The Australian Treasury has released new structural budget deficit estimates, updating my favourite bulletin article (MacDonald &c.) of the last few years.

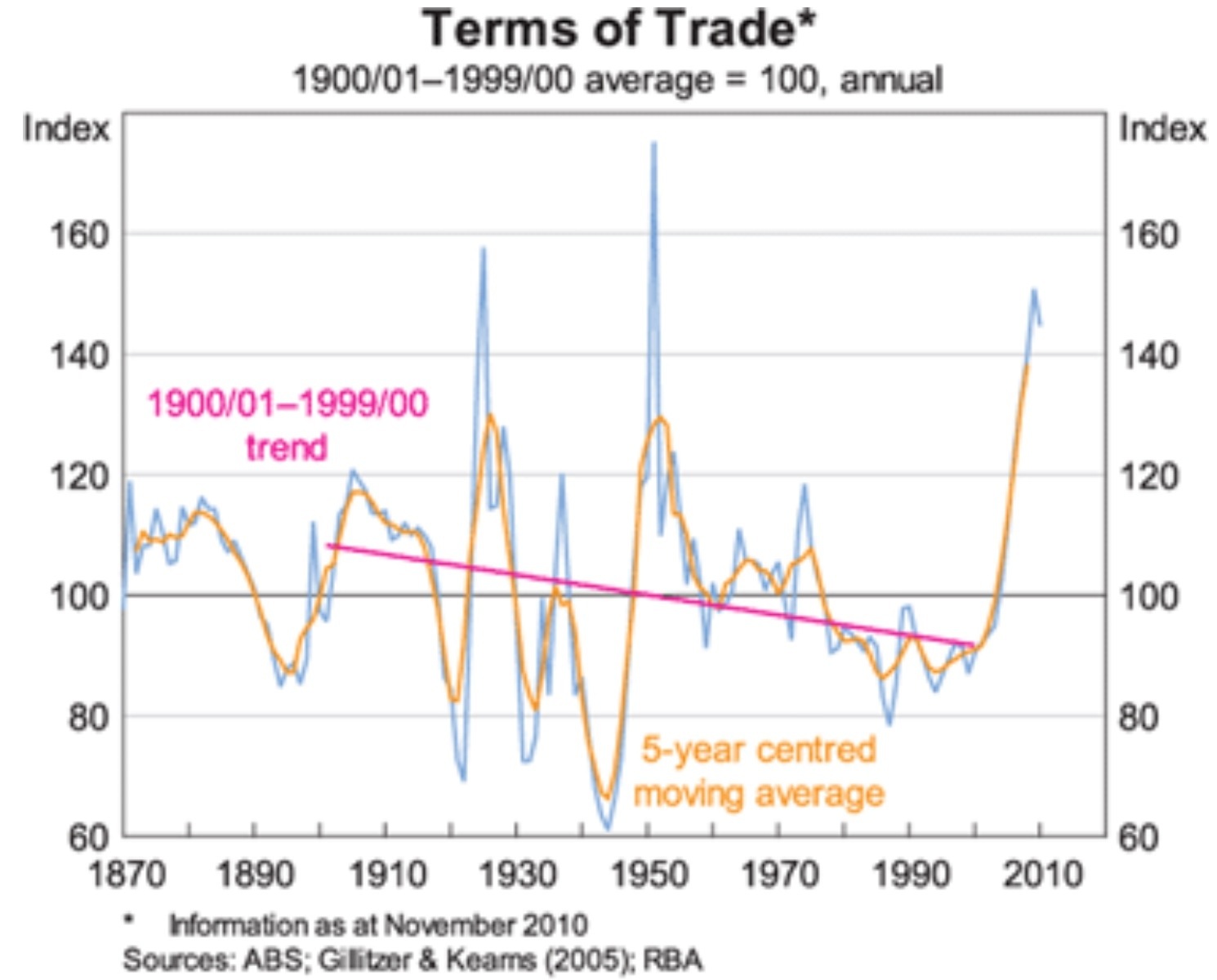

The structural budget deficit is around 1ppt of GDP larger, for each 20ppts we wipe off the terms of trade (in terms of deviation from the long run pre-boom level). This seems fair to me.

