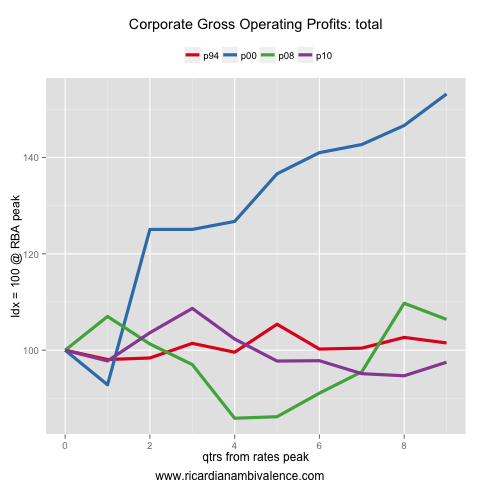

There are a great number of interesting stories in yesterday’s data-deluge, however my personal favourite is the profits story in the ABS Business Indicators release.

A comparison of the four easing cycles in the modern period clearly shows why this easing cycle has been so disappointing. It’s been nine quarters since the RBA’s tightening cycle peaked (in Q4’10), and yet the nominal value of company gross operating profits still remain below the level that was reached at that time.

In prior cycles, economy wide profits typically exceeded the prior peak by this time – and in the 2001 cycle, when the AUD was weak, housing was booming and the terms of trade were rising, profits exceeded the prior peak by more than 50%. Even then, it took the RBA about 6yrs to get the cash rate back to the prior peak — thus, current weakness suggests it will be a very long time before we see a 4.75% cash rate once again.

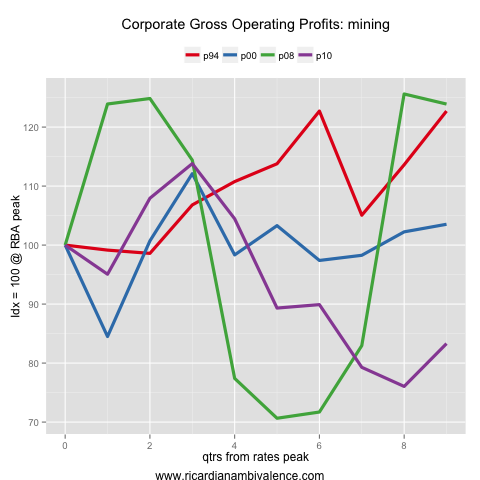

The most part of this story, of course, is the weakness in the mining sector (though it was a source of strength in Q1’13). Mining profits are ~17% below their Q4’10 level — an improvement on down ~24% in Q4’12, but weak relative to all prior cycles (by the way, note how critical mining cycles have been in Australian economic cycles).

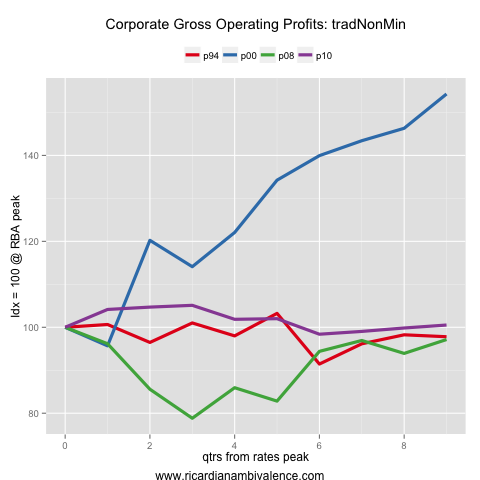

For the rest of the economy, I think it makes sense to split it between the non-mining tradable sector (this is the sector that’s been most harmed by mining’s expansion), and the non-tradable sector.

In the non-mining tradable sector (manufacturing, transport, wholesale, retail and accommodation & food services), profits firmed a little in Q1’13, taking the index back above the level when rates peaked in Q4’10. If the AUD continues to weaken, this is the sector where I’d expect to see profits rise — which will presage an increase in investment and employment.

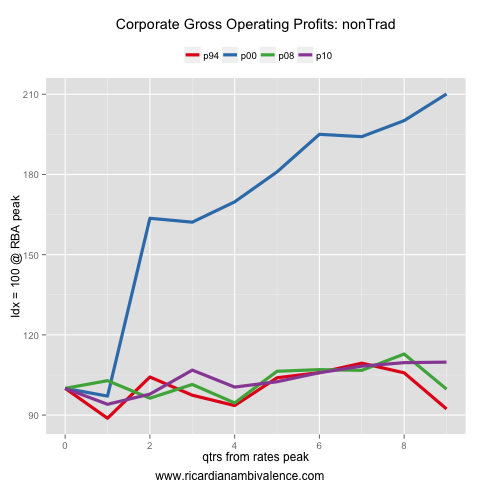

I have bucketed the rest of the economy in the non-tradable sector. This sector ought to be more sensitive to the level of interest rates. Surely enough, here we can see a little more policy traction, with profits up ~7% in the last year.