On Friday night, the Australian Government published the budget results for November and December (for some reason we cannot get regular publications of the data, like most first world countries).

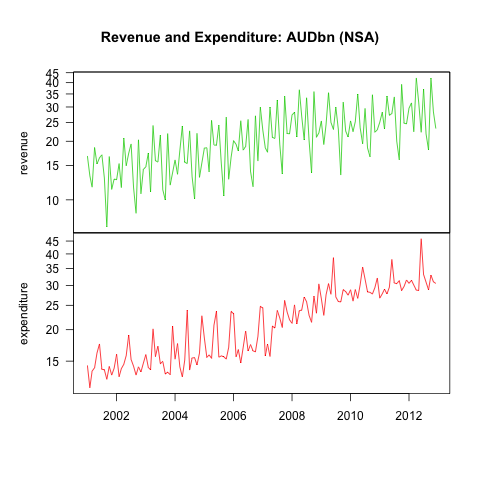

As you can see above, there is a lot of seasonality in the data. I think the most interesting thing in the data is the silly ‘bring forward’ of expenditure into June 2012, to try and depress spending in the 2012/13 fiscal year, and therefore pretty up the 2012/13 budget.

This sort of behaviour is addictive — you have to do more of it each year to bring down the next year. Thus, though they may try the same trick to help 2013/14, by bringing spending into Q2’13, it’ll have to be even more extreme — and eventually they will run into a limit of what spending can be sensibly pulled out of the following year.

While it’s not that meaningful to report that revenue for the two months was 51.515bn, and that expenditure for the two months was 61.552bn, i do think there is enough information to conclude that they are headed for a rather large miss on the 2012/13 budget outcome.

The question is how large?

The monthly budget returns say that they are currently 3.877bn behind the MYEFO targets, due to a 5.172bn shortfall of revenues, which is partly made up for by expenses being 1.54bn below forecast. If we assume that the next six months will be like the prior six months (relative to forecast) we get to a 7.745bn deficit.

I think the deficit is likely to be much larger than this. Why? Well if the 6m we don’t know are like the 6m we do know (meaning H1’13 is like H1’12), then the deficit will be a whopping 32.4bn.

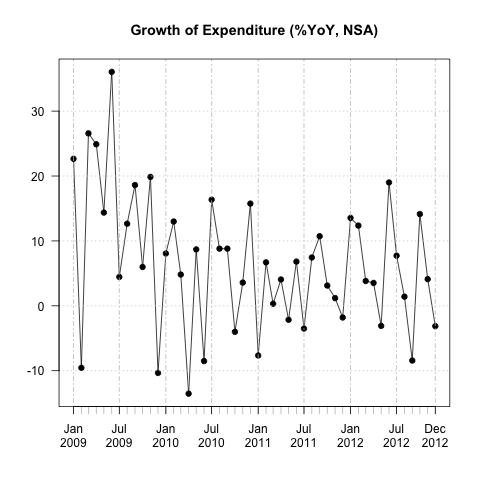

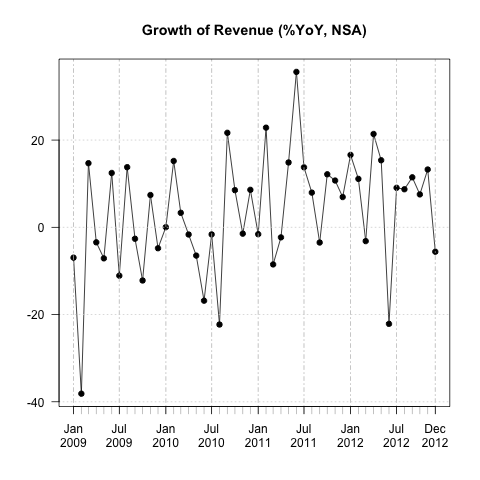

As you can see from the above chart, a 22bn improvement in six months would be unprecedented (the largest ever was 16.5bn in 2007 when the mining boom was pouring in company tax receipts) so a single digit deficit seems unlikely. Assuming that they hit their expenditure target and that revenue growth holds pace, the budget outcome will be a deficit of ~10.5bn.

These seem to me to be best case — the deficit could be much larger.

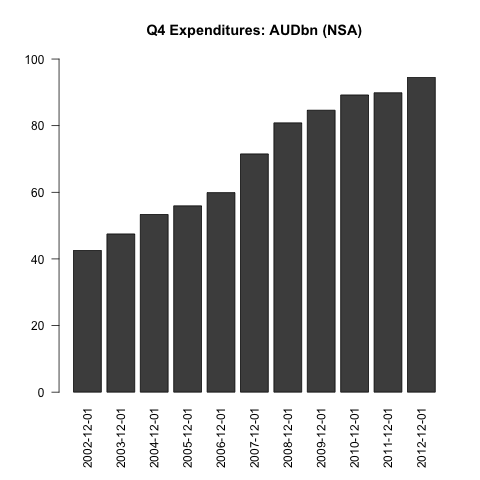

The above chart shows expenditure only in fourth quarters of each year — you can see the spending continues to grow firmly, after flat-lining in Q4 for the past two years. This looks like an end to belt tightening – not the start of it.

