The market rushed to price in a July RBA rate cut, following Gov Lowe’s 20 June speech, The Labour Market and Spare Capacity. I’m not so sure.

On the surface the setup coming into the July meeting (speech 20 June and speech after the meeting) looks similar to the June meeting (speech on 21 May, speech booked for right after the meeting), there are a few important differences.

The first and most important is that the easing bias in the 20 June speech didn’t have a meeting date attached. You’ll recall that in The Economic Outlook and Monetary Policy, Lowe concluded that:

at our meeting in two weeks’ time, we will consider the case for lower interest rates.

RBA Gov Lowe, The Economic Outlook and Monetary Policy, 21 May

The easing bias in the 20 June speech is less specific. The section on monetary policy is reproduced below:

It would, however, be unrealistic to expect that lowering interest rates by ¼ of a percentage point will materially shift the path we look to be on. The most recent data – including the GDP and labour market data – do not suggest we are making any inroads into the economy’s spare capacity. Given this, the possibility of lower interest rates remains on the table. It is not unrealistic to expect a further reduction in the cash rate as the Board seeks to wind back spare capacity in the economy and deliver inflation outcomes in line with the medium-term target.

RBA Gov Lowe, The Labour Market and Spare Capacity, 20 June

So while there’s a clear message that rates need to fall further to put the economy on the right path — it’s not as specific about timing.

Anyhow, the need to cut further is old news. The RBA has told us multiple times that they baked 50bps of rate cuts (Aug & Nov) into their May forecasts, and that things would be worse if they weren’t delivered.

Gov Lowe reminded us of this fact in his cut setup speech on 21 May, and again in his immediate post cut speech, Today’s Reduction in the Cash Rate, on 4 June. Indeed, in his 20 June speech he used language that is (deliberately?) similar to the language he used in his 4 June speech.

it is not unreasonable to expect a lower cash rate. Our latest set of forecasts were prepared on the assumption that the cash rate would follow the path implied by market pricing, which was for the cash rate to be around 1 per cent by the end of the year.

RBA Gov Lowe, Today’s Reduction in the Cash Rate, 4 June

So he has been saying ‘cuts to come’ for a while now — and the 20 June speech wasn’t a new development on the 4 June speech.

