The RBA’s Q1 SOMP is an odd document. It is odd for two reasons: it breaks my policy rule of thumb (the RBA moves rates when they move their forecasts), and it contains an odd tension between optimism and reporting on the data — so much so that it might have been written by completely different authors.

For basically the entire time I have been watching the RBA, they have been a fairly plain-speaking central bank. Perhaps due to the luxury of a floating rate mortgage market, the RBA has simply told it straight and moved rates when the world changed.

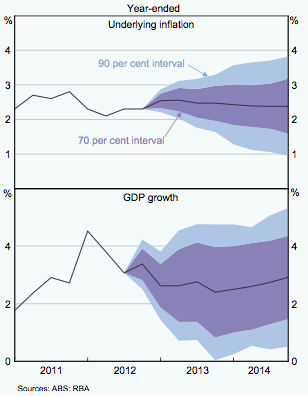

This seems to have changed in the Q1 SOMP — the RBA lowered both their growth and inflation forecasts, but they did not move their policy rate at the proximate meeting (in this case February 2013).

As a result, we are now in an unusual place: the RBA forecasts below trend growth and sub-target inflation for most of the projection period. Admittedly, these are not very large ‘misses’ just now — however given the weakness of many current indicators and the ever-present downside risks to the forecast, I am surprised that the RBA is happy to run with the risk of sub 2% inflation exceeding the risk of over 3% inflation.

Indeed, due to the fact that growth is sub-trend, we actually see inflation trending down slightly across the projection period.

The RBA sees all the risks i see — but they don’t worry about them like i do … the difficult question is: why?

Liaison has told them that the increase in the Iron Ore price is not flowing through to activity:

The sharp increase in the price of iron ore in recent months does not appear to have materially affected investment plans to date, in part because the general expectation is that prices will not be sustained at these levels.

They see the broad based weakening of business conditions, and the decline in both mining and non-mining investment intentions …

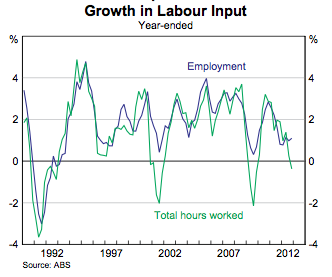

They see the recessionary state of labour demand …

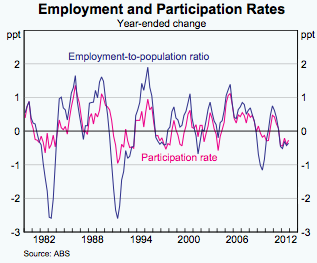

They can see that odd movements in the participation rate are hiding the slack in the labour market …

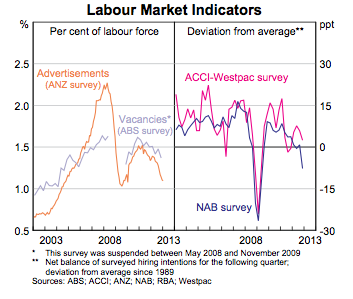

They see the ongoing weakness in the leading indicators of labour demand …

They see the ongoing weakness in the leading indicators of labour demand …

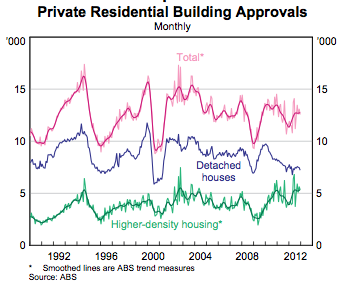

And they can see residential investment is struggling to gain traction despite 175bps of rate cuts …

But still they do not sound all that dovish on rates … Why?

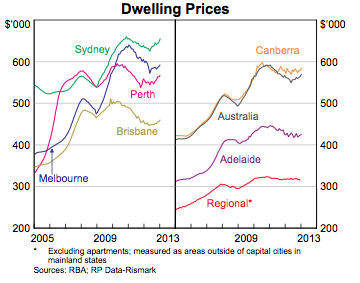

The answer seems to be rising house prices …

House prices are going up, and what we know from experience is that rising house prices tend to boost short term demand (of course, they also may create other problems down the track — which perhaps the RBA would also like to avoid).

Rising house prices tend to boost consumption via a wealth effect. Also, as the expected cost of carrying development inventory declines, rising house prices also tend to boost housing investment.

These are two of the elements of demand that have been weak for some time, and it seems that the RBA has decided to pause for a moment to see if this is a turning point for these sources of demand or if they will remain weak.

This still leaves the question of timing unanswered — the same trends were fairly clear in Q4, so why cut in October and December?

