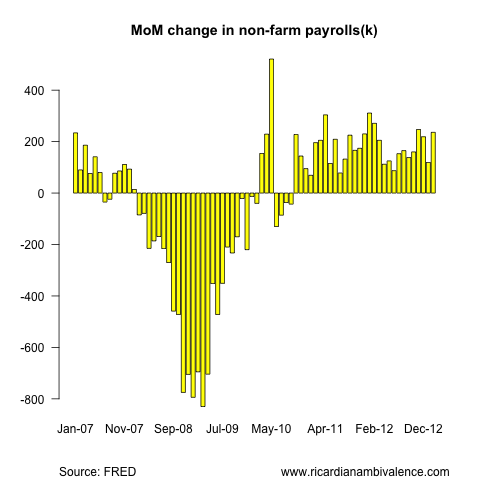

The February non farm payrolls report was better than most expected, with establishment employment estimated to grow by 236k jobs in Feb (mkt was ~170k), though net revisions took about 15k of these (Dec +23k to 219k, but Jan -38k to 119k).

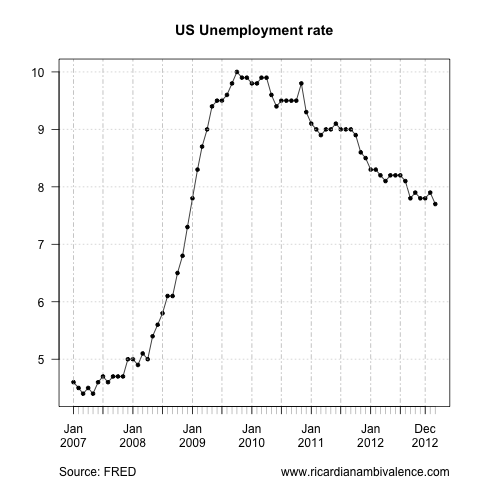

The unemployment rate dropped back down to 7.7%, and though it is now moving in the right direction once again, it hasn’t moved much over the prior few months. Perhaps this is payback for dropping too quickly previously.

In terms of the recovery from the crash, the US labour market (as measured by establishment employment) is now as far away from the peak as is typical at the bottom of a ‘normal’ recession.

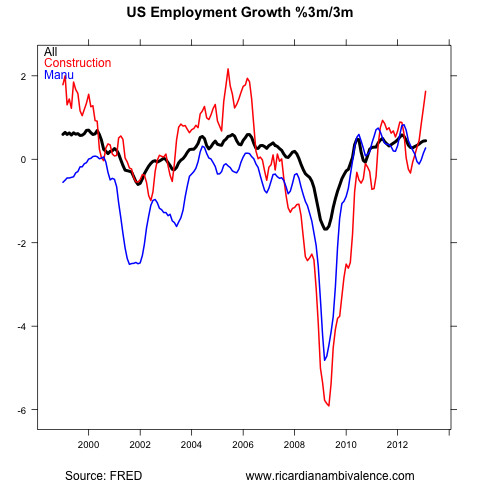

Sure, this is bad — but there is also a positive spin we might put on it. There are encouraging signs that we are starting to see some of the things associated with a normal end of a recession. Robust growth in cyclical interest rate sensitive sectors such as construction is especially encouraging.

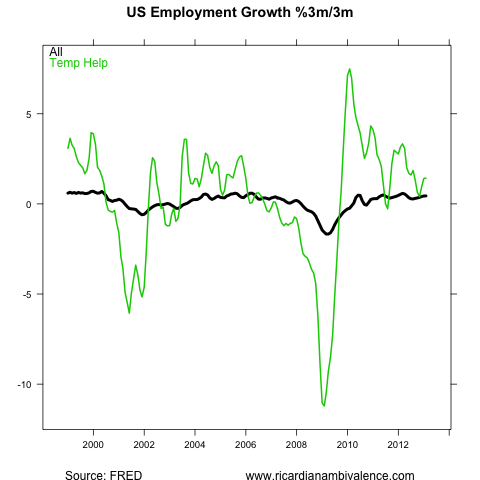

There are also signs that temporary help hiring (a typical precursor to full time employment) is starting to pick up once again.

While employment growth has recently been lacklustre in Manufacturing, the work week has been extending – which typically presages a pickup in manufacturing employment.

Manufacturing hours simply do not extend much past this – current hours per week are about as high as they ever get. More people will be required to further boost production.

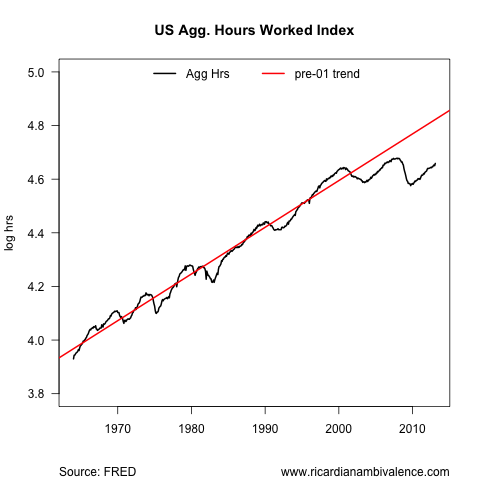

The general extension of average hours, and increase in employment has boosted aggregate hours — relative to total jobs, it is a little closer to the prior peak.

Of course, that leaves a still massive gap between where we are now and where we might have been had the prior trend held.

This relationship is a decent first blush at an output gap, and finding the difference pegs lost output at a troubling ~15% of output.

