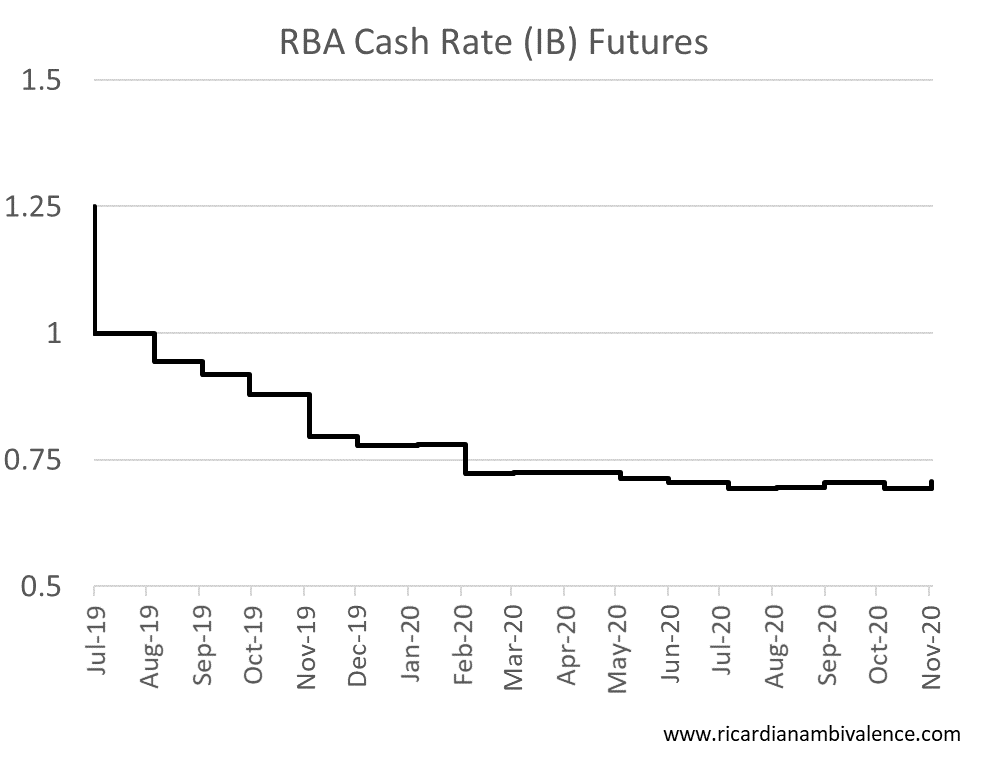

I was wrong again … the RBA cut their policy rate 25bps to 1% today. This is only the 13th time in the last 30yrs that they have cut back-to-back (13/47).

What’s the lesson from all this?

My main take-away is that Gov Lowe is a direct and practical person. His comments are intended in a straight-forward way: so when he says that “the possibility of lower rates remains on the table” he probably means he’s cutting next meeting, unless some surprise knocks him off course.

In hindsight, I should have put more weight on the fact that he said that rates would fall further in the post-meeting speech on 4 June.

… it is not unreasonable to expect a lower cash rate. Our latest set of forecasts were prepared on the assumption that the cash rate would follow the path implied by market pricing, which was for the cash rate to be around 1 per cent by the end of the year.

RBA Gov Lowe, Today’s Reduction in the Cash Rate, 4 June

Notably, there was no similar language in today’s post meeting statement — or the speech.

Both the post meeting statement and the speech rates could still be lowered if needed. That statement concluded:

Today’s decision to lower the cash rate will help make further inroads into the spare capacity in the economy. It will assist with faster progress in reducing unemployment and achieve more assured progress towards the inflation target. The Board will continue to monitor developments in the labour market closely and adjust monetary policy if needed to support sustainable growth in the economy and the achievement of the inflation target over time.

Gov Lowe, 2 July post-meeting statement

… and the Darwin speech concluded with:

We need to remember that the central scenario for both the global and Australian economies is still for reasonable growth, low unemployment and low and stable inflation. As I discussed a few moments ago, there are a number of developments that are providing support to the Australian economy. So we will be closely monitoring how things evolve over coming months. Given the circumstances, the Board is prepared to adjust interest rates again if needed to get us closer to full employment and achieve the inflation target in a way that supports the collective welfare of all Australians, including those who call the Northern Territory home.

RBA Gov Lowe, Remarks at Darwin Community Dinner , 2 July

So the RBA is now in wait and see mode… watching the labour market.

While I have my reservations about the RBA’s forecasts, there’s no doubt that there are some notable positives in sight.

1/ Tax cuts: It now seems almost certain that the Government’s tax bill will pass the Senate this week. So ~10mil taxpayers will get an extra 1k in their refunds. Will people spend it or save it? Things aren’t so bad right now, so my guess is that we see a savings rate that’s much less than the ~50% in the GFC cash-splash.

2/ Terms of trade: The Iron Ore bonanza looks like it may deliver a surplus in 2018/19, and could add more than 10bn to the top line in 2019/20. This will allow the Federal Government to use money (for infrastructure?) to purchase micro-economic (structural) reforms from the States. With demand now playing a role in higher prices, we may even see some modest investment in new capacity.

3/ Housing : If the relationship between auction clearance rates and prices holds, we are already at levels associated with slowly rising prices (in Sydney and Melbourne). A further rate cut should help the market rally. So the suck from the negative wealth effect should fade.

I would prefer infrastructure spending along the lines advocated by Infrastructure Australia.in their priority list.

I just don’t see monetary policy doing much now

the problem is that it takes so long to start. particularly for the federal government, which is mostly an admin and transfer organisation. they don’t do capex well. states do capex — but states don’t have the tax base to support counter-cyclical policy. so the problem is how to get the cash to the states. might as well purchase some reform!

Infrastructure Australia has a prioritised list.

I guess another problem of lower interest rates is that it may lead to higher asset prices rather than activity.

In essence lower interest rates can really only increase housing activity which then leads to increased activity in other sectors.

Infrastructure Australia have 34 projects would would allow the econmy to lift and boost productivity.

Let them judge. Keynes rules again

I should add I have linked t your article so in my owm modest way you may gain more readers. I hope so given the quality of output you produce.

I find it interesting that you and the Kouk are agreeing more often these days

That’s okay mate. I enjoy our interactions and your support

Just a thought on housing,

Apartments is where the action is and who would build an apartment today or even next year.

This surely must have an impact on any housing recovery

True. But the wealth effect can still work if established house prices rise.