The Department of Finance has released two fresh months (Jan and Feb) of data since I last posted on the Commonwealth Budget.

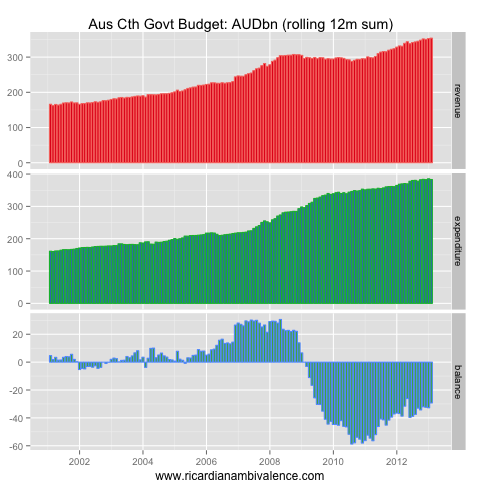

Broadly speaking, Jan and Feb show ongoing — but slow — progress towards fiscal repair. It still remains the case that they are falling behind on revenue — revenue to Feb is ~7bn behind the MYEFO forecast. They are running close to target on expenses, so this means that they are ~7bn behind on their MYEFO forecast of a 1.2bn surplus.

I never thought their revenue projections were reasonable, so I’m not surprised to see this. I expect that they’ll fall further behind on revenue over the next few months. If we assume the current rate of softening, you’d think that they’ll be ~11bn behind on revenue for 2012-13, however I suspect that’s going to prove optimistic.

The rolling 12m sums are a guide to how things develop ‘on average’ (the implicit assumption is that the months to come will be like last year). On this basis, revenue is ~354bn, and expenses ~383bn for a 12m deficit of ~29bn.

So why do I think it’ll be a 20bn deficit and not a 30bn deficit? Because i doubt we’ll see the usual end of fiscal year money-shuffling. In prior years, expenditure has jumped in June as payments were pulled forward into the current year — to try to make the following year look better. Not doing so will cut spending in 2012-13 relative to 2011-12.

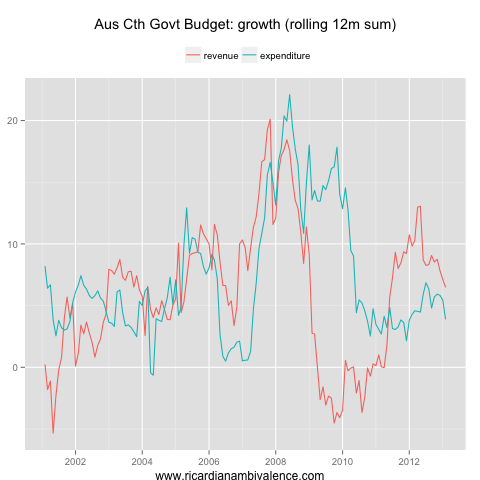

The growth rates show the current economic slow down very clearly — revenue growth has been slowing since Q1’12, and continues to slow. The revenue line is falling more quickly than the expenditure line, meaning that the monthly improvement in the budget deficit is slowing.

The lack of year-end ‘shuffling’ will lower spending growth further, however the fact that the ALP hasn’t yet passed some of the savings measures in MYEFO calls into question the probability of a reduction in spending in 2012-13 (relative to 2011-12).

On balance, it seems things are a little worse — and that has me edging out my deficit projection ~4bn to ~20bn.

I’m really interested in what Treasury projects for the carbon price in 2015/16, given that the European price is tracking at < $A4/tCO2-e. The original Treasury projection was that the price would rise above and beyond the indexed Australian fixed price, which will be about $A29 by then. Lower price means a big Budget hole down the track.

Yeah, things are looking fiscally fairly bleak. The conservatives are going to have to cut hard in their first budget if they are to get the structural balance back to surplus. At least 1ppt of GDP. That’s another reason to think the RBA will need to start cutting once again.

No way they’ll cut while the mining boom fades…. forget the surplus, it won’t happen for a few years, no matter who is in govt.

