I missed the mark with regard to Gov Stevens’ speech yesterday, at least as far as the market was concerned. For, while much of what he said in his speech has come out of the RBA in other communications – or was calculable given what they had told us – the market reacted as if it was new-news, and cash rate expectations declined.

Thus, on the only score-board that matters, i was wrong that he would not sound 80% sure. Following the speech, the market was left pricing in ~90% chance of a cut in August – up from ~80% prior to the speech.

Some point the finger at his repeat of the scope to ease line from the statement and minutes:

We have been saying recently that the inflation outlook may afford some scope to ease policy further if needed to support demand. The recent inflation data do not appear to have shifted that assessment.

This was surely a line that the market reacted to – however we knew the inflation result was around their forecasts, so for me this was not the entire story.

That story was really a lower-for-longer story, where slow consumption growth took centre stage.

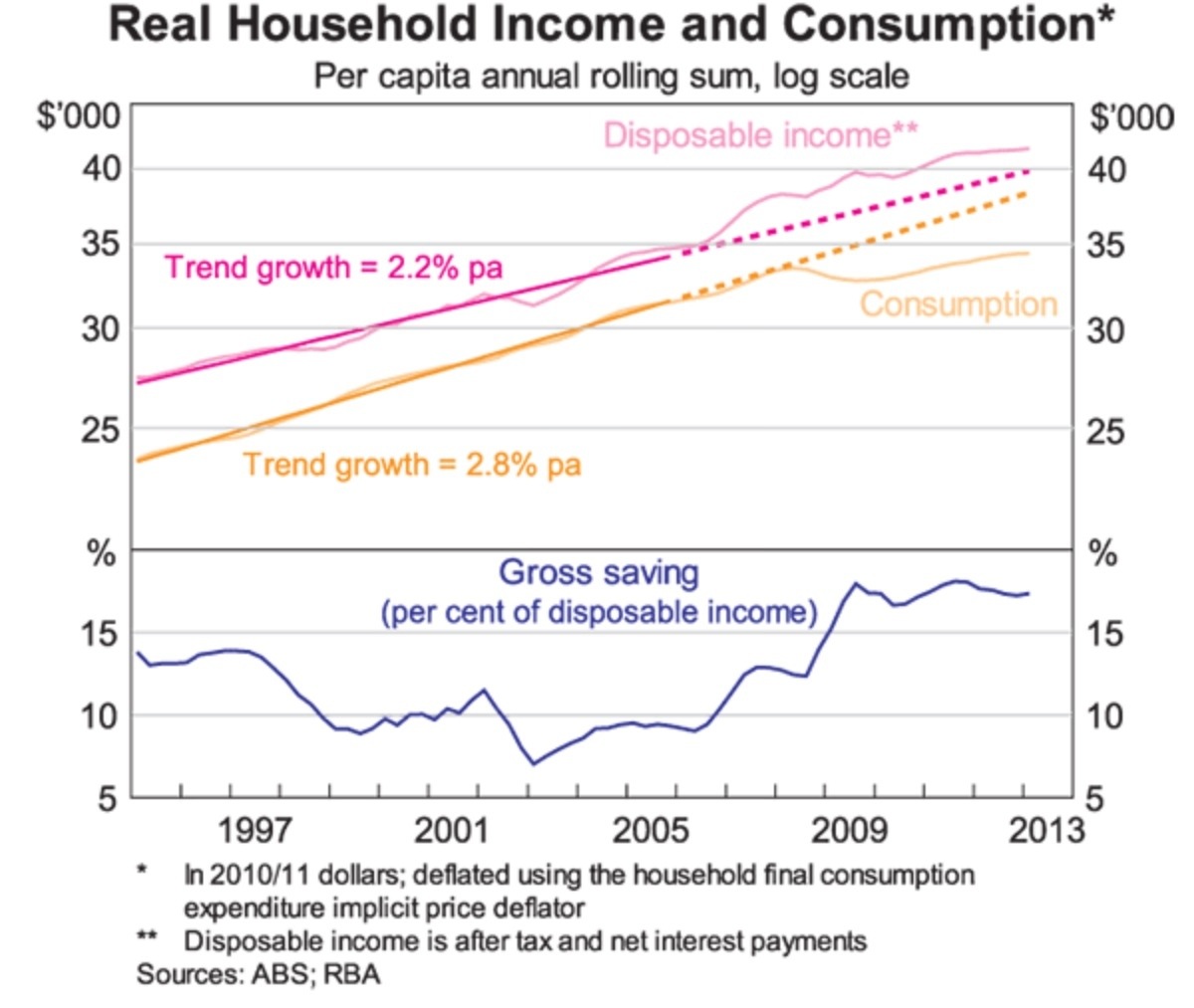

Gov Stevens recycled two charts from a speech two years ago (updated, of course). The first shows the slowdown in both income growth and consumption growth – along with the increase in the saving rate.