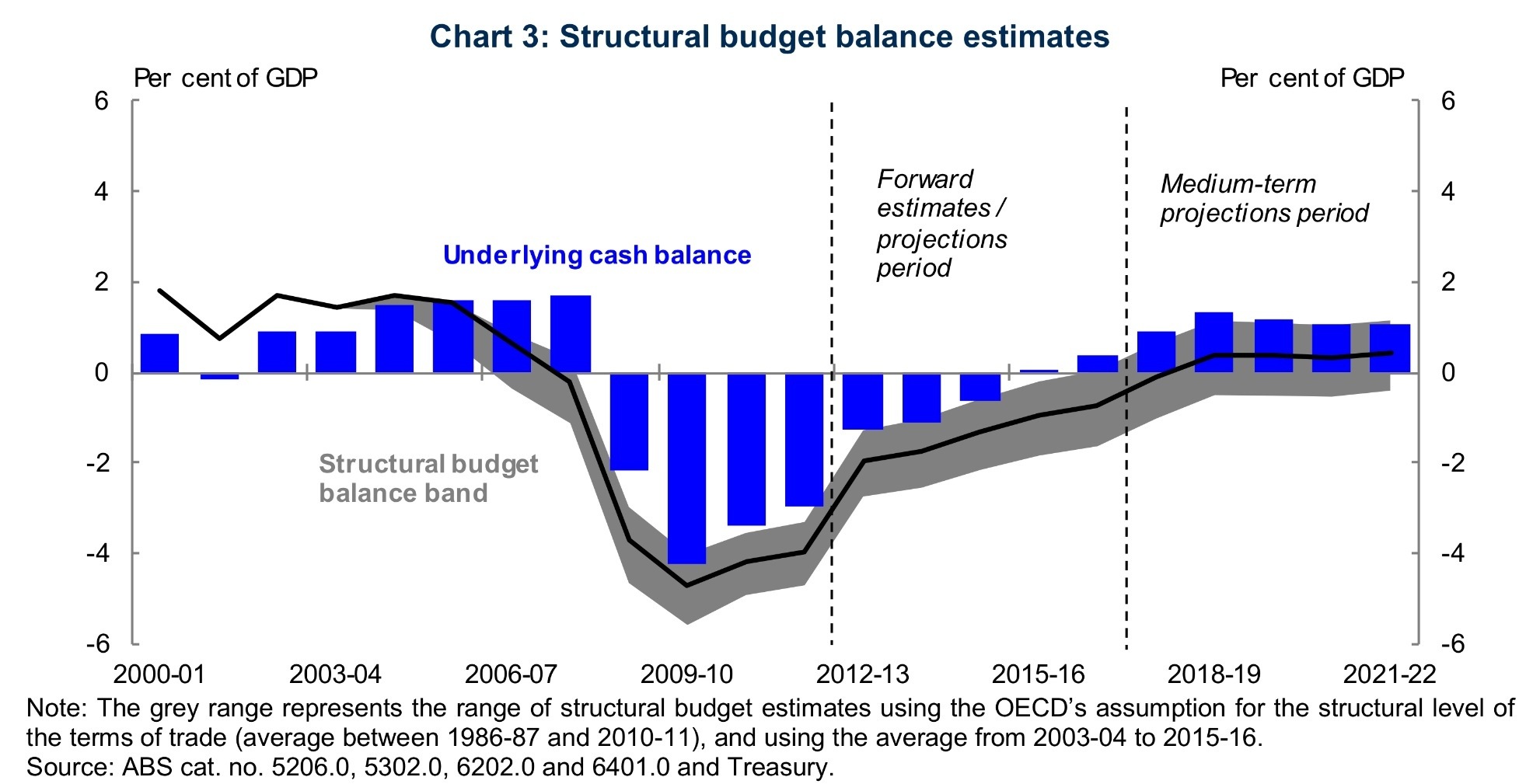

So, while we have a deficit of ~1.1% of GDP forecast for 2013-14, in terms of the underlying cash balance (or 1.5% of GDP using the headline cash balance, which we probably should use given that there is no way the NBN or CEFC are ‘financial investments’ worth book value), the structural position is said to be something like a deficit of ~2% of GDP (the band is 1% to 3%).

The error bands are fair enough in one sense, but i think the way they have positioned them boarders on abuse. The mid point should have been the long run average, and the error bands should have allowed for the true upside and downside cases: some small persistent increase (to reflect resource scarcity) in the terms of trade; and the probability that resources prices would resume their relative price decline, causing the terms of trade to resume their century long trend-decline (which is what RBA Gov Stevens has been warning of)

Instead, the top of the error band is a silly ‘super-cycle’ assumption cooked up by Deloitte-Access Economics. They assume that the terms of trade will sit just below the all time high forever. They may be right, but i bet it is not — and in any case, assuming such good fortune lasts forever is imprudent. The bottom is a reasonable OECD assumption that the terms of trade rests at the 25yr average, or about 10% above the pre-boom average (this would have been my upside case).

We can make a back-of-the envelope adjustment for this – nudging the terms of trade down to the long run average suggests a structural deficit of about 3.75% of GDP in 2012-13 and ~3.5% of GDP in 2013-14.

