The RBA board will discuss the disappointing Q4’18 GDP data for the first time at their 2 April board meeting. The size of the downgrade is so large, and the domestic and global data for Q1’19 has been so weak, that I think they’ll respond by making a further dovish step — potentially to an explicit easing bias.

The Q4’18 GDP data delivered a ~50bps miss on headline GDP, with particular weakness in dwelling investment, household consumption, and household income. These areas of weakness were partially offset by an unsustainable increase in public demand.

The weak H2’18, and poor start to Q1 (both locally and globally) should see the May SOMP growth forecast fall into the mid 1% region (helped by a negative base effect as the very strong Q1’18 drops out).

With growth so slow, it would be remarkable if the unemployment rate didn’t starting increasing. And a rising unemployment rate means there’s no reason to expect an accelerating rate of inflation.

The global picture has also soured. Since the RBA’s prior board meeting on 5 March, major forecasters have downgraded global growth. The OECD cut 2019 and 2020 on 6 March; and the IMF is widely understood to have already done so once again (they already downgraded in January). The RBA would have a clear idea about the IMF’s April WEO downgrade — though we have to wait until the IMF release when the release the analytical chapters of the WEO on 9 April.

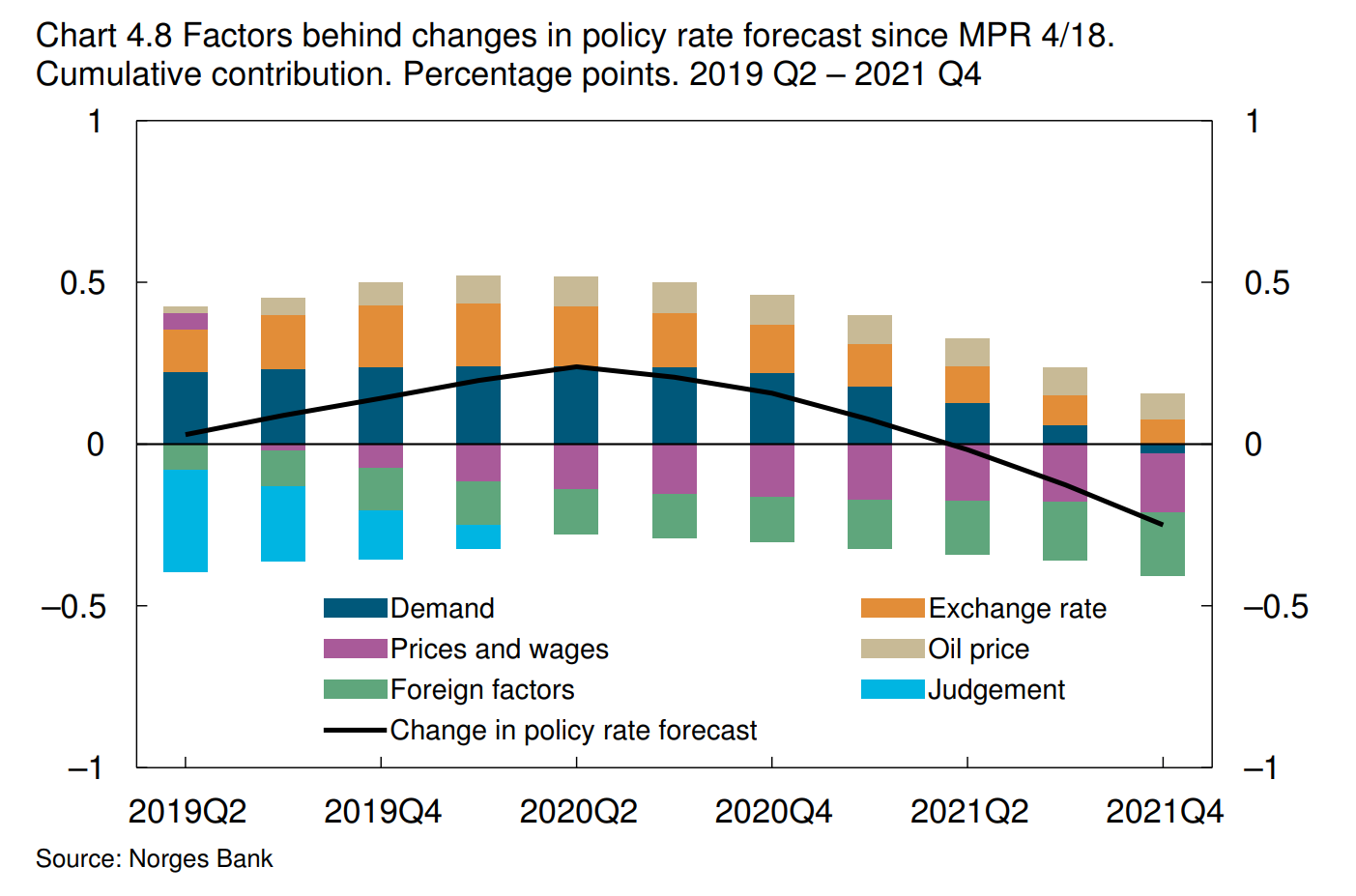

Anyhow, these are just words: the facts call for some empirical judgement about the importance of the recent global growth downgrade. I don’t have time to build an Aussie / Global model, but I did notice a nice chart in the Norges Bank’s March MPR that i have included below. This chart shows the contribution of various factors to changes in the Norges Bank’s policy rate forecast: between the 4th MPR of 2018 (13 Dec) and their 1st of 2019 (21 March).

The global growth downgrade has shaved off ~20bps (10bps in the near term, and 20bps further out). That’s a meaningful step.

It might not seem like much, but it was enough for the RBNZ. Last week Gov Orr said that “the more likely direction of our next OCR move is down”, due to a weaker global growth outlook (partly a weaker Australia) and slower domestic growth in H2’18 (note that Q4 NZ GDP was a decent +0.6%q/q v. Australia’s weak Q4 GDP of +0.2%q/q).