The structural position, if commodity prices return to their long run averages, is dire. If the mining boom ends, there is going to be massive pressure to cut spending.

I agree. Abbott, Hockey and Robb are all talking a big game regarding slashing wasteful government expenditure. Sure there’s waste to be cut, but I’ll be very surprised indeed if the Coalition has the courage to follow through with it. Abbott’s too timid to support sensible means tests of middle class welfare payments like the baby bonus, private health insurance rebates and super contributions. Even the Coalition’s talk of cutting 12,000 federal public servants is to be done through natural attrition over who knows what timeframe. Abolishing the carbon tax and mining tax are offset by the resultant spending and compensation that he’s vowed to keep. Campbell Newman in Qld gave it a good go when he came in as premier. John Howard took the knife to spending when he came in. But these guys were convervative ideologues. Abbott is bereft of any real ideology that I can see. He’s a big government populist. Perhaps he’ll develop a ticker when he’s in government, but at the moment, I can’t see him having the courage to make any meaningful net expenditure reductions at all. Rudd talked about the razor gang when he first got into office, but could only deliver some very modest savings once the realised the GFC was coming. Abbott & co will be no different. Don’t expect much in the way of cuts.

Here you go:

Abbott kills off surplus promise

http://www.afr.com/p/national/abbott_kills_off_surplus_promise_HUvzXUwV8vw8iIJjaUcHnK

oh dear there are problems with the comments.

You only cut structurally when the economy is strong and can take it. As Keynes pointed out correctly and presciently in 1936 austerity only works on good times.

you people are advocating policies that put Europe in a recession.

The budget bottom line is only a means to an end not an end in itself.

if the revenue from the ETS falls because the price falls then compensation will commensurately fall as well.

I am not advocating it as optimal policy, just pointing out that i think it will occur. Australian politics has been anti deficit since Keating.

Carbon tax compo to industry might fall, but not to households. Fiscal policy should have no effect on output if the central bank targets inflation or nominal GDP and does so assiduously. Even Krugman recognises this; unfortunately, most policy-makers and commentators don’t.

C’mon, the issue is that it is hard to get either monetary or fiscal policy right in the short run — as forecasting is so hard. Go to a long enough run and monetary policy has no impact on anything at all, regardless.

True, it’s hard to get stabilisation policy right. But the issue is not so much getting it right but whether the central bank will take account of fiscal policy in setting monetary policy. My point is that if they’re targeting inflation or NGDP, they have to take it into account. The central bank might under- or over-estimate the role of fiscal policy, but there is no reason they should systematically understate the impact of fiscal policy, such that fiscal policy has real effects in the short term.

What will happen is that private debt will be transferred to public debt in the next few years as the private sector will continue deleveraging. Maybe that will bring Australia to lose their triple A rating and finally the AUD will come down to more optimal levels.

Is household debt a worry for Australia?

http://www.smartcompany.com.au/finance/052845-is-household-debt-a-worry-for-australia/2.html

Spot on IMO

Depends who you ask. It will be if unemployment spikes, but i am not so convinced it is a trouble just now.

Here is a good summary table of public and private debt; Australia not much lower than Italy and the USA.

http://www.switzer.com.au/the-experts/shane-oliver/debt—how-does-australia-compare/

But apparently rating agency only care about the public part, as if private debt would not need public support in a recession (see Ireland).

That’s false. SnP and Moody’s both explicitly count state, local and bank debt when rating. Indeed, the reason Australia is most likely to go on a negative outlook would be bank funding (which means almost the same thing as the CAD).

Debt per se isn’t a problem, what is a problem is when expected returns on borrowed money fall short of anticipated returns — that’s when the fixed repayment hurts you.

OK, they consider all debt. So Netherlands AAA?

“It is a problem is when *expected* returns on borrowed money fall short of anticipated returns. OK.” Ireland was rated triple AAA until 2009. Public debt/gdp was below 38%. Then housing and the economy popped. So what’s the value of “rating” really?

Sure, they aren’t worth much — but the buy side likes them …