Any way you cut it, there is a lot of fiscal tightening left to do – and due to the fact that there is no reason to think that nominal GDP will ‘bounce back’ to the prior growth path (as the terms of trade are unlikely to bounce back to prior peaks) it must be done. We can not assume that the deficit will shrink as the economy recovers.

I expect that a long period of tight fiscal policy and low interest rates is ahead of us!

Why is there a necessary link between the ToT and NGDP? Can’t the RBA target 5.5% NGDP even with a falling ToT?

Surw they could, but then they would be targeting export prices – which doesn’t seem that smart to me.

I can think of worse things. Lars Christensen has a post discussing export price pegging for small open economies, based on some previous papers by Jeff Frankel. The main drawback is that such a peg would not automatically respond to velocity shocks.

I am dissappointed no comment or mention of the PBO paper which was peer reviewed.

you neglect to mention the main reason for the deficit and it aint spending

My comment on both papers is here with the obligatory link to this naturally good writeup by RA.

Brief comment

PBO paper is good for lay people whilst the treasury paper is only for economists

I’m not sure about the whole ‘structural budget balance’ concept. If it can only be known in hindsight, then what’s the point? Even now, I would suggest that had the RBA does its job properly over the last 2 years, much of the so-called ‘structural deficit’ would disappear. This is why I think Hockey should be having coffees with Glen Stevens now and floating a change to the RBA’s mandate, before the ToT crashes and the ZLB approaches.

More importantly, commenters (including yourself, NT) have highlighted how the structural balance started deteriorating in 2001/2, due to tax cuts, etc. But isn’t the whole point of a structural measure that diminution of a surplus is not a problem – a structural surplus is a structural surplus – but absolute shifts from surplus to deficit or from small deficit to large deficit are important? Put another way, unlike a (non-structural) cash surplus, there is no virtue in having a large structural surplus because it simply means you are taxing too much.

You want to aim for structural balance. That’s the point of the estimates, really. And sure, as economists, we are forever looking in the tear view mirror!

Could you do me a favour a link the PBO paper as well. That way anyone getting on to this topic from Around the Traps can link to both papers.

I really do not want to put my bit up on ATTs!

You will undoubtedly be the person with the most articles this week!!

Sure, you should link to it in a comment, and i might make a review in another note – else i will make an edit.

AUD currently testing your 96.70 again …. Last night I watched Bernanke on TV, and it’s clear he is suffering from bipolar monetary disorder.

I link it in my comment at my place!! I also link this article!!

but Here it is!!

Rajat the only point in having a large structural surplus is to offset say a commodity boom or you need to pay off large public debt. Neither are relevant here.

I agree. What I’m getting at is that the commentariat seem to be suggesting that the rot started with Howard and Costello. My point is that they are confusing structural with cash balances.

I happen to agree with this — the rot did start with Costello. The baby bonus budget was the start of the nonsense.

A surplus to offset a commodity boom would not be structural.

So we were talking recently about govt malinvestment…. the car industry a classic example of it unfortunately. Now it looks like they are going …. Holden next…. and obviously we think about all the money spent to support a dying industry, that was short sighted (although in the short term it was all about defending Australian Jobs govt would say!). Short-termism.

When you listen to the Ford boss in Australia mention that production costs in Australia are DOUBLE the costs in Europe and 4 TIMES the costs in Asia, then one starts understanding why it’s a problem that non-tradable inflation has been running at 4% p.a. for a decade, salaries are growing at the same rate too and AUD has appreciated 30% in a few years. Here is a list of FORD factories, in places that are now obviously much more competitive than Australia: http://en.wikipedia.org/wiki/List_of_Ford_factories

Yep, total waste. Never good to see someone lose their job, but it is also a great shame to trap someone into a dead industry. The money is much better spent on training than subsidising poor quality cars.

It has mostly to do with Taxes in particular cutting personal income taxes in the belief company taxes would keep rolling in!

Yes, but the chart shows that cutting personal tax was fine up until 2006/07 inclusive. It was only the 07/08 and subsequent cuts that swung the structural budget into deficit.

In any case, on the politics of it, I think Judith Sloan and others (including Costello himself) have made the valid point that the notion that the government (Liberal let alone Labor) could have resisted pressures to spend ever-mounting surpluses is pretty fanciful. Better the cash was returned to taxpayers than getting ‘invested’ in more white elephants or fattening up public sector/subsidised pay packets.

Sure does – but what’s your point? Rudd and co could have objected at the 2007 election

No with a commodity boom you have larger surpluses.

Cutting taxes was simply adding to inflationary pressures in an economy at full capacity.