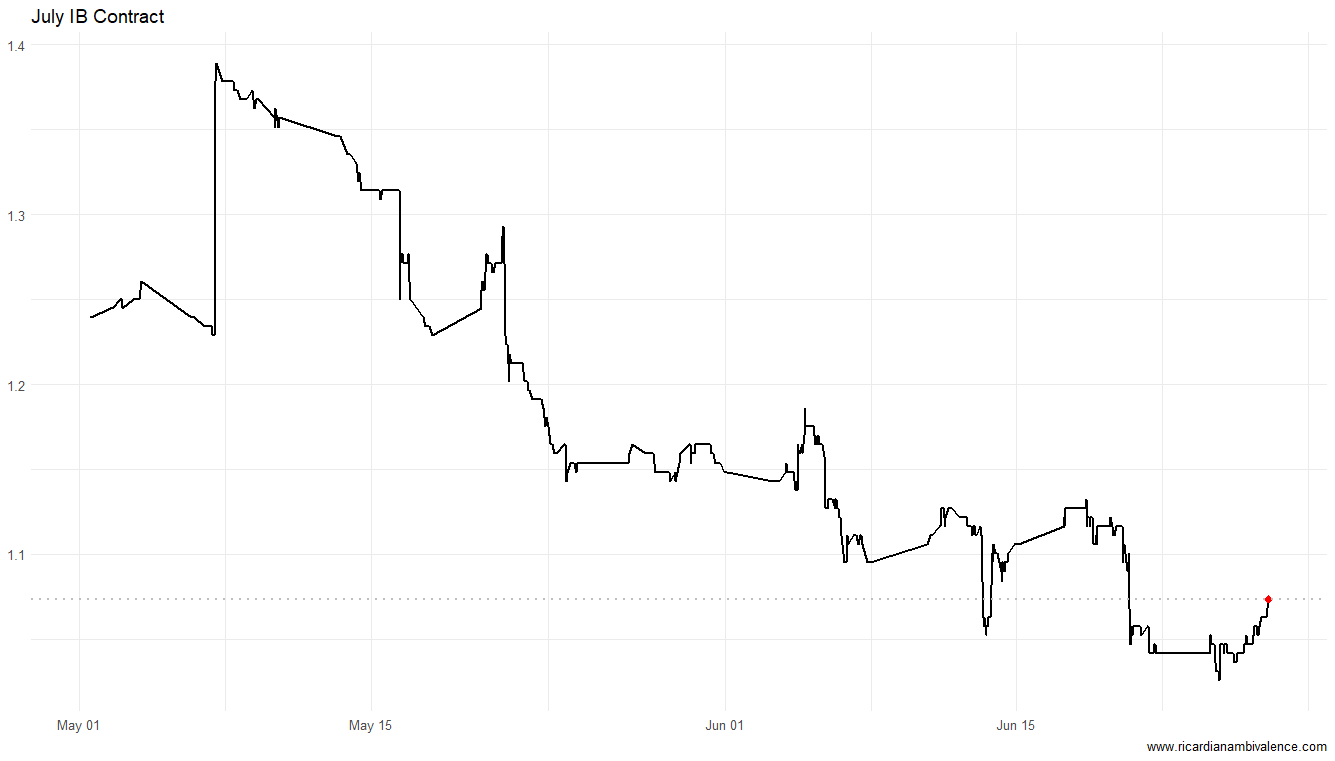

The post-meeting speech he has booked looks a bit suspicious — but look at market pricing! The market thinks a July cut is a certainty (it was ~90% sure last week). So particularly if he does not deliver a cut he will need to explain what’s going on.

But if his mind is made up about the need to ease, why not cut in July?

Well, why didn’t he cut in May — they assumed 50bps of cuts and produced a set of weak forecasts, so a rate cut should have been a lock. I suppose they wanted to wait and see…

Having waited to see, they decided to deliver on only one of those cuts in June. But if the baseline was two cuts, why not just do them both? I suppose they wanted to wait and see. Also, 50bps cuts are unusual.

Well, back to back cuts are also unusual. We last saw a pair in 2012 (May + June). Every cut since that time has been 25bps. And the six cuts from 2013 to 2016 were all 2x25bps on adjoining SOMP months. So July would also seem out of character — unless you had a growth problem, or figured you were clearly at the wrong rate. It’s an unusual action, so something unusual must exist to justify it …

The market certainly thinks we are in unusual times. But the Governor doesn’t seem to agree. He keeps saying that the May SOMP forecasts are on track — and since he’s got back from the G20, he’s been saying that the IMF was telling them that things were picking up (with the obvious caveats about the US-China trade war).

What about the NAIRU? Does a lower NAIRU create urgency?

Gov Lowe first said that he figured the NAIRU was around 4.5% in QnA following the speech, Trust and Prosperity, on 20 November 2018. The board sat on that view for six months before it decided to act. Doesn’t seem urgent to me.

So the situation is that the May forecasts are on track, and the IMF is growing more upbeat. The G20 is an imponderable, it might create a mess — but perhaps it will be benign.

And the challenge of keeping up with the Fed seems to be fading — with the ever-dovish Jim Bullard saying that he doesn’t see the case for a 50bps cut in July.

So no, I don’t think the RBA will cut their cash rate in July. It would be odd and out of character for a Governor and a Board that has emphasised that importance of the Bank being ‘a source of stability and confidence’ over the past few years.

I think after the next CPI release makes much more sense.

rogue CPIs have occurred previously. Just ask Glenn!

Agreed.

If 25 basis points doesn’t shift the dial then why wait?

If they don’t cut next week it’ll just be another example of the crap RBA crap communication.

Have to say, I agree all these points without any second thoughts. I find the ‘why wait’ narrative tiresome and lazy, and as you rightly note, it is distinctly out of character for the RBA to act in this way. That’s not to say the RBA isn’t irrational most of the time, because they are, and 15 straight months of trying to jawbone rates higher in the face of contrary evidence highlights this, but throwing all the toys out of the cot in this way would indicate that:

– they couldn’t even dream of being the ‘source of stability and confidence ‘

– they cannot come to well-thought out judgements about the economy even with an army of economists

– they are admitting panic and far lower rates

– all future RBA comments are rendered completely useless as guideposts to their thinking and future actions.

