Looking at the detail of Q1’13 CPI, inflation does look low — but CPI is very lagged to the cycle, so I’m not convinced it will make the RBA cut in May (though it lowers the bar for an easing); for more on policy see this post.

The rest of this post is a review of the CPI in charts.

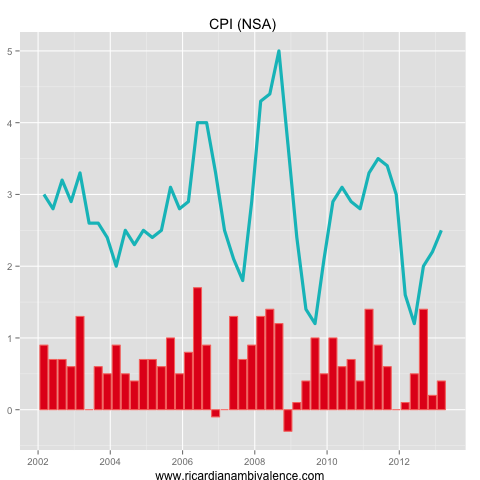

CPI was 0.4%q/q in Q1, taking the YoY pace of inflation to 2.5%. That is exactly the mid-point of the RBA’s 2% to 3% band, however (according to the Treasury modeling) there is ~70bps of carbon price in there, so the true pace of inflation is likely to be somewhat lower.

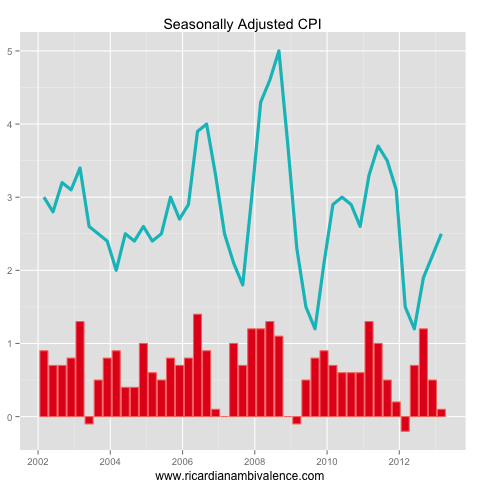

Also muddying things is that Q1 is a seasonally high inflation quarter. Taking out the seasonality puts Q1 CPI at 0.1%q/q (but leaves the YoY pace unchanged).

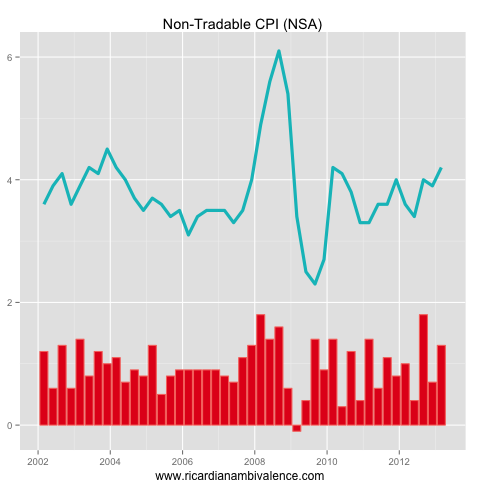

As has been the case for many years (and should be the case when you have a terms of trade boom) the tradable sector continues to have a deflationary impact on the level of prices. Prices fell 1.2%q/q to be 0.2% lower over the year.

The corollary of this is that the non-tradable sector should inflate. This is also occurring. Non-tradable inflation was 1.3%q/q, to take YoY non-tradable inflation to 4.2%y/y. Again, a good portion of this is the carbon tax. Seasonally adjusting at the aggregate level suggests that non-tradable inflation was ~1%q/q in the quarter. That’s probably a bit too high.

