The June RBA Statement was basically a return to the situation prior to the surprise cut in May (with fewer words). The bottom line remains that the RBA could cut their policy rate at any meeting — because things must improve.

The statement itself contains fewer words, and few changes in sentiment. There are, however, some notable tweaks to the last two bits: aimed at playing down the decline in the currency, and making their easing bias explicit. My guess remains that the next two cuts will come following the quarterly CPI prints.

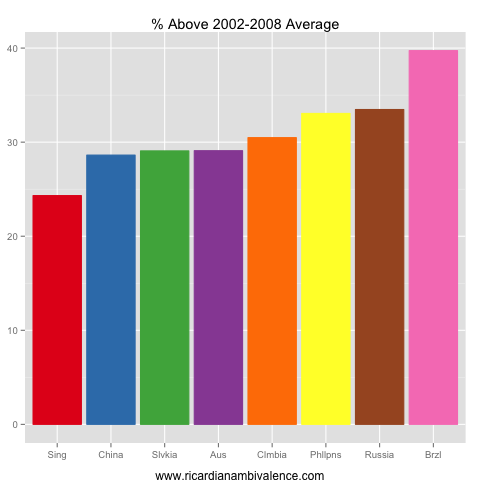

I am surprised at the confusion that surrounds the FX issue — a few months ago, the RBA said that the AUD was over-valued, and cut rates because of it in May. A seven cent decline changes the degree of over-valuation, but not the basic issue … at ~30% higher than the 2002-2008 cycle average, the REER is way too high IF the mining boom is over. We remain at the top of the BIS leader-board for the largest increase in REER this cycle.

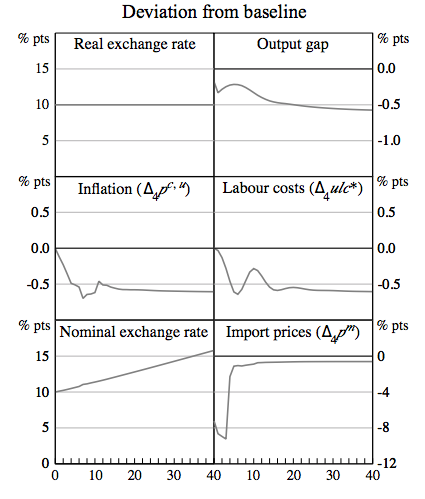

Much of the confusion about policy seems to relate to uncertainty about mapping from FX to interest rates. There are some wild elasticities out there — but the reality (as set out in this RBA RDP) is more mundane. A 10% shock to the REER moves inflation by about 50bps over three years, and moves the output gap by about the same amount. A good deal of the increase in inflation is from import prices, — which may or may not be ignored, depending on the broader context.

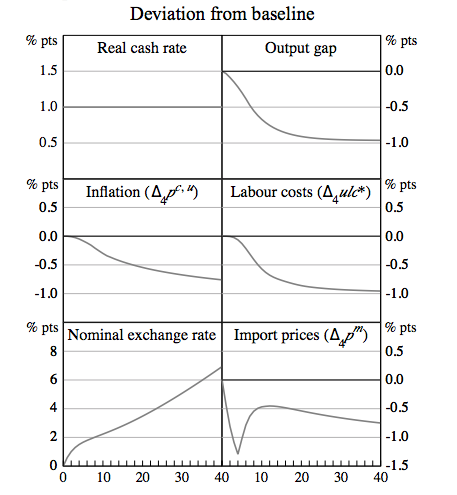

Leaving aside the debate about import prices as FX adjusts, a 100bps move in the real cash rate moves the output gap by about twice as much over a three-year period, and has about the same impact on inflation. So while a 10% move in the REER maps to ~100bps of cuts in headline CPI terms, it is more like a 50bps cash rate change in growth terms.

With this in mind, I doubt that the AUD is a major obstacle to the RBA easing rates further — which I think is basically the message of today’s post-meeting statement.

There are some notable tweaks to the last two section, which are along these lines.

First, the financial conditions section is a total re-write. I think there are two points that are being made here:

1. Policy is working and there’s more to come from prior easing:

The easing in monetary policy over the past 18 months has supported interest-sensitive areas of spending and has been reflected in portfolio shifts by savers and higher asset values. Further effects can be expected over time.

It’s worth nothing that they said this in April and cut in May, so just so there’s more loaded into the pipe does not mean they cannot cut further.

2. FX was over-valued before, so the move down isn’t troubling:

The exchange rate has depreciated since the previous Board meeting, although, as the Board has noted for some time, it remains high considering the decline in export prices that has taken place over the past year and a half.

The conclusion and summary section has been changed in three ways. Two of these are substantive points, and the third seems to be a communications improvement (aimed at dolts like me who over-emphasised the demand-test prior to May).

1. The 2.75% rate is meeting by meeting (my emphasis):

the stance of monetary policy remained appropriate for the time being

2. There remains scope for further cuts — but note the subtle change from would afford scope to ease policy further. My guess is that this is mostly stylistic, with a common sense adjustment to reflect the fact that they used some of that scope in May, and that the inflation outlook is uncertain given the AUD’s recent decline.

the inflation outlook, as currently assessed, may provide some scope for further easing, should that be required to support demand.

3. The new communications bit: making the inflation link explicit (so if they miss on inflation, they cut), to prevent dolts like me from ignoring absurdly low CPI prints in the future.

the easier financial conditions now in place will contribute to a strengthening of growth over time, consistent with achieving the inflation target

Are you still bullish on AUD or bearish now? Don’t fight the RBA…..

not super bearish at this level — though in the medium term, the REER is way too high, so either we have very low inflation or a lower NEER.

abd since the RBA don’t want very low inflation, they’ll keep cutting rates and push the dollar down a bit more….

