The exit of Ford from Australian vehicle manufacture has flushed the rent seeking club out once again. Their arguments range from the sad and true but irrelevant (what else are elderly skilled workers to do — which is an argument against change) to the clever (manufacturing has special ‘spillover’ benefits).

The spillover story is the most compelling for subsidy, as we want to subsidise things that don’t get rewarded for all they give to society. Within this, i think the RnD story is strongest.

With so much noise in the debate, i thought it worth reviewing what vehicle manufacture contributes via research and development (my source is the annual ABS BERD publication, 8104). I have split manufacturing into transport and non-transport (you do not need to assemble in Australia to have a great parts export industry).

So who does RnD in Australia? Listening to the debate, you might think it is mostly the car manufacturing industry. You would be wrong.

Of all the RnD we do, the transport manufacture industry is about 5% of the total. Mining and manufacturing ex transport do a similar share, at ~21% each. Finance and professional & scientific each do about 15%

We need to dig deeper, however – for all RnD is not equal. The stuff with the best claim to ‘spill-over’ benefits is the basic stuff. The more general the RnD, the more likely it is to benefit a broad range of activities.

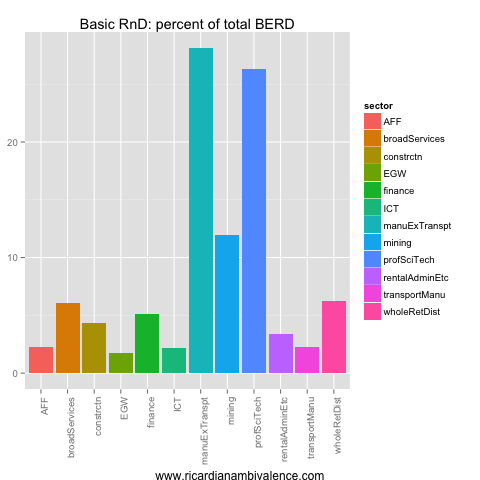

On this score, transport manufacture does about 2%, a little less than Agriculture & fishing. Again manufacturing ex-transport is up there (28%) as are the professional & scientific areas (26%). Mining does about 12% of this RnD.

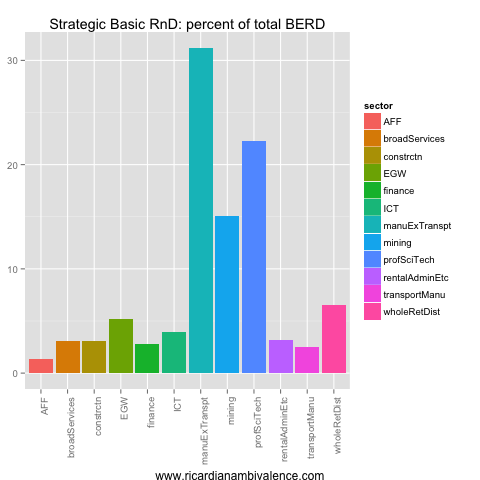

The next level up (less general) is what’s called strategic-basic RnD. Here transport manufacturing is ~2.5%, less than construction, finance, and the service sectors i aggregated together. Manufacturing ex-transport is 31%, science is 22%, and mining is 15%.

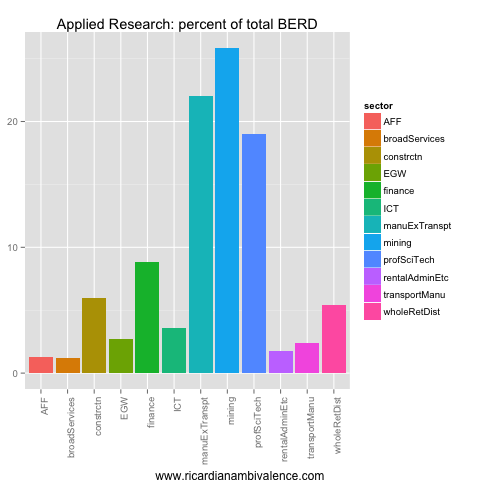

Another step up (less general) is applied research. Here transport manufacturing is 2.4% of the total. Broader manufacturing ex transport is 22%. Mining is 25%, science is 19%, and finance is 9%.

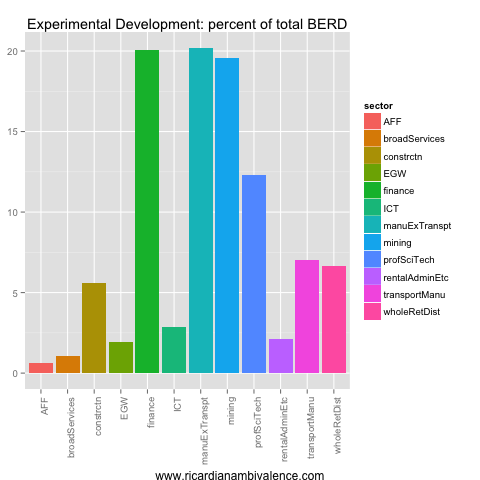

Finally, we get to experimental development. This category is basically a production subsidy, wrapped in a WTO compliant cloth. Here transport manufacturing leaps to 7% of the total. Manufacturing ex transport is 20%, finance is 20%, and science is 12%.

A comment on these facts – the subsidies are being spent on production, so unless you buy the specific car that was subsidised you are unlikely to enjoy much benefit from the government’s support. How much better to give this money to the science guys to spend on basic RnD?

Finally a broader point – Australian manufacturing is dynamic and innovative. It does plenty of research even if the government is not heaping ‘RnD’ subsidies on it. Indeed the data suggests that the unsupported bits do more ‘basic’ RnD than the supported transport sector.

A little comment.

most people employed in the ‘car’ industry are involved in sales or servicing.

Therefore the cheaper the cars the more people employed.

no manufacturing here would see more people employed in sales and servicing!

ironic eh!

Haven’t heard that argument before …

is that a yeah or a nay?

I think it may well be correct!

Awesome post!

Thanks Katy.