Last night’s price action spoke to the virtues of sleeping deeply and turning off your phone. First, better than expected data drove yields higher (US 10yrs tipped 2.7%) and then the Fed downgraded their growth assessment and sounded more worried about low inflation, and yields came back down.

So which is more important? The data, or the change in Fed language?

I am tipping the data. The Fed is still looking toward the exit, and their next move remains a tightening of policy. In this environment it is hard to fall in love with duration / out of love with the USD.

Still, it seems to me that Sep-taper had become very consensus. It is clearly up to the data to deliver.

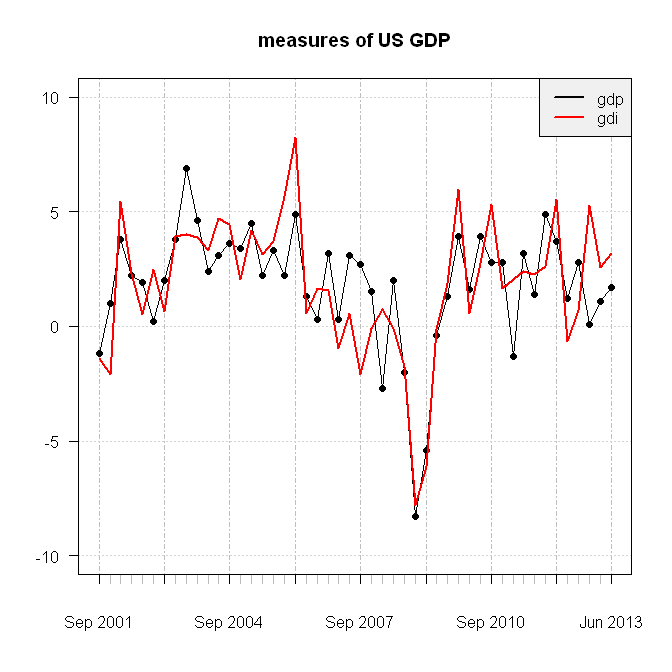

That basically means that it is up to payrolls to prove the apparent weakness in GDP wrong. That is very possible. Many researchers think that real GDI is a better measure than real GDP, and this has picked up to a 3% pace over the last year (GDP remains stuck at around a 1.5% pace).

If real GDI is right, there is less tension between the falling unemployment rate and labour market data – and therefore less reason to expect that the labour market will soften up. That ought to be enough to keep Fed tapering on track for September.

In practice, it does not matter when they go , as markets have already decided to tighten for them: all yields are up significantly since they started talking about reducing QE. I wonder if they are regretting doing that now and if they expected this kind of reaction.

I think the Fed has completely stuffed this up. I see very little chance of a taper before the end of the year – but as ssec noted, the rise in yields is already the tightening in monetary policy.

Payrolls will decide. I agree with you both — the market has delivered the tightening, as they must have know it would when they surprised the market with an ‘early’ move to taper.

You can see an emerging downtrend in the weekly mortgage purchase applications series.

It is weird to taper with nominal gdp weak and inflation low – they must be very confident about the labour market and inflation. Or perhaps they are just very wrong.

Well, 30-Year mortgage rate went from 3.5% to 4.31% in a couple of months, the highest level in 2 years, that’s definitely tightening. Apparently house prices in California are up 25% y/y, so maybe …..

The economic data is very strong and last night’s data was evidence of that. I am not a fan of headline GDP because it is understating how strong the U.S. private sector recovery is at the moment.

The problem is the output gap is still so large and inlation as a result remains so low. Why you would allow such a tightening of monetary policy in that environment can only speak to their general incompetence. They have an opportunity to really let GDP and jobs rip for a while (and why not a bit of extra inflation later on as well), and then they go do this!

Bring on Janet Yellen I say!

Well, ECRI is still claiming the US went into recession mid last year and still in it presumably.

Hang onto your black box!

nein! nein! nein!

RA, interested to get your thoughts on the non-farm payrolls out last Friday. Looked mixed; lower UE but lower part rate. btw, here’s the link to my latest post on Australia’s productivity renaissance post