It’s also noteworthy that Lowe says he’d had his cathartic moment in NAIRU way back last year, yet kept the hawkish rhetoric in full swing as he and Luci continued to beat the full employment drum. It’s almost analogous to the easing recommendation put to Stevens by staff in 2014, yet easing didn’t come until 2015.

The RBA’s perennial hawkishness has not been positive for its credibility. Bias vs actual rate moves illustrates this rather well.

I didn’t know about the 2014 reccos. Very interesting. Please keep commenting!

Not many do … :)

The RBA seems to have a perennial hawkish bias, and seem to find it hard to ease when recommended to do so. Would make today even more odd, as well as a bit of a ‘panic’ move and further erode their credibility.

The real issue, though, is not the micro events of one month vs another, but the cycle/terminal rate, and (I feel) the RBA has already told us fairly clearly that the bias is firmly lower.

Your point about having to explain a cut to the Darwinians (and the rest of us) tonight why he felt such urgency would be fascinating to watch, and I can’t see how such a rapid increase in the ‘rate of change’ of easing isn’t taken as a sobering signal by consumers.

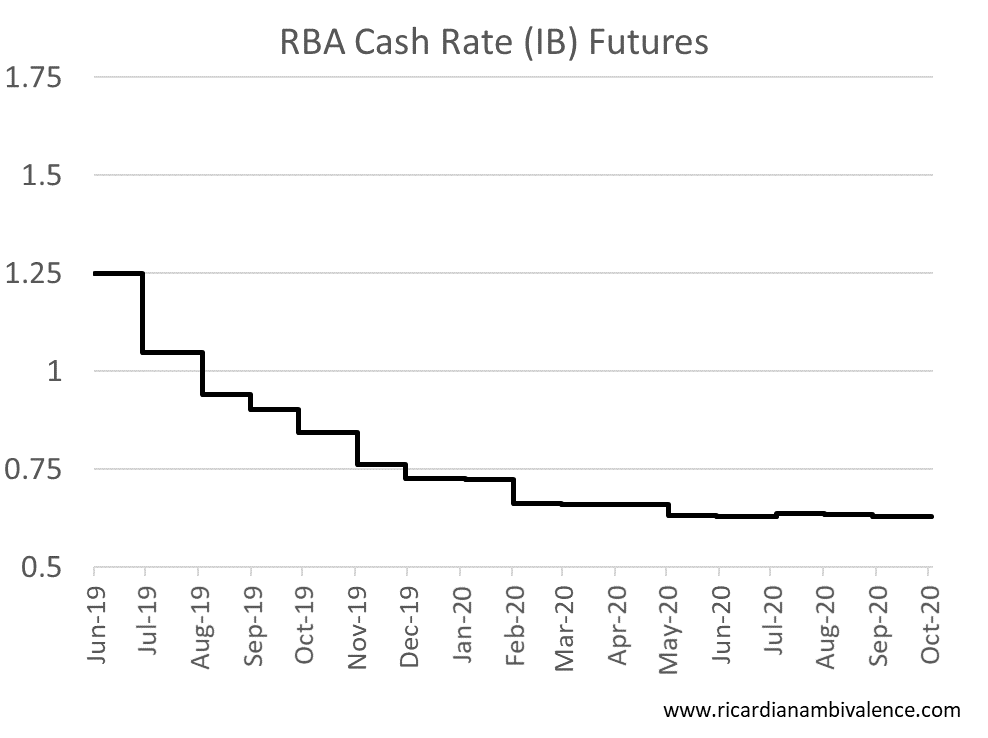

Below are the OIS runs (and the day prior) showing market expectations for the cash rate at the time of specific events.

It shows clearly that the RBA’s SMP forecast was based on 50bps of easing – BY FEBRUARY. Why the rush, Mr Lowe?

After 25bps of easing, the remaining 25bps was essentially spread from Aug-Oct. Any need to rush Mr Lowe?

The labour market speech seemed to get the masses excited, but as you say, there nothing definitive, nothing different, and a lot of the same as we had already seen.