The problem of taxes once the GFC hit was readily apparent.

did any of you see the example of Ireland Treasury showed

But doesn’t the structural measure account for the commodity boom? So with a commodity boom, you should get larger cash surplus but no change in the structural position? What I am saying is that it was entirely appropriate to cut taxes for so long as the structural budget was in surplus (to the extent you have faith in these measures, which I don’t).

Cutting taxes did add to inflationary pressures, but that is the RBA’s job to manage, not the government’s. Just as now, it is the RBA’s job to manage low inflation and NGDP; it is not a reason for the government not to quit wasteful spending. Fiscal policy is about getting the supply side right, not stabilising demand. Even your mate Krugman accepts that activist fiscal policy has no role outside a ZLB world.

100% agree.

You are incorrect. Keynesian policy demands greater fiscal stringency in VERY VERY good times.

It is merely the mirror image of using fiscal policy in very very bad times.

This is possibly the best piece on what Keynesianism really is.

I agree with Quiggin’s short term prescription. The rest is a utopian stream of consciousness about how one could in theory save the Eurozone if human nature were somehow different.

Keynesian policy is perfect on paper, just like Marxism!

But in the real world…. public institutions may be corrupt and may not spend the money for the common good. I give you an example: do you know that the exact same syringe costs double for some of the local health authorities in the South of Italy compared to the North of Italy? Ask yourself why. Then a good administrator came in and just slashed the budget by 50% and guess what? It worked! Now prices are aligned. Do you know that there are thousands of people receiving invalidity payments, while they actually are NOT invalid. And there’s people still receiving pension payments while they are actually dead (their families do). Do you know tax evasion in Italy is double the tax evasion of Germany. And Keynesian are still preaching MORE spending for those same people that are corrupt and with no credibility? To solve this problems you actually CUT the money, not increase it. Keynesian want to postpone addressing the real problem, let’s survive a few more years. It’s like suggesting to give an overdose of heroin to a heroin addict, just because otherwise the pain is too much to take right now. Wake up! These are structural issues that must be addressed with very hard measures, not a soft hand.

But it never happens. Keynes is trotted out by those that love big govt in times of weak demand, and then the economy is always too weak to tighten in the recovery. That’s what happened in europe, and what we see and hear in Australia just now.

RA that is complete cobblers.

Keynes only approved fiscal stimuli that was temporary. big government needs permanent increases.

Just what countries in Europe are you talking about. Prior to the GFC they should have almost all has surpluses. Some such as Ireland and Spain actually did.

Given that nominal GDP here is well below trend that is entirely the correct view and your view is incorrect!

Unless you are a commodity super-cyclist, there is no reason to think the gdp deflator will ‘recover’. That is the essence of the structural adjustment for the terms of trade.

ngdp need not bounce – we could all just get lower incomes due to an export price drop.

Real growth is around trend, and the unemployment rate is low, which means that there is scope for tightening. Better now than later when the market forces the issue.

Re Europe – some had surpluses after a massive boom. I should have thought all would have!

Don’t you understand that surplus or deficit does not matter when the money that is spent is actually wasted? Your economic theories require a system that actually works…. Here you go, just the tip of the iceberg, then let me know how your Keynesian policy will work in Giarre.

http://www.businessweek.com/articles/2012-10-04/sicily-a-portrait-of-italian-dysfunction

A little jem: “All governments get called upon to tackle unemployment. In Sicily, the solution was to create jobs by fiat. The regional government directly employs some 18,000 workers, five times as many as the region of Lombardy, around Milan, which has twice Sicily’s population. In addition, regional and municipal governments employ tens of thousands of workers on short-term contracts. The city of Palermo alone has 20,000 public workers. The region also funds about 8,000 instructors for professional training programs, which both teachers and students are paid to attend.”

I do believe I did say that about Europe

So you understand now why Germany is pushing for austerity? They are right, it’s the only way to rein in more wasting and cut off the excessive fat. It’s a painful process some European nations will have to go through.

SSEC,

Both Spain and Ireland had surpluses. Italy had a primary surplus. you are talking rot!

Hey RA the PBO link isn’t on yet.

You are not listening…. Italy had a primary surplus, yes, for a minute, and tax money was wasted and wasted and wasted and wasted and wasted until the money has run out completely. Your solution? Waste more! Maybe in Napoli they should have 40k public servant instead of 20k doing nothing, while no one is collecting rubbish from the streets.

Spain inefficiencies are mythical too, the Borboni came to the South of Italy from there. And Ireland had surpluses during the biggest credit bubble ever, it all came down like a house of cards. They went from triple A to bankrupt in a few days!

Italy had a primary surplus, but also large debt to gdp and a nominal growth rate that was only around their financing cost. A primary surplus was necessary to stabilise their debt dynamics.

I have a job – tonight i either write it up or link.

no need to write just link it.

They both say the same thing. The PBO paper is easier to read.