Expenditure growth in Q4 (Q4’12 on Q4’11) was 5% YoY — at ~94.5bn, Q4’12 expenditures were 4.6bn larger than Q4’2011. This follows expenditure growth of 0.4% in Q3 (partly depressed by the pull forward into Q2’12). I find it hard to believe that this is a setup for an expenditure reduction across the entire year. It looks more like that they realised they weren’t going to make surplus for FY12-13 some time during Q4’12 and re-opened the purse.

Sure, the spending profile was as budgeted in the MYEFO, but they would have known enough to tweak the scheduling by that time. In any case, their track record suggests that spending is going to be larger than budgeted (and all the risk is that it balloons as they bring 2013-14 spending into 2012-13, so that they potentially forecast surplus in 2013-14 ahead of the 2013 election).

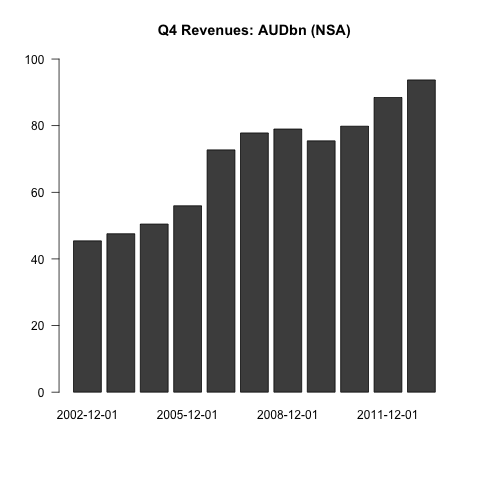

The above chart shows the level of revenue only in fourth quarters. As you can see, revenue growth has been pretty good since 2009. The current problems on the revenue side are more due to the unrealistic 2012-13 budget revenue forecasts than weakness. Growth has been pretty good for the most part, though there was worrying weakness in December.

Despite a cracking start to 2012-13 (+9.5%yoy growth in Q3’12), and a pretty solid Q4’12 (+5.7%yoy) they are already 5.2bn behind budget — how is this? The assumptions were always unrealistic.

So what are realistic assumptions?

I think it’s realistic to assume the revenue growth in H1’13 is around the pace of H2’12 (so i applied the H2’12 yoy pace of growth to the level of spending in H1’12 to estimate H1’13 — this should deal with problems of seasonality). This process suggests a miss of ~9bn on the revenue side.

On the expenditure side, let’s assume that they are able to get H1’13 spending 1% lower than H1’12 (this should be possible as the bring-forwards into Q2’12 probably won’t be repeated in Q2’13, which will depress the YoY pace). On that basis expenditure is ~5.7bn larger than expected.

This yields a fiscal deficit of ~16bn for 2012-13. I would say that the risks are to the downside of this number, as i am both pessimistic about expenditure control and suspect that we may (again) see spending moved into Q2’13 — so they can forecast a surplus in 2013-14.

OT, but I found this video amusing (warning: foul language).

Be interesting to see if the ECRI will be able to come back from this. I think everyone used to watch their gauges pretty closely, but they seem to have drifted from consciousness as their analysis diverged further and further from consensus.

I found it surprising that they held the call after the resi sector started growing as a share of GDP.

You find out that you have a divide-by-zero bug in your formula only when variables actually get to zero. The GFC was no normal economic cycle… I think ECRI were mainly wrong because they forecasted a new recession when the US had not had any recovery yet.

:) :) :) !

Yep, should be good for your short AUD position.

The original movie “Downfall”

http://www.imdb.com/title/tt0363163/

is a must see and Bruno Ganz exceptional.

There was a great rudd / downfall youtube prior to the coup / last election. Haven’t seen the original.

Highly recommended. Actually this just reminded I must watch it again!

Yes, I agree it was a great movie. Harrowing, but completely engrossing.

Tax is highly seasonal which I think you did not really emphasise.

Stronger commodity prices would halp there if it occurs and is sustained.

I tried to emphasise that both sides are highly seasonal – but it seems unlikely that we will see all that much boost from iron ore. Perhaps in Q2, but not earlier.

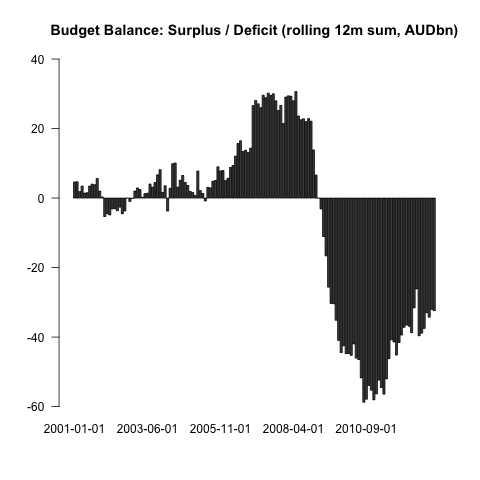

I should have added if conditions do not change then a deficit of $16b instead of a balanced budget is far more appropriate outcome

Yep, i support letting the stabilisers work as well – though i do generally think a little more tightening will be required at some point, as the deficit is starting to look a little more structural than i had first thought. The RBA ought to offset this with cuts.