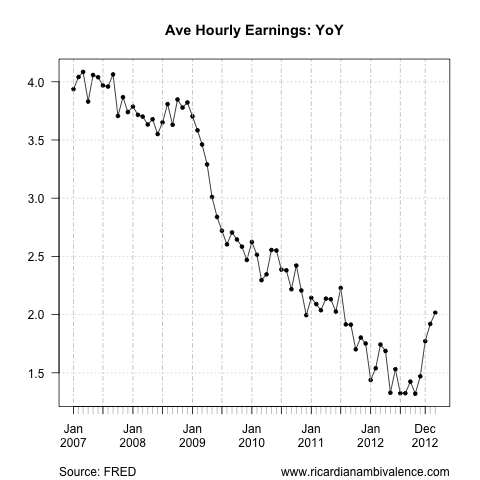

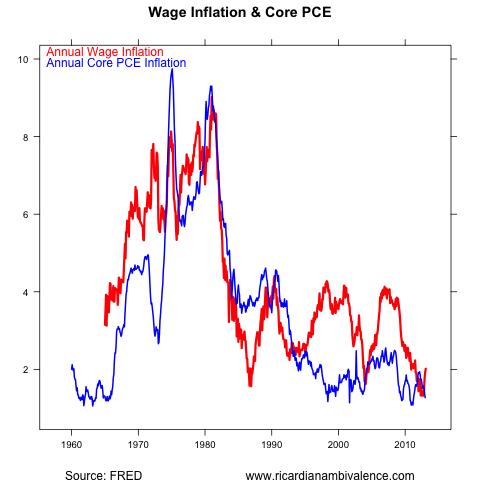

Reflecting the fact the the labour market is firming up somewhat, we are starting to see a pickup in wages growth.

As labour is the main input to production, you cannot have a core inflation problem without having a wages problem. The US is closer to a deflation problem than an inflation problem just now, so rising wages will be welcome.

So where does this place us with regard to the FOMC’s eventual exit from their current 85bn/month of buying?

A test laid by Chicago Fed Evans is averaging more than 200k payrolls jobs per month for at least a six month period. We remain a modest way below that pace just now, so it seems that tapering will be something that is only talked about at the March FOMC meeting.

The emerging trends are encouraging – but i think the core of the board (Bernanke, Yellen, Dudley) will want to see them develop further before making any changes.

Their new policy tools are working – let them work a little longer.

What those charts also show is how weak the 2003-2007 recovery was in terms of hours worked by post-war standards. Some of this may have been due to demographic factors (baby boomers retiring), but part may have been due to monetary policy being too tight over those ‘boom’ years. An early exit now would simply compound that problem.

IF we are having a “housing recovery”, then it’s on quite low volumes…

http://www.macrobusiness.com.au/2013/03/housing-finance-falls-again-on-fhbs/

Investors seem to be the only one able to get the credit needed to purchase (they are investing at 2007 boom level) probably because they have existing equity. But FHB have left the market again and without FHB there will be significantly fewer upgraders in the upcoming months.

There sure is an interesting divergence between the hood time to buy a dwelling part of the consumer confidence survey and housing transaction volumes. As you say, we need new buyers at some point.

Well, yes, it’s now a good time to buy a dwelling because rates are low…. but hey, what will happen when rates stop falling or even start going up? Can I afford my repayments then.

Forgot to add…. many of the investor loans are taken out as “interest only” and/or from a line of credit and by being “interest only” they are almost positive geared. That will obviously stop when/if rates go up or the bank asks to start repaying the principal. There’s also investors buying within the SMSF umbrella. I think in this first quarter of 2013 we are basically seeing the effects of the hunt for yields, with money moving from Term Deposits into high-dividends Shares, mostly banks, telcom, and into property. However I think consumers are still not approaching credit like before the GFC and the saving rate is still high (or normal now, as opposed to too low then). So this could be a one-off push, caused by rate cuts and expiring term deposits looking for yields. I think it is still to be seen if it’s going to be sustained and if rate cuts have really an impact on the new saving propensity of consumers.

Cameron Kusher of RPData:

– Owner occupier refinance commitments have fallen by 10% over the year and non-refinance commitments are down 0.8%

– The total value of investment finance commitments in Jan-13 is up 4.4% over the month and 18.6% yoy

– 5799 FHB finance commitments in Jan-13 nationally, lowest volume since Jan 2004 (5,636)

– Qld’s proportion of FHB owner occupier finance commitments in Jan-13 was also the lowest on record at 10.4%

– 7.4% of owner occupier finance commitments in NSW to FHB in Jan-13, lowest proportion in history

and house prices were up in January…..

We need some real analysis of the unemployment data from yourself asap! :)

The seasonal adjusted numbers just do not make any sense. All of the sudden the participation rate jumps 0.3 in one month and they all find a jobs waiting for them, all in the same month, all 70k of them? Since abs data is moving billions nowadays, can’t we put more money into producing stats which have a smaller margin of error? None of the other employment data pointed to the biggest job numbers jump since since 2000! Very suspicious.

I looked at the error in the US employment surveys and found this VERY interesting document:

http://www.bls.gov/web/empsit/ces_cps_trends.pdf

cheers

Peter Martin has a column on the jobs numbers, referring to a survey rotation issue.

Thanks, yep, as you said in the past ( and I still remember! :) ), this report is NOT designed to measure the total employed persons month to month as for that projection it relies on population estimates, which are continuously revised. But the show has to go on. The unemployment rate seems to have stabilized at 5.4% so far, and that’s the main outcome. I’d suggest to the ABS to drop the seasonally adjusted employed persons number and only report that number at the trend level.