The other part of the Treasury Structural budget estimates working paper is the PBO study — both were published on 22 May.

The PBO paper is extremely similar to the Treasury note — but the charts are uglier (what’s wrong with these people? Even excel can make better charts than this).

There are, however, a few things to commend about the PBO paper — the most prominent being a very good discussion of the terms of trade, and the reasons for the adjustment (starting on page 7).

Their starting chart is a very good one (lifted from Treasury), that shows how unusual the increase in Australia’s terms of trade has been, even against other commodity countries such as NZ and Canada.

This is why the real AUD TWI had to appreciate — and why it did not make sense for the RBA to intervene to hold it down. We could either take the real appreciation as inflation or a higher nominal exchange rate — we made the right choice, inflation is a greater evil.

The second chart shows the excessive optimism of the Treasury forecast — in FY2029-30, the terms of trade will be between the early boom and late boom. Given that our terms of trade appreciate has been around 3x the appreciation of comparable nations, this seems imprudent.

Isn’t the downside risk that the century long decline in the relative price of resources resumes? Iron ore is not scarce and coal could well be replaced by a combination of gas, solar and nuclear in 10yr to 15yrs.

The other valuable part of this report is the technical appendix — here it is valuable for throwing some light on the problems with the estimation strategy. This section also shows how fragile these estimates are (I was in Canberra in 2002-3 and I promise you no one in budget policy thought the Treasury was in a rich structural surplus).

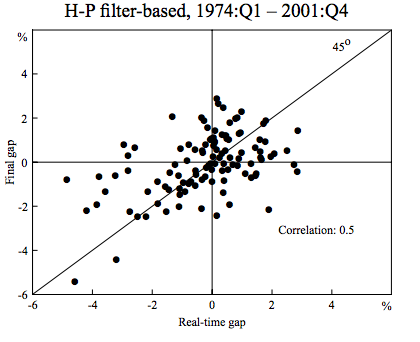

First of all, it’s odd that the PBO uses a Hodrick-Prescott filter for their trend estimation. Serious research (RBA RDP 2002-06) has found that these measures are basically uncorrelated to the actual output gap in real time, so they are not at all useful.

Such output gaps work okay(ish) mid-sample, but are basically useless at endpoints. This deeply flaws the most important use of the work (understanding where we are right now) — but there is hope, as this part of their work can fairly easily be improved.

Such output gaps work okay(ish) mid-sample, but are basically useless at endpoints. This deeply flaws the most important use of the work (understanding where we are right now) — but there is hope, as this part of their work can fairly easily be improved.

This brings me to a final point about the ridiculous structural deficit charade of the last week or so — The Australian Treasurer called for structural estimates on 20 May, and just two days laster the Treasury has an entire working paper and the PBO publish a 28 page study.

Anyone who has worked in the public service knows that sign off on even non-political papers takes longer than a few days. These estimates should be both produced and published as a matter of course — not because they are robust (for they are not) but because they are useful.

I’d sooner have this paper, flawed output gap estimates and all, than none at all.

excellent work, as I entirely expected, but you work on the week-end and get no sleep!!!

you definitely need a life! Watch some Castle episodes!!

“We could either take the real appreciation as inflation or a higher nominal exchange rate — we made the right choice, inflation is a greater evil.”

Maybe we should have limited the boom by assigning fewer licenses to extract minerals. I mean we are “booming” for the benefits of other countries who need our commodities, but the boom could have been managed better. A “boom” is not necessarily good, especially when it finishes. Now we may even face the issue of over-capacity in mining and have allowed the boom to kill other parts of the economy, not necessarily less competitive per se, but definitely less in demand compared to minerals in this specific time.

By the way, it looks like this grand Japanese experiment of doubling the monetary base is completely irresponsible. -7.32% ???? What the hell are they doing here? Playing with people’s money? Unbelievable really. And tomorrow up 10%?

Yeah, it is wild. Perhaps we might ask what they was Bernanke thinking with that tapering mumbo jumbo?

My read is that, under pressure, he got a bit confused and some of his insecurity came out. I see Central Banks as being like a sort of referee, and usually the best referees are the ones that you do not notice during the game. But can’t say that of the fed lately. In the end, for the US it’s good to start talking about tapering and prepare markets for it, even if several months away… what happened yesterday in Japan it’s really what must be avoided in the US in the upcoming months.