Q4’12 GDP came in bang on the median expectation of +0.6%q/q 93.1%y/y), however it was a little lower than the RBA’s Q1’13 SOMP forecast of +3.5%y/y, and a little lower than the pre-release whisper numbers of 0.8%q/q (folks saw upside risk following public demand).

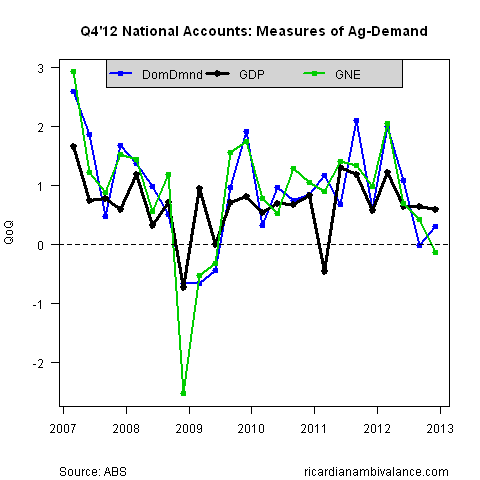

The quarterly story in the data was all about a hand-over from domestic demand to foreign demand. This is likely to be the story for some time. In quarterly terms, demand came mostly from net exports (+60bps) and public demand (+110bps), with Household consumption adding a modest 10bps; private capex subtracted 90bps, and a slower inventory build subtracted 40bps.

A part of this is bogus — the large public capex and weak private capex number partly reflect a transfer from the private to public sector.

Overall, I think it’s more helpful to think in terms of the aggregates — quarterly accounts are always noisy. Let’s frame it in terms of:

Income (Y) = (C)onsumption + (I)nvestment + (G)ovt + e(X)ports – i(M)ports

Taking the first three terms (C+I+G) we saw domestic demand growth of 0.3%q/q (~1.25% AR), which is a slight improvement on the donut in Q3’12. Adding inventories (which makes GNE) we saw a modest contraction of -0.1%q/q (~ -0.5% AR). Adding in net exports (which gets us back to GDP), we get the +0.6%q/q headline number (~2.4% AR).

I prefer 2Q annualised rates to smooth the volatility. On this basis, the transition that’s underway is clear — after driving growth at the start of the mining boom, domestic demand is now weak. This reflects a move from the investment stage of the mining boom to the net export phase of the mining boom.

Does it matter?

Depends how linked into the economy you think the export and import sectors are. In Australia, we export mostly farm and mining goods. Neither employs many people in the operation phase, but mining does in the expansion phase.

Has that expansion phase ended? It’s too soon to tell.

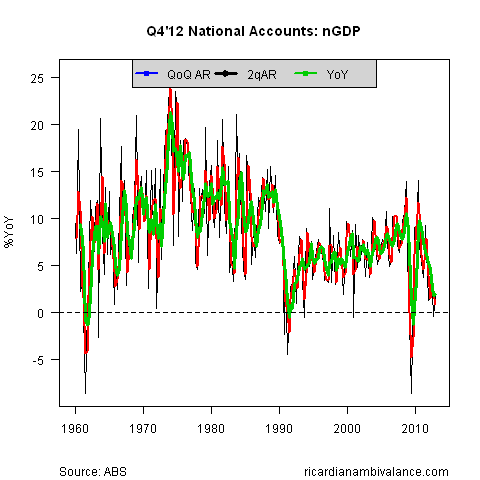

What’s not too soon to tell is that the nominal economy is basically in recession. It grew by 0.5%q/q in Q4’12, up from -0.1%q/q in Q3’12. That takes the 2q AR and YoY pace to ~0.75%.

As you can see from the above chart, it really does only get worse than this in a actual recession.

The weakness of the nominal economy is why i think that inflation will remain low, and why i think it’s way too early to talk about rate hikes.

“What’s not too soon to tell is that the nominal economy is basically in recession… it really does only get worse than this in a actual recession.”

Funny you say that, because ECRI have doubled down on their recession call in this slide pack. After observing that US NGDP is down to 3.5% yoy, they say:

“Based on the full 65 years of historical data, nominal GDP growth of less than 3.7%… has always occurred in a recessionary context – without exception.”

So does this apply to Australia too?

We are not in an activity recession — but the nominal side will be weak, which means weak profit and tax revenue growth, and low inflation.

It is possible that we will get weak nominal growth and low domestic demand but trend GDP as mining investment becomes export volumes. This is a low inflation mix.

Should we be satisfied with trend GDP growth if growth is becoming driven by exports, which are not too labour intensive and hence impose few inflation pressures? We should be able to enjoy above-trend growth under such circumstances.

Agreed.

Hmm … Fits with the inflation data. I don’t see a recesssion in the US data just now — for the outlook it is a question of if the equity and financial market price action /easing can boost real activity. Some folks say recoveries are first mace in the equity market. I am not so sure … We shall see.

U.S. Recession Began Middle of 2012, Achuthan says:

http://www.bloomberg.com/video/u-s-recession-began-middle-of-2012-achuthan-says-w1RsvrcETIGv~p1LSvwIIg.html

Hmm … If you can’t get it right, re-define it?

I would be willing to bet a tidy sum that the nber never dates a recession over h2

Me too. And neither in 2013.

great post Ricardo. i thought chris joyce’s arguments in AFR on the CLF and illiquidity vs insolvency, which is something youve discussed here before, were worth highlighting…seems the RBA does not understand the difference…

http://www.afr.com/p/blogs/christopher_joye/rba_opens_pandora_crisis_line_GFp5R62vJOSDAt0YCJqH5K

http://www.afr.com/p/blogs/christopher_joye/rba_quietly_increases_banks_bailout_ksLcB6WlebkzfQ89p3pPAK

Thanks, i enjoyed this note. Chris and I have gone back and forth on this topic before. Perhaps i might put forth a reply.

Damn,

Can only agree.

yep i agree with Joyeboy on this one too. altho wld be v interested in old Ricardo’s views as i think he is one of the few that can go toe to toe with the big fella

you have made it again.

Thanks!

More GDP graphs:

http://grogsgamut.blogspot.com.au/2013/03/gdpaustralias-economy-grows-by-31-in.html

If residential house prices keep going like in this last quarter (I can’t believe how much shares prices and housing prices are related) no more cuts, sirs. Which will push the AUD higher, even if iron ore eases and lower the term of trade.