houses (not sure about RP DATA). No new residential apartments.

2) The indexes miss all the small renovations and capital injections such as a renovated bathroom, kitchen, landscaping, roofing, ducted airco etc. I’d say that accounts for 2% p.a.

3) The indexes only include houses actually sold. Not houses sitting on the market unsold for years or withdrawn. So it is a natural tendency of the index to be positive.

4) Sydney is by far the healthier market, not having moved as much since 2003 (compared to the other capitals). Amount of house transactions in Sydney are also very healthy.

ssec, you’ve mentioned this idea a few times about construction inflation. I don’t think that’s how things work. The way I see it is that it currently costs a certain amount to build a house (say $X) and a certain amount to buy an established house (say, $Y). Obviously, Y needs to be > X to stimulate housing investment, which I think needs to happen. Your objection seems to be that X is already too high and so monetary stimulus will simply make X higher and houses more unaffordable. But there are two things going on here – the level of house prices and people’s expectations of their future nominal income growth. I don’t want to pay X now if I expect my income will be flat or at most rising with inflation over the next 10 years. But I don’t mind paying X+10% (say) if I know my income will be rising by 5% pa over the next 10 years. The problem we have at the moment is that people have made decisions over the last 5-10 years based on the expectation that their nominal incomes will rise at 5-7% pa whereas now they are rising at 3-4%. If the RBA avoids recession, we will eventually reach a new equilibrium with lower interest rates accommodating lower wage growth expectations and broadly stable asset prices. That hasn’t quite happened yet. The alternative (which I advocate) is to move part-way back to the higher nominal growth path we used to have. This will help keep up from the lower bound and minimise adjustment costs to the post-mining investment world.

When I see a brand new house sold for $3,250,000 in 2009 and then resold for $2,300,000 in 2012 (by the way – the whole apartment block is down about 30%-40% according to recent sales, also the 1 and 2 bedrooms apt and so are most new apartments in SA built after 2007) I wonder: What’s the cost to build that apt now again. If it’s closer $3,250,000 than to $2,300,000 than it’s a problem. It means now there’s NO demand for new apartments at today’s cost. If the price paid was a stupid price and $2,300,000 is still above what is cost to build that apartment, then it’s still a good business case for the builders.

However new house sales have been extremely weak this whole year.

Regarding your example, what happens if it costs $X to build an apartment , and that is simply too much for the level of demand that is out there? Yes, you can try to stimulate demand, by lowering the cost of credit, but what if instead is the building cost that should come down to match demand? In your posts you never seem concerned about what inflation can do to an economy.

He’s Sumnerian – they are much more concerned to validate expectations and therefore to stabilise demand. I worry that this would encourage extremely high leverage, and when big leverage busts, i fear that monetary policy goes from weak to ineffective. The US isn’t out of the woods yet – it could still turn Japanese, despite Bernanke’s best (and better) efforts.

My point is that monetary policy will never succeed in getting “the building cost down to meet demand”. That would require extremely tight policy, which will hit housing demand far more than it will reduce building costs, not to mention cause a lot of other pain on the way. The argument for NGDP targeting is that nominal wages are sticky and fall only reluctantly under the worst conditions. As for inflation, it seems far from a problem at the moment. As I said, I don’t support going all the back to 2007-08 levels of NGDP (8-9%) and inflation (5%), but perhaps half-way (NGDP growth at 5-6%, average inflation at about 3%).

Good micro policy might succeed. But they don’t want to be too successful in the short term, as that will push prices down even further.

My point is that you can’t just focus inflation for a quarter, or a year, and say we are OK. Building costs are where they are today as the result of a decade of monetary policy and a decade of cost rises. And if too much demand was allowed to be carried forward then, and now that demand suddenly dries out, then you find out what inflation really means. You say yourself we had NGDP (8-9%) and inflation (5%), and that was a big miss in 2007-08. So now we may have a product (new residential) that became too expensive to build, at the exact time when demand for the product is slow. Shouldn’t building costs actually come down instead of going up when demand was high (new building technology, new efficiencies, etc).

Maybe the housing sector needs a productivity dividend? Surely the BER and the First Home Buyers subsidy saved anyone worrying about better tech, processes etc. and just let things rip.

as you know i like the idea that monetary policy mostly just changes the timing of housing investment. I tend to agree, real construction costs are going to have to fall — but part of the reason we had such a boom in the capital prices of existing homes is that it is difficult and costly to build new homes in Australia. The great genius of the US is that the took the world’s cheap capital and invested it in homes that will last for 60yrs.

so when the hangover clears — even I don’t think the hangover is going to last longer than the homes – they are going to have cheap and plentiful homes. I think that’s a benefit to all sorts of risk taking / entrepreneurialism.

ssec, if you are suggesting that monetary policy was too loose for a decade, you must be also be saying that you would have preferred lower growth. I am not convinced that would have been preferable. Going back to the point of all this, the RBA is concerned that growth will be weak (and UnN will rise) in 2013-14 if we don’t have another source of demand to pick up from mining investment. It’s not the job of stabilisation policy to pick winners; I just don’t see many options for where that growth could come from – there’s government spending, exports, consumption/retail and housing investment. The first one is off-limits (so we are told), the second is hampered by the strong dollar and the third and fourth will require lower interest rates and/or higher house prices. So the way I see it, we either have higher house prices or we have a recession and I see no good reason for the latter. I also don’t share the bring-forward concern because housing starts have been very low over the last couple of years and are now at GFC levels.