Thanks for the post. I agree FX is no barrier. The AUD might rise again anyway when the market works out that the Fed is unlikely to taper much in a hurry. Also interesting they didn’t mention property, probably because RP Data prices and clearance rates are moving in opposite directions. The thing I find puzzling is that another cut is so widely expected in the near future (which implies that the data doesn’t need to surprise for a cut) that the RBA seems to be a passive player rather than the maker of policy. If a central bank is credible and the market is reasonably efficient, shouldn’t expectations around future moves be roughly symmetrical if the bank is doing its job properly?

Australian economy is at the top and the US economy at the bottom, the monetary gap will close sooner or later.

Actually today I read this, extremely bearish I admit, but it has some truth in it!

“With the Federal Reserve immersed in aggressive balance sheet expansion through the use of quantitative easing the Greenback has become a form of funding especially within the emerging markets through various official and unofficial pegs. At the behest of the Fed through its forward guidance, investors have borrowed these cheap dollar assets to invest in higher yielding non-dollar ones. Looking at the difference between the growth in FX reserves and cumulative current account surpluses we can estimate the rough size of the short USD carry trade. According to the most recent data it is at least around $2 trillion based on this metric! The whole trade, however, is built on the notion that the Fed and other central banks will continue with this policy into perpetuity. For this reason even slightest realistic hint that the Federal Reserve is set to move away from ZIRP has the potential to unravel the whole thing. All those who have borrowed dollar assets will be forced to buy back their dollars forcing the currency higher – some 2 trillion USD worth! This de facto policy tightening would have grave and dramatic knock on effects for emerging and developed markets alike. Pay close attention to the dollar. Prolonged strength in the currency could the unexpected tail that prompts the beginning of the end in the latest central bank induced asset bubble.”

Hope he is wrong. But if central banks made it, why can’t they keep it up as surely they do not want a global financial meltdown?

The longer they wait, the bigger the bubble. I think it would be good at this point to test for it and to send messages to the markets to give them time to ‘smoothly’ reverse some of their trades, that’s probably what the fed are trying to achieve with these tapering talks. I think they’ll manage but they should stop supporting this one way trade / ‘fed put’. When you see markets down on good news one must think the above analysis is correct.

I flip in and out of thinking that central banks are almost always passive — that they are basically just validators. Most central bank policy seems to be fairly systematic + appropriate, which means they are not the source of fluctuations.

i agree, in an previous testimony Stevens said they are mainly reactive as they think forecasting is too hard and data itself is always lagging anyways (especially if you need to use trend data).

you are on the money as usual( get it!). God analysis but I am preoocuied elsewhere. ( Castle)

sorry you are not that high. analysis is good!

BUT we all want to know what you think Kate Beckett will say!!!!

Okay, don’t think me weird, but I do not watch tv :)

I have a theory.

comments anyone?

Yes there is apparently more to life than Castle

Good theory. When inflation is running low and asset prices are flat to down and you have a large debt to repay, then you can’t be happy.

When you are ‘geared’, you need inflation to help you repay your debt, the level of interest rates itself does not matter at all. If I borrowed money to buy an investment worth 300k, I’d prefer that investment to be worth now 400k and rates at 8% rather than the same investment to still to be worth 300k with rates at 5%.

Let’s say that:

– superannuation returns were not good since 2008

– low rates on your term deposits now, makes it harder for saver

– property investors did not see any appreciation and are mostly negative geared

– govt finances are deteriorating

– small business are seeing their costs rising (salaries are sticky to the downside) but revenues are not growing like they used to (because debt is not growing like it used to)

Our economy is addicted to inflation and more and more debt. When that does not happen, we are unhappy and want to change our govt (even thought this situation has nothing to do with the current govt really, it’s a global situation and we were temporarily shielded by the mining boom).

Makes sense – high ngdp feel like a golden age, low feels bad. Get your 9% return for 12w now!

I am fully on board the NGDP cart, both as a proxy for what matters to people most, as well and (hence) as a preferable target for Mon pol. Sumner had a famous post a couple of years ago where he argued for banning discussion of the term ‘inflation’.

More specifically, I agree that slow NGDP growth is an important reason why Labor is in such a hole. That’s why I think Hockey should talk to Stevens now about changing the target or else changing it later will look desperate and ad hoc and not changing it could lead to the Coalition being a one-term government.

I remember giving presentations way back in 93-96 when inflation came tumbling down ( as I predicted at the time).

I talked about what it meant for profit margins , asset turnover etc.

It was interesting that people, VERY senior peole in particular, always would go on about having to get a return of 15%.

When I start to inquire why you stil needed a nominal retuen of 15% and that meant a much higher real return it completely went over their heads.

It occurs to me we are seeing and hearing something similar but different today because of what you have said.

People have not realised circumstances have changed at all.

Yes, exactly, the vast majority of people think in nominal terms, not real.

What’s wrong with data in this country? The PSI came in AWFUL (second worse since 2009), but FX hardly moved!

Haha, that data is very volatile so the market ignores it.

Yes, markets tend to ignore the Australian business surveys while for China, Europe and the US they are tier-one data…. strange. I thought especially the services survey would be quite significant and actually it was leading to the weak GDP results we got (would have been a negative GDP number without exports and exports were up on commodity prices which are down this quarter so far). ToT too.

they are PSIed ff!

Gosh, we are indeed seeing the impact of fed tapering on our market already!

If you were a foreign investor, why would you buy Australian shares or bonds right now, with Australian dollar foretasted to fall further, maybe significantly?

And if you know that foreign money flows are going in the opposite direction, why would you buy right now if you are a local investor?

Anyway, after this selling wave is passed it will be a good time to buy more. But the AUD has to stabilize first.