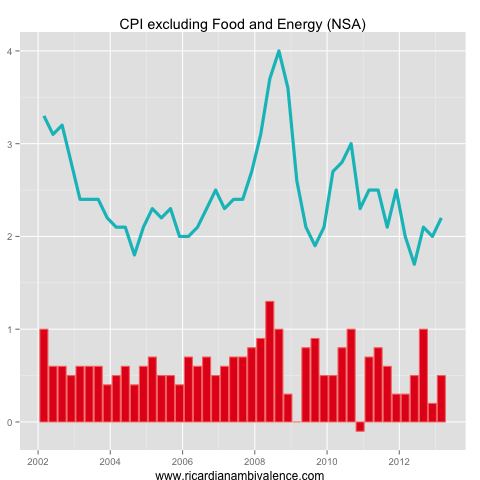

Of course the various exclusion measures are the policy relevant indicators. The RBA’s preferred QoQ measure is the trimmed mean. At 0.3%q/q it is very low. The YoY pace is 2.2%y/y, however about 25bps of that is carbon, so through-the-year core inflation is ~2%. That is also around where inflation for the last two quarters annualised (~1.8%).

An interesting thing is happening to the distribution of inflation. The left hand tail of the distribution is getting stretched out. As a result, the mean is a long way below the median just now. Weighted median CPI was a more ‘normal’ 0.5%q/q in Q1’13, taking the YoY pace to 2.6% (and the 2q AR to ~2.2%).

The problem with these measures is that you cannot explain them to your mum (unless she’s an economist!). The US-style exclusion measure is therefore a handy reference — and at 2.2%y/y (the NSA QoQ was 0.5%q/q) it is basically in line with the median CPI measure.

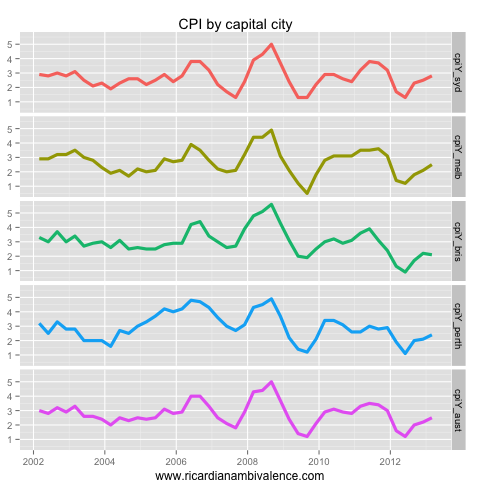

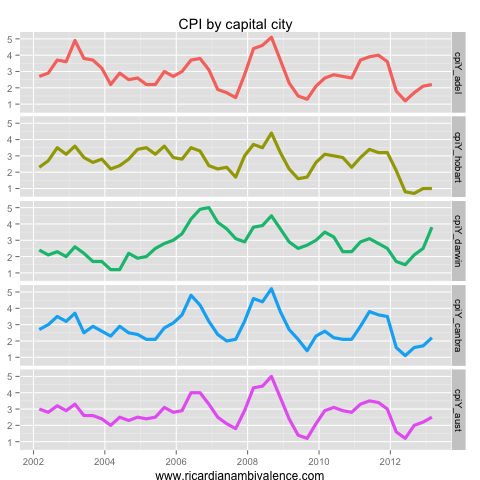

Looking around the capital cities, I find the split very interesting.

Among the big four capitals, Sydney (the most leveraged, and therefore most sensitive to interest rates) has the highest pace of annual inflation: 2.8%. Brisbane is likely to be the most FX sensitive (due to their exposure to Agriculture, Tourism, and coal mining) and inflation there is 2.1%y/y.

In the minnows, the recession in Tasmania seems to be lowering inflation, with annual inflation of 1% clearly behind the rest of the country (Darwin is a booming 3.8%y/y).

Inflation = house prices. The only indicator the RBA must watch for monetary policy is house prices. They did not in 2007 and they got burned.

The inflation vs house prices graph even matches city by city. Which shows the huge role house prices play / have played in our economy.

You have made it.

There are quite a few articles from you also a number further on R&R.

All in all the best weekend blog reading anywhere!

Very kind. Your blog is clearly picking up. I can see it in the referrer links. Well done.

There is quite a bit of very good stuff linked – it is flattering to be in the same group.

RA, your expertise needed here :) Is it historically “normal” to have so much difference between some items that are appreciating quite fast, e.g. mostly services like electricity, health, education, etc. where you could even see a structural inflation problem, and some items depreciating fast e.g. audio and visual, electronics, furniture, clothing, eg. mostly imported stuff. If not normal, how much is this deviating from “normal”?