Rajat, I prefer balanced, stable growth. No consumerism, no waste. No spending just because tomorrow it’s going to be more expensive. I prefer stable inflation at 2%, like most developed economies and asset prices / salaries growing at around the inflation rate. I also would prefer people not drowning in a ocean of debt, just because otherwise I can’t afford a place to live in tomorrow and taking on too much risk (the whole economy is taking a risk with them).

“I also don’t share the bring-forward concern because housing starts have been very low over the last couple of years and are now at GFC levels.” You keep referring to the last coupe of years, but I refer to the last decade which is a time frame that is more appropriate for something like housing.

Can we have trend growth and flat house prices?

Even the last decade has not seen atypical growth in the number of dwelling units. The monthly average of private housing starts over the 10 years to June 2012 was 25.6k. It was 25.5k in the 10 years to June 2002 and 24.4k in the 10 years to June 1992. This is despite faster population growth (in numbers) over the last decade. The equivalent figures for the ‘other residential’ series are 11.8k (2012), 10.1k (2002) and 6.5k (1992). Does that suggest to you we have built too many houses over the last decade?

The trick is figuring out why house prices went up instead of home building when we lowered the cost of housing capital. It is a hard trick.

I agree, we could usefully build a few – and perhaps the period of high rates meant we built too few. But i am not sure about that, and i stand by the view that rates mostly change the timing of durables consumption. Just like first home buyers boosts change the timing of first home entry, but not the homeownership rates, and cash for clunkers policies change short term sales but not vehicle ownership rates.

Still, it is the only way to avoid recession, so we might as well give it a try. I favour LVR caps to deal with the froth.

I think it’s clear that the supply side of the housing market is fairly inelastic. Difficulty and cost of sub-divisions, council regulations and comparatively high wages for unskilled labour. The RBA has to take all that as given. The recent RBA Ellis conference paper said some interesting things about this. She makes similar points about LVRs but ends by saying, “the level or change in aggregate indices of asset prices are not good guides to predicting the extent of financial distress during the bust, and neither is the amplitude of the cycle in credit.”

We will not find out if we have built too much until we find out.

To be honest, I do not know if we built too much or not. That depends on an extensive set of variables. What I know is that prices have gone up significantly, building costs too, new houses and apartments are very expensive, and new house sales are extremely low now, what’s on the market is not selling, for whatever reason, even with 3 year fixed rates at record low.

It could be we are all waiting for the cutting cycle to be finished, for the US economy to recover, that I do not know. But I think the most likely reason is that the credit boom we had in the last decade was that: a boom that can’t be repeated. Will the economy, including housing, be able to adapt to the new regime of low inflation and lower rates? There’s lots of debt out there that must be repaid, low inflation certainly makes that a lot more difficult. So, are we addicted to 3% inflation and 4% salary increases or will we be able to have growth with 2% inflation and 3% salary increases, without the whole thing to collapse?

hang on the deflator used in construction activity doesn’t back up your assertion.

moreover if the stimulus simply was too large the output gap would have disappeared quick smart and cash rates would have risen sharply and a lot quicker than October 2009.

I was referring to a long term view, e.g. since 2005, including the period of high inflation that escaped the RBA in 2007 for which we are paying now.

Gentlemen,

I believe we owe RA to the extent we should make this his thread of doom.

come on we can do it!!

Well, if he doesn’t post again on economics for a while, it will be without much trying!

Okay, i will post something on economics soon :)

Merry Christmas Gentlemen!

You know i love the comments section :)

We need a target. Let us get 100 comments

:)

What an arbitrary target to maximise our utility with. Is this rational behaviour?

Who cares about “Rational Behaviour” ! :) Think with your HEART…..FEEL….

You think it’s rationality that lead Einstein to formulate the relativity theory? No! He actually FELT it. He WAS the theory. :)

I have no idea what this means – what do you think we ought to aim at? Maximising utility is good, sure, but what is it?

On the way to 100…. :) From the minutes, it looks like the main reason behind the RBA cut in Dec was the lack of a Jan meeting. If I am not mistaken, after the cut we got weak GDP but the employment numbers were OK. Inflation expectations are at around historic lows however. Iron ore is recovering. I reckon no cut in Feb pending further data, especially if US cliff OK. They will then cut again in March.

yep; looks like it was a close call. I think that a 0.5%q/q core number or lower would do the trick. That drop in inflation expectations is pretty interesting. Seems that punters are not seeing price rises in their day to day (which mostly means food and fuel) — it is a decent general guide to inflation pressures, and it suggests that there’s not much about. Perhaps the ability to blame it on carbon pulled forward price hikes into Q3?

I think the drop in inflation expectations is also caused by the RBA cuts and house prices stable. It’s probably a reaction to that.

No chance. Folks don’t care about the bank or know – not like us junkies do.

touche! :)

It seems ‘liberal voters’ have gone pessimistic again.

Will consumers or businesses respond to lower interest rates. Hmm

Not far from 100!!!

I blame Turnbull

100!!!

well done gents! Almost all were legitimate too

One reason I like this blog is because both the author and commenters make you think.

It is all very well to disagree with a point of view but you need firm foundations and I believe the commentary here does just that.

It is a credit to both RA and the commenters here.

Well done

I agree!