A funny thing happened yesterday. It was not the RBA dropping their easing bias — which was fairly obvious given the Q4’13 inflation surprise — but the way the market traded on the news.

To see why this was odd, we need to rewind so as to give context to market pricing before the statement was released.

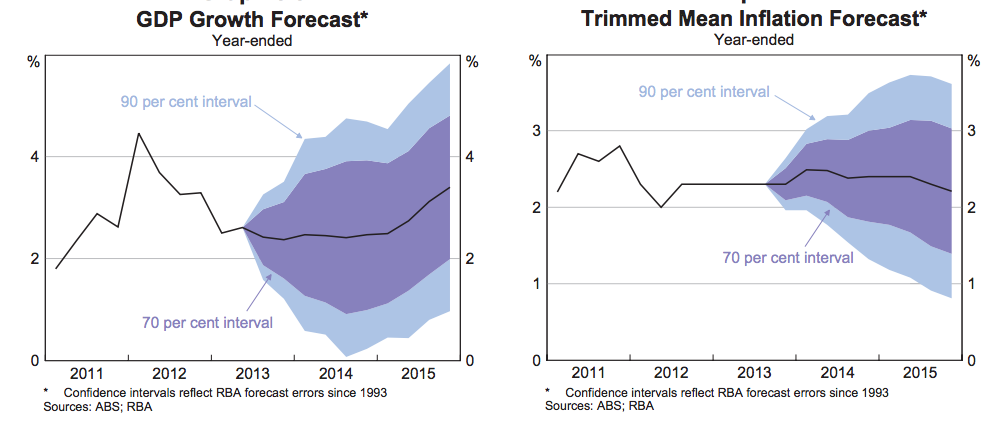

The above charts (from the Q4 SOMP) summarise the situation following the November RBA meeting: their central forecast was for growth to remain below potential (which is thought to be about 3%yoy) until mid 2015. As a result of this weak growth outlook inflation was expected to be around or below the 2.5% target for the entire projection period (the tick up and down mostly reflected the pass-through of a lower exchange rate to prices).

Given a forecast for growth that is too slow, and the fact that inflation was expected to fall back below 2.5%y/y once the weaker currency was fully passed through, it was no surprise that the RBA had been telling the market that cuts were the most likely policy step over the visible horizon.

Reflecting this, they put the following into their minutes (in both November and December):

The Board’s judgement remained that, given the substantial degree of policy stimulus that had been imparted, it was prudent to hold the cash rate steady while continuing to gauge the effects of earlier reductions, but not to close off the possibility of reducing it further should that be appropriate to support sustainable growth in economic activity, consistent with the inflation target.

So at the conclusion of the December meeting, the RBA’s message to the market was cuts were more likely than hikes. This is not what was priced, however: the market had only a very small bias toward further cuts. A fair summary was that pricing suggested that cuts and hikes were about equally probable.

By the time we hit the yesterday morning, that’s surely what was priced: the Dec’14 bill implied a 3m rate of around 2.7%, which is basically consistent with the RBA being steady at 2.5% (the current 3m fix is around 2.6%). Reflecting this, I had figured the market was pretty much priced for the RBA dropping their easing bias (meaning that pricing suggested cuts and hikes were as likely as each other – which is pretty much what ‘neutral’ means) and that we’d not see much of a move when the RBA made the change of bias explicit in their statement.

Well … i was very wrong about that! The Dec 14 bill has sold off 11bps since the announcement (above chart) and the AUD rallied sharply (below chart), to be up by about 2c against the USD.

To my mind, this is exactly what the RBA wanted to avoid. It is in this context that I think we should place their experiment with ‘forward guidance’ in the post meeting statement.

On present indications, the most prudent course is likely to be a period of stability in interest rates.

My view is that the RBA knew (from experience) that losing their easing bias might cause the market to price in rate hikes, and they wanted to avoid this inappropriate increase in yields (and consequent appreciation of the AUD). Forward guidance was their attempt to prevent this from occurring.

If you take this perspective, it neatly frames the ‘if sustained’ comment about the weaker AUD — the implication being that the RBA’s easing bias might re-appear if the market gets it wrong and pushes up the AUD.