Good subject for a post: the textbook idea is that as the terms of trade rise, fx appreciates, and domestic / tradable prices rise by more than global / non-tradable prices. When the terms of trade go down, this is supposed to go into reverse — partly due to fx going down.

This is why a rigid labour market is going to be such a poor policy setting (if sustained) if the terms of trade goes down fast and the AUD does not.

Makes sense… then the textbook monetary policy shouldn’t it be not to cut rates further now as this lowish inflation does not seem due to poor demand but rather it is just the result of the ToT ongoing adjustment? If you cut rates now, while the ToT is coming / will come down, all you do is to keep non-tradable high, while instead it should come down and tradable should come up?

Hmm, it is very complex in my mind. It comes down to what you think is going to happen in the labour market.

The ratio of tradable to nontradable prices is a measure of the real exchange rate — as domestic prices rise relative to foreign prices, the real exchange rate rises, which means that (all else equal) monetary conditions tighten. This is appropriate as the boom builds.

Now we have this measure of the REER rising, while the ToT are falling, which means that monetary conditions are tightening even as the economy loses income. Now if the labour market is about to crack – as firms lose competitiveness – and you are sure that wages will adjust down you might cut in advance … But if you are unsure about the outlook you should wait.

I tend to think that the labour market is more rigid – as the aim of recent regulation has been to improve the bargaining power of labor – so i am inclined to wait and see … But it is a tough call.

The current mix – falling terms of trade, inflexible FX, rigid wages, is hard for policy makers. The REER must fall – either via an FX collapse, or lower domestic inflation (which means slow wage growth).

Without confidence about flexible wages, i think they should wait and see – but it is a close call.

I’m not sure about this. It seems a bit odd to me that one form of looser monetary conditions (nominal ER depreciation) is regarded as desirable under the present circumstances whereas another form (lower official interest rates) is not.

I would say that if the ToT is falling but the currency is not, real wages need to fall to maintain internal balance. It’s less clear to me that the REER needs to fall. Real wages could fall via a depreciation, or if domestic prices rise faster than domestic nominal wages. Therefore, I would say loosen monetary policy and even if we have some downward nominal wage stickiness, we should see falling real wages and UnN remaining (or moving closer to) the natural rate.

It’s only if you are worried that labour has sufficient bargaining power to increase nominal wages in line with prices that you would be concerned about doing this. But then if that was the case, you wouldn’t welcome a depreciation either.

Wages are the only real cause of inflation in Australia. So services, for which wages are the major component. The rest of the stuff (mostly imported stuff) is getting cheaper.

We had wages growing about 50% in a few years, while the rest of the world is fighting high levels of unemployment. The goal should be that as the mining boom passes, we regain some of our competitiveness to support other sectors. That includes reducing costs, not increasing them. We will not achieve that by allowing domestic inflation to be considerably higher than imported and wages to keep appreciating much faster than in other nations. The overall CPI is benign yes, but if you look at the internals, domestic costs are still escalating. Is it a good policy to compensate imported deflation (not in the hand of the RBA, since they do not want to control the exchange rate) with higher domestic inflation?

“Is it a good policy to compensate imported deflation… with higher domestic inflation?

If the underlying problem is downward nominal wage stickiness, then I would think so.

Well, if we allow wages and non-tradable inflation to grow at ~4% p.a., then the exchange rate WILL fall, as we are not worth that much, and are becoming absurdly expensive relative to other economies.Maybe that’s your plan.

RA you are far too modest. quality counts

Better to under-promise and …

But thanks mate :)

Ricardo can you please explain what you mean by “The corollary of this is that the non-tradable sector should inflate. This is also occurring. ”

If the exchange rate collapsed leading to a complete reverse of the current tradables deflation, what do you think would happen to non-tradable inflation? Would it deflate enough to offset the inevitable inflation spike on the tradables side?

Price level would rise, but i think tradable goods would rise by more than non tradable goods. This is a good subject for a longer post. I think i will do that this friday.

Great, thanks