Here I have a less satisfying answer — there are hints of a material change in external demand in the Q4 export data, and the prospective improvement in external demand gives the RBA time to see if the easing they have delivered to date will continue to work its way through the financial space, and also to gauge the extent to which higher financial wealth might eventually seep into higher real demand (there must be a few savers who are still well behind on their retirement plans relative to 2007).

This does not require two authors … but there is a lot of tension between the optimism surrounding house prices and the reality of the bulk of domestic data. Pretty much everything else in the domestic data-set remains weak-to-flat (even the house building data).

The bottom line — the RBA seems a little further from a rate cut than i had imagined. Not because they don’t see the weakness i worry about — for they do — but because they have a little more hope than i do that the rate cuts they have delivered so far will boost demand via a wealth effect (one of the classic channels of monetary policy, and one that has been basically missing for the past 175bps).

The increase in house prices to date is largely a Sydney story. Feb 23 is the first major auction weekend in Melbourne, the biggest auction market in Australia. Anything less than a true 70% clearance rate should send alarm bells ringing.

What I find so surprising is how cautious the RBA is compared to how they were during the GFC. They seem preoccupied with avoiding their mistake between 2006 and 2008. But the hours worked data you highlight in particular looks dire.

Perhaps they think that the wealth effect is sufficiently strong … But i doubt it myself.

Level targeting? Are they happy to let NGDP slip lower to make up for the overshoot?

Possibly, but seems like a generous interpretation to me. Business and labour market conditions should tell them the overshoot has been more than made up.

two points.

Is monetary policy as potent now as it is in ‘normal’ times? In other words will lower interest rates actually work as usual.

will commodity prices firm up as the RBA believes. They have been caught out on this before.

My feeling is it is better to stimulate too much as it is easy to put up rates if wrong.

I do not think a given level of rates is as stimulatory as it was in the past, but i do think there are rates will will impart an equivalent boost to demand. so yes, i do think that the traditional channels remain open, and that it will work in the ‘normal’ ways, it is just that it is going to start working at lower than usual rates.

You can see it this cycle – things really only started to pick up once cash got below 3.5%

You write: “I am surprised that the RBA is happy to run with the risk of sub 2% inflation exceeding the risk of over 3% inflation.” Around 2% must be the new target while AUD is above parity. Targeting 3% in this climate would be a disaster. High AUD naturally leads to lower inflation which leads to lower rates. RBA can’t fight that. I think the RBA has accepted this and has new targets. Anything else would be “unnatural”.

I also understand their concern on Real Estate, although I do not think the risk will eventuate. Should real estate prices really start accelerating now, they would ruin the master plan. Rates would could no longer be cut, maybe hikes would be needed, dollar would get even higher. No, the plan is to stabilize housing and hope to stimulate construction. So a pause is understandable.

Right now we have Perth real estate price increasing after big drops and while they are at the peak of the mining boom. OK. Let’s not forget GDP there is well ahead trend. Sydney is also doing well, but they never experienced the major increases like other capital cities during 2006-2008. For the rest, it’s more like Rigor Mortis. The wealth effect is not there, because overall volumes are still very low. Transaction numbers are poor. Lots of unsold stock on the market, new home sales record low and most who bought after 2010 are now underwater and can only sell at a nominal loss.

Re shares, it’s unclear how many people missed the latest rally and how much cash waiting for better return is there… that could be the real worry, IMO, more than real estate.

One more thing… :) We do know that cutting rates “frees” money for people that are repaying debt. But it also cuts into the income of savers. When term deposits are at 7%, and your inflation target is 2-3% that is quite inflationary per se. It adds to inflation and inflation expectations. And symmetrically when term deposits start being very close to the inflation rate, they must have a deflationary effect for those people who are not ready / want to move money to more risky investments (surely now a bigger slice compared to pre-GFC). Another reason to consider for a pause in rate cutting.

I can’t see how we will get more dwelling construction with house prices outside Sydney (and to some extent Perth) well off their peaks and only climbing slowly. Prices stabilising at levels where those who bought 3 or even 5 years ago are facing a sizable nominal loss will not stimulate construction.

Yes, I agree. And as discussed before, there’s a lot of catch-up to do for established house prices to make new dwellings prices competitive. But on the other hand, the RBA would not want house prices to get bubbly again. So it’s a dilemma. Can Australia only stimulate construction demand only with “bubbly” conditions? Does that mean we have built too much? That’s what inflation does to you, new stuff becomes unaffordable, and you only buy if you know prices keep going up.

Just released, Housing Finance was actually down in Dec.

http://www.abs.gov.au/ausstats/abs@.nsf/Latestproducts/5609.0Main Features2Dec 2012?opendocument&tabname=Summary&prodno=5609.0&issue=Dec 2012

A ray of hope: “Purchase of new dwellings actually up”, but “Number of Owner Occupied Dwellings Financed Excluding Refinancing” is still going nowhere, and that is the vast majority of transactions.