Clearly the price action tells us that their first experiment with forward guidance failed — but i expect that the RBA will continue to elucidate the case against rate hikes in coming days and weeks. We still have the same domestic issues (terms of trade decline / mining investment drop, and the need to tighten fiscal policy to close a structural deficit of about 3% of GDP) and there’s the new EM downside risk to add into the mix.

Given this backdrop, it’s hard to see how the labour market might get tight enough to create a core inflation problem — which is what’s required to get rate hikes.

Contrary to popular press, we don’t have an inflation problem at the moment — we have some FX pass-through and price hikes in semi-administered ‘non-tradable’ goods. Folks cannot substitute away from these goods in the short run, and wages growth is very weak, so this sort of inflation is likely to work like a tax hike and sap spending power.

Domestic headwinds continue to blow hard, and offshore headwinds are rising (if our trading partners get weaker currencies and higher rates it will be bad for our exports), so (partly because the market got their ‘forward guidance wrong’) it’s most likely that the RBA’s next step will be to re-instate their easing bias.

Any tightening bias seems at least a year away.

Welcome back, Ricardo! And thanks for such a meaty first post of the year. Very interesting what you say about what the RBA was trying to achieve with its ‘forward guidance’ and ER comment; it sounds right to me.

I think part of the confusion in the ‘popular press’ (that means you, Koukie!) relates to what inflation targeting is all about. Until I started reading Sumner, I thought that a rising CPI – regardless of where it was coming from – was a bad thing that warranted tighter monetary policy because otherwise resources would be misallocated. This is how much of the popular press think. But now I think that if the CPI is rising because the AS curve is shifting to the left, because of increased regulated charges and taxes or because of a falling dollar, then it doesn’t make sense to tighten. Accordingly, I think an NGDP targeting approach, which could be read into the RBA’s ‘over the cycle’ mandate, seems to make sense. But while the popular press interprets this wording to mean that it is ok for the RBA to miss on the upside if demand is strong and on the downside if demand is weak, I think it should be understood in almost the opposite way: it’s okay to miss on the upside if demand is weak and we have non-demand-related cost-push pressures and it’s ok to miss on the downside if the we have strong demand and falling exogenous costs.

I think that view is going to win the day. You sumnerians are gaining ground – it is pretty much what the Bank of England had done these past five years … if EM sucks the resources sector and AUD down, i think the RBA would do basically the same thing.

In fairness to the RBA, that’s more or less what they did in Q3/2008 when the CPI was still high (due to oil prices) and the AUD was falling: They presumably cut in the knowledge that a (2011) BoE-type story could unfold. That time, the GFC rate cuts did not cause inflation to subsequently materialise, probably because the demand and ToT shock swamped the impact of the depreciation. But the RBA took the risk and I agree they would probably take it again if the various headwinds ramped up. Don’t see much ECB-style self-flagellation happening! Having said that, I think the RBA gave us some unnecessary repression under somewhat less threatening cost-push conditions in 2011 and 2012.

Agreed, in retrospect they totally misjudged mining boom II. it would have been best to hit this downturn with 4.5% unemployment

Could the bigger implied 3m rate out of dec 14 be 1s3s increase? What did IBs / OIS do?

3x1for a year stable around 4.5bps

I think this was just short-squeezing of a pretty much oversold AUD. We all know the RBA does not want a higher AUD or else… but for now, all shorts were squeezed!

Myself, I am still trying to understand where from here for our economy. As the RBA said, the situation is finely balanced between pluses and minuses, but it can fall on either sides fast IMO.

Overall I am not concerned about inflation at all, how could you be when we have mostly advanced economies actually trying to fight deflation and a mining boom close to an end?

There is one thing thought that “bothers me” however! What if the economy DOES NOT need a lower AUD right now? There’s so many bearish people on AUD, they could all be wrong. I am still AUD short myself, but wondering!

Welcome back! :)

To me it comes down to the following question: could NX, consumption and non mining investment take up the slack that is going to be left by mining and government spending. I think they might, so long as the rba keeps rates on hold for a long time, the AUD track sthe ToT down to 80 or below, and our trade partners don’t stumble.

