One of the biggest traps in Australian economics over the past decade has been worrying about non-tradable inflation. I fell into this trap myself prior to the May 2013 RBA meeting — for reasons which I hope will be apparent in a few minutes.

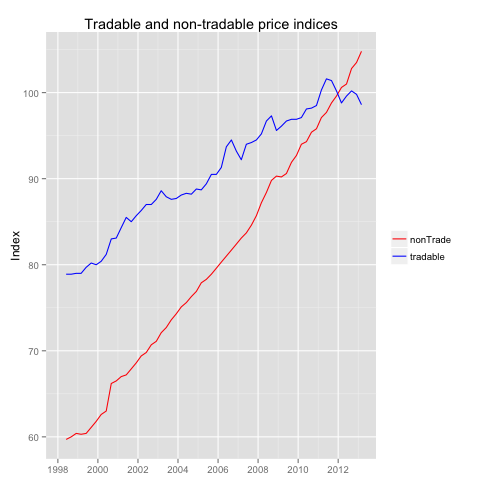

First of all, a re-cap of the facts. Prices pretty much always go up — except for over the last few years where traded goods prices have gone sideways.

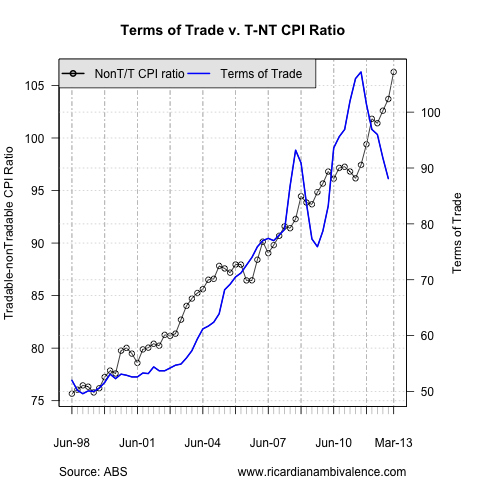

We only have tradable and non-tradable CPI indices back to 1998, but over the early part of this period, non-tradable prices rose a little more quickly, but both tended to accelerate and slow according to some common cycle (the global business cycle).

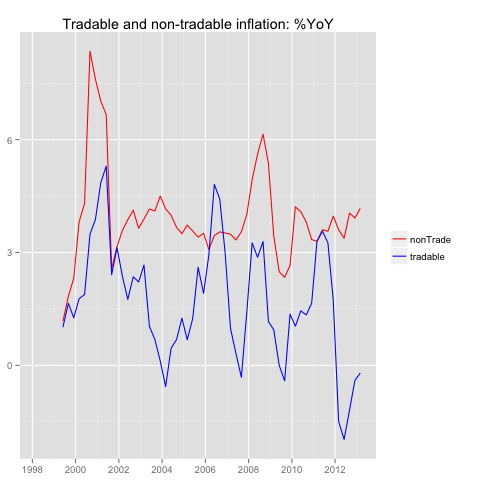

So why should we not worry about non-tradable inflation? After all, it’s tradable inflation that’s holding down CPI, due to FX appreciation and that cannot go on forever?

Well, that’s because a rise in non-tradable prices relative to tradable prices is exactly what the textbook suggests.

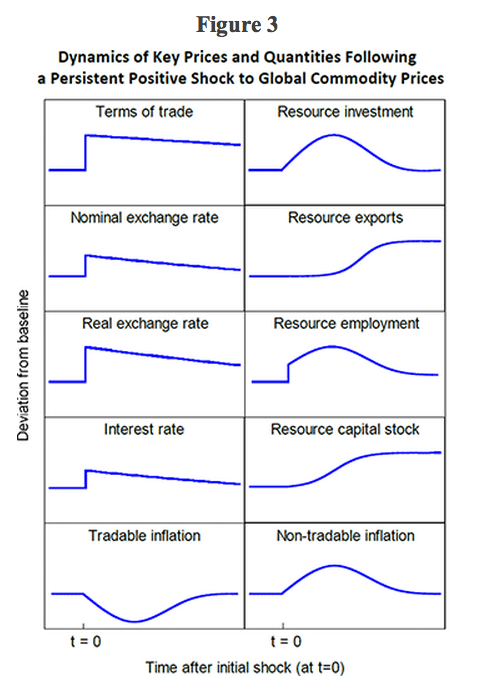

RBA Gov Kent has a nice schema of the text-book dynamics in a speech he gave last year. He shocks mineral prices, and shows the consequences. I have re-produced the chart above.

Taking the ratio of the two lower panels in Gov Kent’s chart, you can see that the ratio of non-tradable prices to tradable prices ought to rise. That’s exactly what we’ve seen since the terms of trade started to rise: non-traded inflation has been higher than traded inflation.

Why does this occur? Because the higher terms of trade means that the prices of tradable goods are lower, and as a result we have more income to purchase non-traded goods and services. More demand means higher prices … just like micro 101.

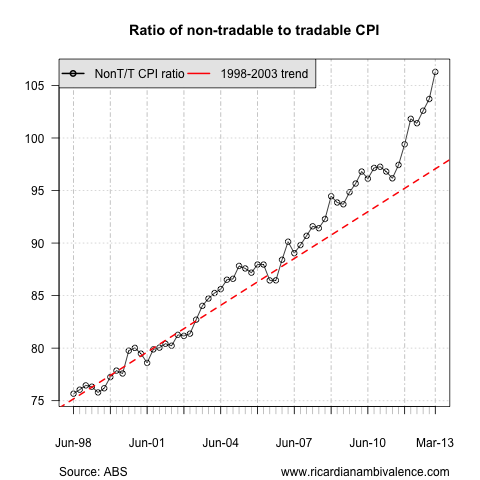

So how does the theory work? Pretty well so far. When we look at the ratio of non-traded to traded prices against the terms of trade, you can see that the increase in the two match closely — up until the last few years.

