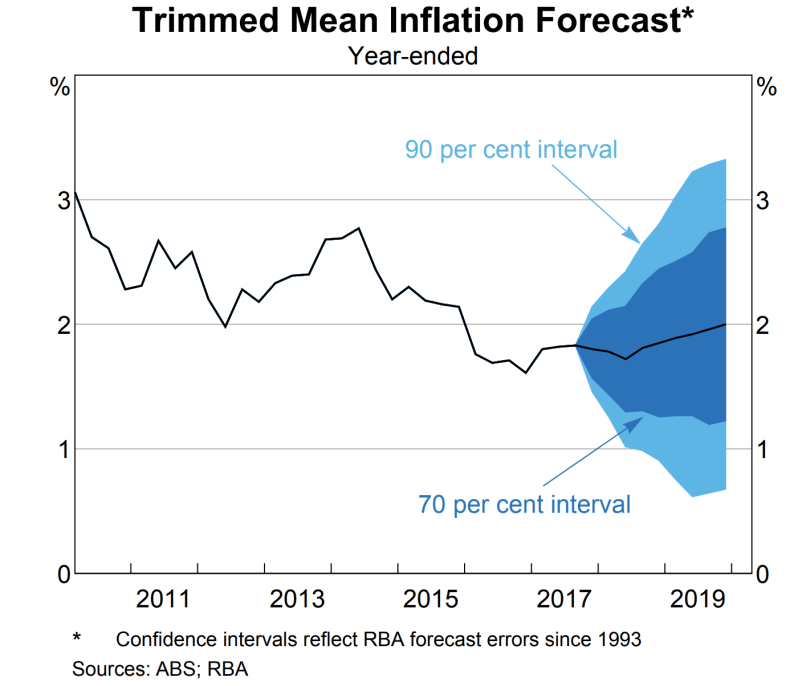

Say you were the Governor of an inflation targeting central bank and wanted to communicate to the world that you were not about to raise rates — what would you do? How about forecast that inflation remains outside of your control range for your entire forecasting horizon. That’s what the RBA did today.

As you can see from the above chart, the RBA’s central forecast for Trimmed Mean CPI (their preferred measure) is for it to remain below 2% until 2020. Recall that their target is 2.5% inflation, with a 2% to 3% control range. The inflation number tracks up about 25bps per year, so i would assume that the model tells them that inflation hits target sometime in 2022!

These forecasts assume market pricing for the cash rate, which means that the current pricing of a first hike in Q4’18 is assumed in the case case. The only interpretation of this is that the RBA is telling the market — you’re wrong, we are not going to hike in 2018. On these numbers it is doubtful that they’ll hike in 2019.

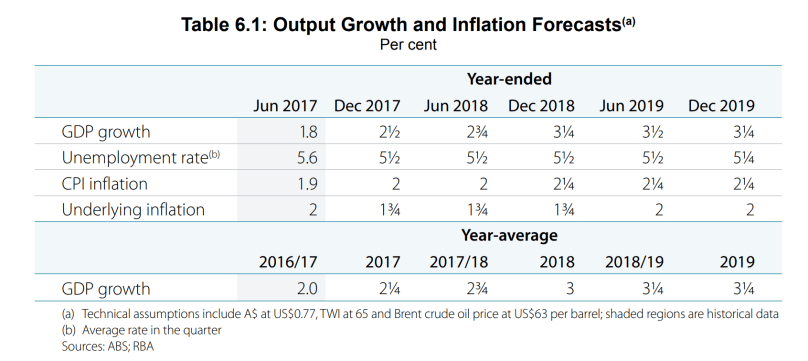

Despite the shibboleth about forecasts being ‘little changed’, the RBA cut their growth numbers today. This is the tradition. Like the horizon, 3% growth is always about the same distance away. I think that their growth numbers remain too high. The Economy has been undershooting their growth numbers for a while now (we were supposed to be at 3% right now 1yr ago).

Recall that these changes are despite a lower AUD and a higher oil price.

Finally, the bank cleaned up their forecast table a little bit — in the process making it a little easier to integrate with their charts. I think a 2% for core CPI is more transparent (than the 2% to 3% range) and easier to understand.

The message is clear — we’re not raising rates. How could they, when their job is to make CPI 2.5% (while trying to keep it between 2% and 3%) and they don’t know when they’ll hit their target?

We need a stronger Union movement and less deregulation???

Ha I don’t think so!

being serious now de-regulation has a dark side. Perhaps we are now experiencing what is normal for the USA for example

I don’t think low inflation is as evil as some do. Growth is not too bad. The labour market is pretty good.

It’s the slow household income growth and raging debt level that’s the problem. If the household sector cuts back on its rate of borrowing, as they surely must, the RBA will be cutting rates not raising them.

exacerbated by very slow wage growth courtesy of our quite deregulated labour market.

how do you get wages to rise as they should

Our labour market is too regulated, at least one FWC commissioner appears to be insane, but that’s not our major problem. The economy needs the household sector to keep borrowing to drive income growth. I think they’re close to tapped out. Mind you I was saying the same thing in the lead up to 2008, turned out to be a load of crap.