May SMP Speech Labour Mkt

post-ease Speech

RBA Meet 10-May-19 4-Jun-19 20-Jun-19 Yest

3-Jul-19 1.345 1.159 1.057 1.062

7-Aug-19 1.247 1.049 0.951 0.954

4-Sep-19 1.205 1.013 0.911 0.911

2-Oct-19 1.161 0.976 0.868 0.869

6-Nov-19 1.075 0.9 0.781 0.786

4-Dec-19 1.062 0.884 0.754 0.754

5-Feb-20 1.016 0.838 0.691 0.691

RBA Meet 9-May-19 3-Jun-19 19-Jun-19 Yest

3-Jul-19 1.355 1.141 1.119 1.062

7-Aug-19 1.26 1.038 0.991 0.954

4-Sep-19 1.221 1.005 0.947 0.911

2-Oct-19 1.176 0.969 0.898 0.869

6-Nov-19 1.088 0.896 0.81 0.789

4-Dec-19 1.071 0.881 0.784 0.756

5-Feb-20 1.025 0.835 0.72 0.694

Look, this is the RBA we’re talking about. They could jump the shark here and toss all semblance of credibility out the window. They would then need to begin talking more authoritatively about ‘other options’.

They could also follow their process and wait. We didn’t have a -42 employment report last month … it was +42.

And I have had the bitter experience of the RBA failing to act on a day (more than one, actually) when they had the market even more fully priced and unequivocal data on which to do so … and then move the next month!

It’s like a jungle sometimes …

Well … i was wrong. To me this even more seriously suggests that the prior decision to pause in May was political. How can you cut 50bps in five weeks on a 9m old reassessment of the NAIRU?

Yeah, we both were, and May was definitely election-related (now proven beyond doubt). But as I always say to my colleagues and market economists, picking one month over another is a mug’s game unless you’re playing calendar spreads or something … though it sure is fun! The major point is the general direction, and given I’ve been calling RBA cuts (and 10yr bonds to cash) even before they gave up on the ‘next move up’ malarkey, I’m not unhappy. The cycle, and the reasons for it are the big show, and we have both been on the easing trade.

As for 50bps in 2mths … wow. I thought his 21st May speech was his comparable ‘whatever it takes’ moment, fresh off remarking one of their invisibles – full employment – lower. Amazing how much slack appears at the stroke of a pen! How they could be blathering about full employment *all* the way through 2018 in the face of nose-bleed under-utilisation is beyond me, but that’s a whole topic of its own related to credibility, not to mention models and specification. Ellis was a chief culprit here (which I find disappointing), and even tried to exonerate herself in her ‘invisibles’ speech by saying ‘as the data unfolded’ … took an awful long time and a lot of unfolding for this penny to drop.

So 50bps (minimum) was always a lock, just the timing, and 3 things come from that I think:

1. the RBA have a history of over-forecasting growth (probably to keep the inflation estimate from collapsing), then simply mark-to-market (down) each SMP. In an easing environment, you lower the bar for easing significantly when forecasts remain too high. GDP in the next SMP has to come down again as we hurtle toward mid-1s … and that’s below their reduced forecasts, which were based on 50bps of easing over 6mths or so … just check what they need on a quarterly basis to reach the end-19 f/c (an average above 0.75% for Q’s 2 thru 4 …)

2. Using those 50bps like he’s a 15yr old coughing up a secret has set the scene for more easing, even this year, despite ‘other’ policy action. The tradition continues – now the Aug SMP will have to be changed, and the market still has cuts in the profile … therefore, the RBA does too.

3. Lowe is now trotting out ‘if needed’ like he’s on retainer. If you’re like me and think, yeah, it’ll be needed, it’s easy at one level to just take it for granted that he may wish to give fiscal policy a chance, but ultimately will have to cut anyway. On another level, what on earth is he talking about?? If needed? Was the July cut needed? Based on what? The ‘support’ he’s been talking about? It had only been a month since the last cut. What more had he gleaned from his rigorous scrutiny of the data (having been impervious to it before)? Couldn’t have been the labour market. We haven’t even had the next data print. He’s clearly not averse to waiting. Maybe the penny really has dropped.

I totally agree. If you have spent any time modelling you know that variables like the NAIRU don’t just collapse 50bps due to one WPI print.

It is amazing how they are just getting a pass on this stuff.

those table are a mash, soz

It’s okay. I see your point crystal clear. The RBA assumed one in August and say one in November. And Lowe keeps saying the May forecasts look good — so why bring it forward to June and July. I think it makes May look political.