If the textbook holds on the way down, what we should expect to see is a decline in the exchange rate and a rise in the relative price of tradable goods. This will probably play out as a rise in the real price of traded goods, which lowers real incomes, and therefore lowers demand for non-traded goods.

So why worry now, given that the terms of trade are falling?

Because the price ratio has just snapped in the ‘wrong’ direction, relative to the terms of trade. This is what a competitiveness problem looks like.

If non-traded prices are sticky, we may have trouble keeping a lid on inflation if the exchange rate falls quickly. If this were to occur, the transmission back to balance would be via a long period of higher unemployment (with larger deficits etc).

well done. This is what quality pieces in the blogosphere is all about.

I award you an honorary Krugman award!!

The most interesting line in Kent’s description of that effect is: “the net outcome for demand in the non-tradable sector is not clear a priori.” That seems a bit of CYA for the RBA, which has kept money too tight and allowed non-tradable demand to fall too much since 2010, at least judging by employment growth. But despite weak non-tradable demand, non-tradable inflation has not been so weak. That’s the concern, although my sense is that energy prices (both network charges and carbon) and the curtailing of the PHI rebate could explain a fair bit of the non-tradable increase.

Another thing is that I find it hard to reconcile the magnitude of the larger immediate effect on the real exchange rate compared to the nominal exchange rate in the charts with the charts on inflation. Wages and prices don’t move up immediately, but the real ER chart implies they do.

One thing i have learnt from the last 40 years is that potential inflationary dangers of a depreciating currency are ALWAYS overestimated.

Yes, I agree. Imported prices are also sticky. AUD has appreciated 20% in a few years, but non-tradable prices have not fallen that much. If AUD falls another 10%, would probably be due to a very weak economy (unlikely), so I would not expect non-tradable to jump significantly in that case. The pricing power would just not be there. If AUD falls significantly I’d expect non-tradable to stabilize and tradable to fall, and rates to go even lower.

I messed up tradable and non-tradable …. fixed version:

“Yes, I agree. Imported prices are also sticky. AUD has appreciated 20% in a few years, but tradable prices have not fallen that much. If AUD falls another 10%, would probably be due to a very weak economy (unlikely), so I would not expect tradable to jump significantly in that case. The pricing power would just not be there. If AUD falls significantly I’d expect tradable to stabilize and non-tradable to fall, and rates to go even lower.”

One thing that is very dynamic are petrol prices. That could be inflationary if AUD falls, but it would take demand from other goods and weaken other imported prices. Overall it would be a frag on the economy.

frag = drag

OK time to stop commenting! :)

Agreed.

As Sumner says, “never reason from a price change”. A drop in the AUD is usually – but not in the most recent case – the result of a hit to global demand, which is net contractionary. The recent fall in the dollar was driven by an unanticipated loosening of the RBA’s stance.

But IF the “commodity super-cycle” is peaking and China starts to re-balance growth, we could see the AUD weakening even without any particular hit to global demand (we had an example recently). AUD would no longer be fashionable.

Let’s face it, it’s commodity prices that have helped us not having a recession in 20 years, so our economy now depends a lot on that. Should that eventuate, we’ll see a lower AUD, lower commodity prices, low inflation (both types) and even lower rates. Yes, I think a lower AUD would not bring inflation by itself.

Great post! thanks

Been due for a while :)

Big drop in consumer sentiment – down to 97.6 in May. Looks like the RBA cut was well-timed!

Sure does. Interesting dynamics in the report — good time to buy a house up sharply, presumably on the rate cuts, but overall softer. Folks don’t like deficits, and for good reason as they know it means higher taxes. A bit Ricardian …

From Westpac document: “This latest survey is based on 1200 adults aged 18 years and over, across Australia. It was conducted in the week from 13 May to 18 May 2013. The data have been weighted to reflect Australia’s population distribution.”

Margin of error = huge. Plus how many of those 1200 adults aged 18 years are actually in the market, looking to buy a dwelling. It would be an interesting extra question I think. Or it’s a good time but not for me? :)

Sorry but deficits in good times means higher taxes but deficits in bad times doesn’t!

Well, we already have higher taxes with higher medicare levy, bracket creep, superannuation changes, and no baby bonus no more. It’s just the start!

Overall we are paying less tax!!

Two great papers on the structural side of the budget released today.

I am going to talk about them tomorrow

“Overall we are paying less tax!!” Please explain! :)

just look at the budget papers

Don’t need to really…. I know, myself I’ll be paying more taxes.

Ha!

I and we (Australia) are not the same!

Actually, you fudge — the tax take is down for two reasons, the ngdp / asset price miss, and the changing structure of the corporate sector. For the most part, it is the corporate sector that is paying less tax due to the shift toward mining activity.

Tsy income tax forecasts have been pretty good …

They mucked up the mining tax, so it is folks that are going to pay more. They already are, due to various cut backs (all of which i support regardless of the budget’s state).

Surely you must be referring to Apple ? Yes…. THEY PAY LESS, BUT WE PAY MORE!

No fudge at all Australia as a whole is paying less tax , much less tax