Funnily enough, just after the housing finance release, the ASX200 jumped, as if saying: the only place to make money right now is shares (cash and property are no good options just now).

If FHB are a leading indicator of the housing market (without them upgraders can’t upgrade) then these graphs can’t be good….

http://www.macrobusiness.com.au/2013/02/first-home-buyer-strike-intensifies/

but hey, the housing market is apparently on fire according to ….

Terry McCrann is now saying the RBA may look to hike rates soon. CJ was way ahead of the gloomers on this. http://www.heraldsun.com.au/business/terry-mccranns-column/the-forces-keeping-a-lid-on-inflation-may-be-about-to-shift/story-e6frfig6-1226575708351

While there is no doubt that the two forces TM identified are waning (supermarket competition and currency led declines in the prices of high value added Manufactured goods), some others are waxing — the NAB survey today shows very weak employment intentions, wage pressure, and the lowest level of capacity utilisation in over a decade.

You would have to have an odd inflation model to see rising inflation risk given these facts.

Today’s consumer confidence number was the first data point that goes against an upcoming rate cut. Although it is mostly due to the raising share market and info on house prices stabilizing, could it develop into something bigger? After an awful second half 2012, in January data seems to be better. JB HiFi results also mentioned a January rebound in sales.

I think the rise mostly captures the easing of financial conditions — which we already knew about. As you point out, it is probably about asset prices. I think it buys time to wait and see.

Perhaps the next window is Q2.

Yes, I agree… unless we get some unexpected data between now and the March meeting (capex?), March is no cut now. The next labour release is scheduled for after the March meeting anyway. I am holding on my long ASX200 over AUD, but …. things are getting less clear now…

Rajat, re getting more dwelling construction going …. how can we stimulate more construction if we can’t even sell what’s already built?????

Easy – higher dwelling prices!

The recent equity market action is pretty impressive. Maybe it will allow the RBA to hold off. I wouldn’t be a market monetarist if I didn’t think the markets had useful things to say. I just don’t see much regret in cutting again in March given all the other dataflow we have seen. The direct wealth effect from equities may be muted because (1) not many people at the moment have a lot of their wealth in equities and (2) the government’s super tax kite-flying is probably not helping things. That said, the indirect effect from the bull market may be significant, to the extent it leads to improved confidence and spending even from those without much in shares.

We need credit growth for house prices and transactions to go up, we’ll see.

It does not look like real estate buyers are much “in the mood” …

The difference between share market and housing is simple: the share market had already paid its price during the GFC, and it is simply now recovering. We are now back where we were two years ago, and still well down from pre-GFC peak. But housing… housing never had a real collapse, and it’s definitely not a bargain. If there were bargains in property I’d be a buyer. I think housing will be consolidating around these prices for the medium term. cheers

I’m not saying house prices should go up for any fundamental or technical reason. You asked me how we will get more dwelling construction going when there is considerable unsold stock and I said it would take higher (established dwelling) prices to make new construction more attractive. My point is that if the RBA wants to facilitate a smooth transition from non-mining investment to other sectors, then it will need higher house prices and the only way to get that is either through a continued exogenous boost to confidence from higher equity prices or through looser monetary policy.

The other option is that spending doesn’t go to housing but to retail/consumption (only). That seems unlikely to me. Consumption tends to be fairly stable and does not drive cycles. Stuff is cheap and everyone has too much of it. Sumner has a terrific post where he borrows from George Carlin to explain that a home is a place to “put all your stuff”, so more stuff means more housing. Alternatively, maybe retail spending will go to services, like restaurants and housekeeping, etc. There is definitely a secular trend in this direction due to increasing labour specialisation. But can a shift to more of this happen suddenly and strongly enough to avert a slowdown? And is the reason people don’t eat out more lack of funds or lack of time/organisation?

I understand what you’re saying about house prices and it does make sense. However RBA may be face the impossibility of lowering rates much further to stimulate housing if it wants to keep inflation in the agreed range. House prices exploded in 2005-2007 and 2009, maybe then the RBA should have had rates much higher then, especially during 2005-2007. I see most economist reckon nominal GDP will be below trend in the next 2 years which it is also my view, but it will depend a lot on AUD. If AUD drops we can go back to the way “it used to be”. I would not be surprised if most people will keep favoring saving and repaying debt over new debt in the medium term.

The very fact that Mirvac and Stockland are writing down asset values is of great significance. They would not do that if they forecasted a significant recovery in residential prices. And they should be pretty much “in the know” and demand for those assets at these price must be about zero.