The implications for rates are familiar for those who have trained – more supply of investible savings lowers the market clearing price, which means the equilibrium cash rate has declined. Of course, in some models slower consumption growth also means lower equilibrium rates.

For the question of why, Stevens again gave the answer ‘House prices’. The emerging bank view appears to be that the credit boom boosted house prices and that they will hold around this level in real terms, perhaps declining slowly for a time first of all. If that is the case leveraged housing investment isn’t a great alternative to saving, and folks will therefore desire to save more from their income. I agree, and think that this is what we are seeing.

So long as income growth is weak (which is what the falling terms of trade will do) and house price gains do not drive sizeable gains in wealth (and hence rapid consumption growth) it seems likely that the equilibrium rate will remain well below what we’ve been accustomed to in the past (even after accounting for spread widening).

The old neutral was a real cash rate of around 3%. My best guess is that spreads are worth 100bps, and that these structural factors are worth another 100bps, which means that the neutral real cash rate is around 100bps, or maybe a little higher.

With cash headed for 2.5% and inflation around 2% just now, we will be about 50bps stimulatory – which fits pretty well with the fact that a few of the interest rate sensitive indicators (such as auction clearance rates and house prices) recently picked up, when cash got to 2.75%

It is pretty normal to get about 100bps below neutral in an easing cycle, which matches pretty closely with my guesstimate that the terminal cash rate will be 2% (though clearly the bank is in no rush to get there).

Not a bad speech, but the Governor is clearly in CYA mode. There’s not much there by the way of mea culpa that the bank has been too optimistic about the handover for at least the last 12-18 months. In my view, talking about not wanting to return to 7% real asset price increases and excessive rising consumer leverage is a straw man. We don’t need a sustained massive increase in household borrowing and perennial 10%+ pa house price increases to get NGDP back to 5-6% (where it should be), but we do need it for a year or two to catch up the last 2 years’ of weakness and get back to a reasonable path. I shrug my shoulders thinking where the RBA believes sufficient growth will come from to offset a decline in mining investment from 8% to, say, 4% over the next couple of years if not largely from housing investment, which needs higher dwelling prices. Stevens obviously would like to see an increase in net exports, but he can’t wait for that and it’s unlikely to be enough.

Ricardo I hope you don’t mind me providing a link to a mate of mine’s new blog. He has just made his first post and it’s on the RBA’s thinking. It’s categorically not me in case anyone’s wondering!

Nice blog. Seems like he’s an equity guy?

Thanks for the feedback Ricardo. Rajat has managed to pull me out of the last century and into the blogoshphere. I’ve worked in equities for over a decade, and in my current role I no longer have to publish research reports, so hopefully Skeptikoi will be a neat substitute. Looking forward to reading your future blogs. Anything that criticises the RBA is bound to elicit a positive response from Rajat :)

Thanks Rajat and I am the first to comment at Skeptikoi’s blog.

article is in Around the traps on Friday.

No Ricardo he in Shares!!!

:)

I wonder whether the Governor’s speech represents the RBA’s first foray into forward rate guidance? I guess only time will tell. Agree Ricardo that lower trend or potential growth ought to be associated with a lower neutral rate. I bought a book recently which sits on my growing ‘to read’ pile (Thomas Aubrey; Profiting from Monetary Policy) that got a good write up in the Economist. Aubrey recommends using a Wicksell framwork to better understand monetary policy; will have to look at in more detail. More generally, trends in the corporate sector suggest that monetary policy remains too tight; gross operating surplus declined for six consecutive quarters leading into the March qtr National Accounts. And the ASX200 remains 20% off its 2007 peak; even the Euro Stoxx index has done better :( Might be the topic of my next post.

Duly ,a href= “http://nottrampis.blogspot.com.au/2013/07/we-have-someone-new-to-blogosphere.html’>publicised. Invoice is in the mail

make that PUBLICISED. I am hopeless