But even if we get all those things, it is hard to see a tight labour market and a core inflation problem. As you note, the rest of the world has a deflation problem.

Of course it is more likely there will be a few stumbles, which that will prevent the savings rate falling, and keep demand growth shy of what’s required to close the gap for a year or so.

Yes, I agree.

Especially in the shorter term (e.g. 2014) we could get a construction bounce due to lower rates that will balance a slowish fall in mining, so rates on hold, but longer term e.g. 2015, I do not think we will be able to replace the mining boom with another boom and the impact of previous rate cuts and investor activity could be diminishing already. Overall I agree with the idea that “it has been all about commodities and China in the last 10 years, it’s now going to be about USA and Europe recovering” which for Australia means lower ToT with all associated effects.

That’s the key question about housing: will it just adjust to the lower level of rates and stop adding to growth, or might we get an ongoing push if rates stay this low? I favour the former, so it seems likely to me that the growth add/push if fairly mature on that front.

About damned time I say

I,like you, am a tad sanguine about inflation.

The output gap and then wages growth both suggest inflation should not be a problem for some time to come.

I think your position re the RBA is correct.

After being burnt by two rogue CPI numbers back when Inflation looked like is was low but other factors suggested it should be rising I think they will wait to be sure.

Rates rising in an economy still weak will have an impact!

what do you think of the CBA thesis re Current Account surpluses I have reproduced on my blog?

I think the view has merit, but much of the income from exports will accrue to foreigners, so it may not be the massive upside he expects. Still surpluses are possible – higher NX is a way out assuming lower G and limits to consumer leveraging.

Given today’s strong retail sales data. the contrary view is that the circumstances are similar to October 2009 when rates started rising post-GFC. As you indicate, the key missing component this time seems to be the labour market: trend employment (unemployment) is still falling (rising), while it was rising (falling) for a bit before Oct 09. Plus, I suppose, this time we have a mining capex fall-off and tighter fiscal policy (?) to negotiate.

Dec was a tax hike boosting nominal food right? ex food it was down about 1%. bigger picture, my view here is the spending that was outside the survey frame (foreign online retail) is moving into the frame as folks substitute back to domestic sellers. This is adding to pricing pressures – as the marginal foreign seller’s price is rising with the drop in the AUD.

As for the big picture comparison with 2009, at that time we had an obvious mining investment boom coming and a large fiscal push in train. We have neither of those now.

I agree. Plus these are the retail sales for Christmas after a new govt was elected and the many rate cuts during 2012 and 2013. Sales were good in the states where housing is doing well, and there is a correlation with building approvals too. In reality, I think the RBA needs much better than this, seeing that rates are already at record low. Let’s not forget we were used to living in a boom that started in 2005!

Do the RBA forecasts change the story? What if some in markets knew that RBA was about to announce they were expecting inflation to breach 3%? Plus GDP forecast increase. NGDP growth too high? Or probability of hike higher?

http://m.theaustralian.com.au/business/economics/rba-warns-inflation-could-breach-3pc-target/story-e6frg926-1226820513033

Hi Manny, IMO, Australia inflation is “self-adjusting” to the rest of the world and monetary policy in the US, Europe, China and Japan count a lot more than local monetary policy.

After having cut rates aggressively during the GFC (2009), the RBA could have stayed put since then and nothing would have changed at all. But I guess they must justify their job….

Does anyone really think Australia will have an inflation problem in the short term (2014)? We will have an inflation problem when/if the rest of the world will, anything else it’s a one-off and will simply self-correct, e.g. give it a couple of quarters and inflation will be back to the mid of the band or lower. The AUD will do the job for the RBA. It already stopped falling. If housing is a worry, introduce LVR limitations. :)

The RBA wanted a lower AUD, they got it, and it comes with some form of short-term inflation, that’s what they wanted isn’t it? Let’s be honest, in a country where private citizens have taken on a massive amount of debt, it’s not inflation that it’is the problem…. The RBA is happier with 3% and a lower dollar, rather than 2% and a higher dollar, as they have demonstrated in many occasions before!

RBA forecasts vs Goldman Sachs ? I take Goldman Sachs. cheers